Over the past six months, Netflix’s stock price fell to $77.63. Shareholders have lost 15.1% of their capital, which is disappointing considering the S&P 500 has climbed by 8.4%. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Following the drawdown, is now a good time to buy NFLX? Find out in our full research report, it’s free.

Why Is Netflix a Good Business?

Launched by Reed Hastings as a DVD mail rental company until its famous pivot to streaming in 2007, Netflix (NASDAQ: NFLX) is a pioneering streaming content platform.

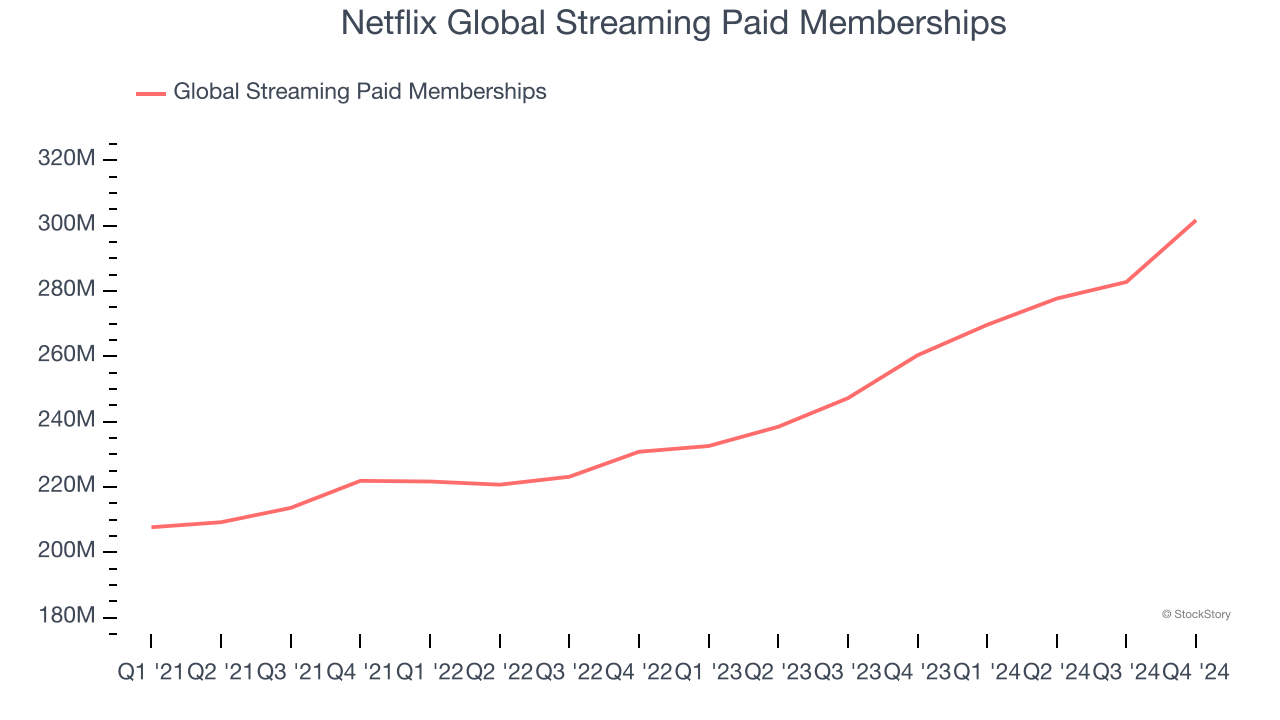

1. Global Streaming Paid Memberships Skyrocket, Fueling Growth Opportunities

As a subscription-based app, Netflix generates revenue growth by expanding both its subscriber base and the amount each subscriber spends over time.

Over the last two years, Netflix’s global streaming paid memberships, a key performance metric for the company, increased by 15.6% annually. This growth rate is among the fastest of any consumer internet business and indicates its offerings have significant traction.

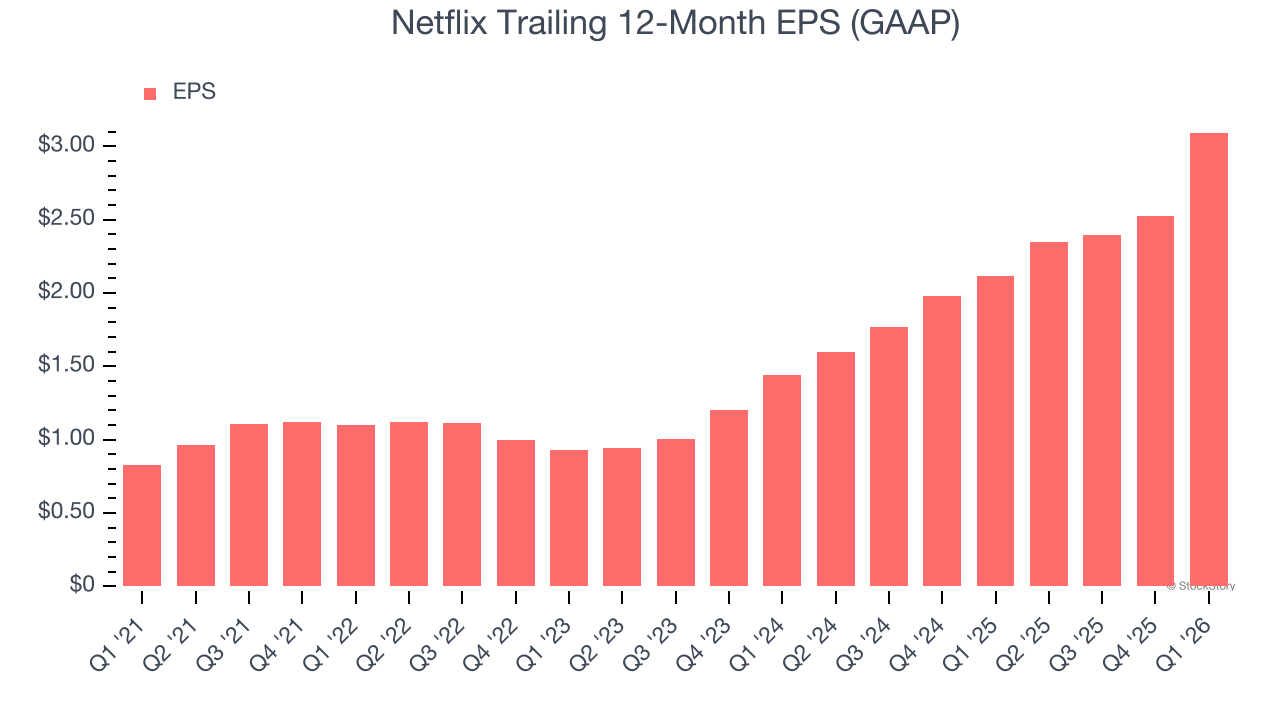

2. Outstanding Long-Term EPS Growth

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Netflix’s EPS grew at 49.2% compounded annual growth rate over the last three years, higher than its 13.7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

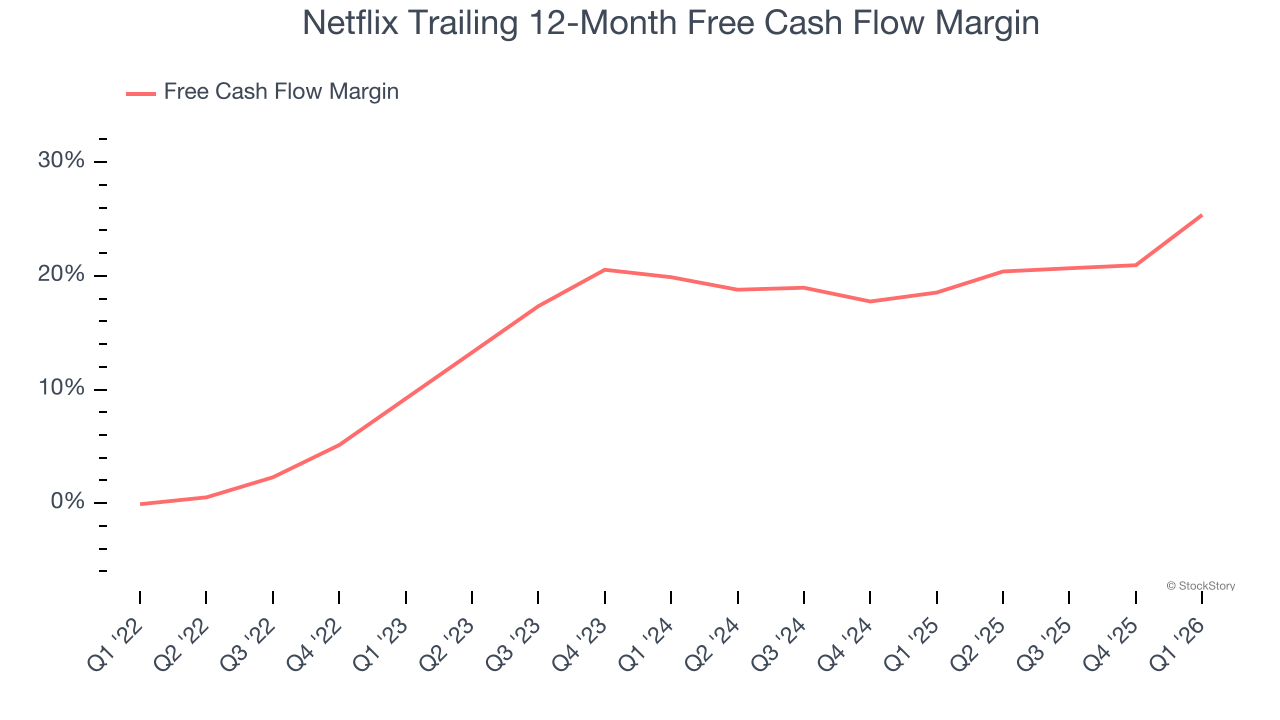

3. Increasing Free Cash Flow Margin Juices Financials

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Netflix’s margin expanded by 16.2 percentage points over the last few years. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability. Netflix’s free cash flow margin for the trailing 12 months was 25.4%.

Final Judgment

These are just a few reasons Netflix is a high-quality business worth owning. After the recent drawdown, the stock trades at 17.9× forward EV/EBITDA (or $77.63 per share). Is now the time to initiate a position? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Netflix

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.