While the broader market has struggled with the S&P 500 down 2.8% since October 2025, Park-Ohio has surged ahead as its stock price has climbed by 15% to $24.14 per share. This performance may have investors wondering how to approach the situation.

Is there a buying opportunity in Park-Ohio, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Do We Think Park-Ohio Will Underperform?

Despite the momentum, we're cautious about Park-Ohio. Here are three reasons there are better opportunities than PKOH and a stock we'd rather own.

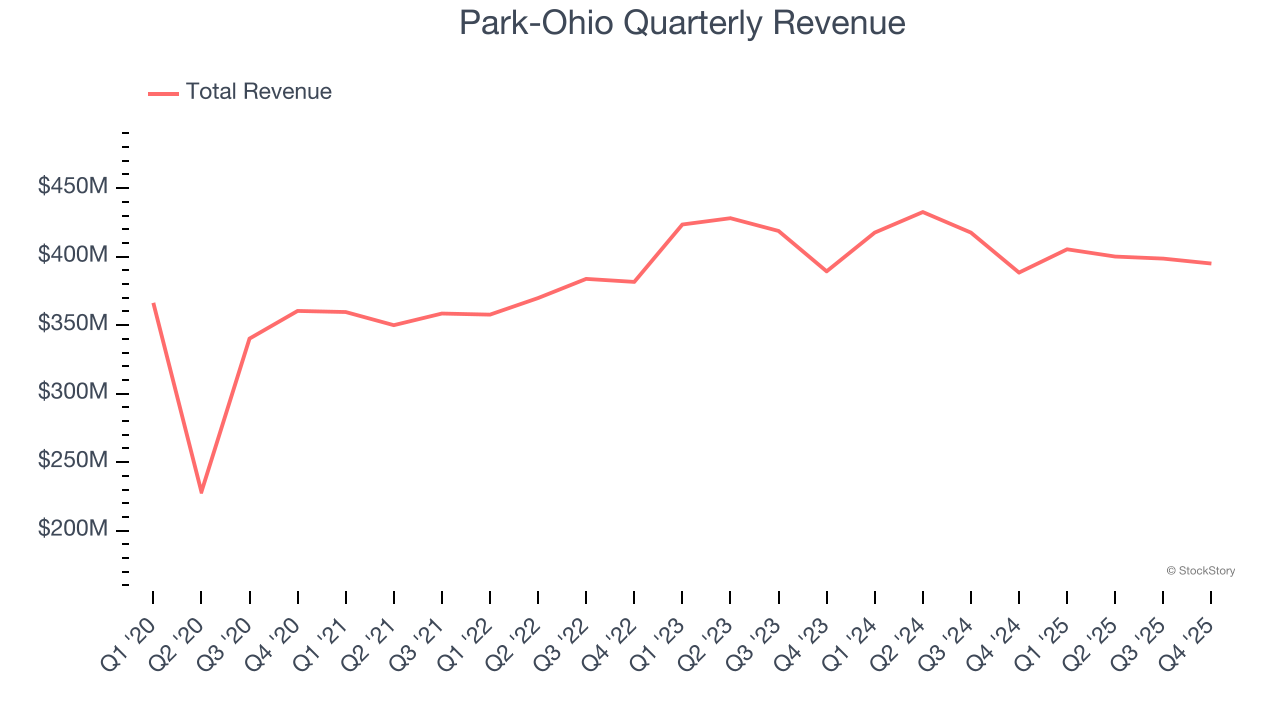

1. Long-Term Revenue Growth Disappoints

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Park-Ohio grew its sales at a sluggish 4.3% compounded annual growth rate. This fell short of our benchmark for the industrials sector.

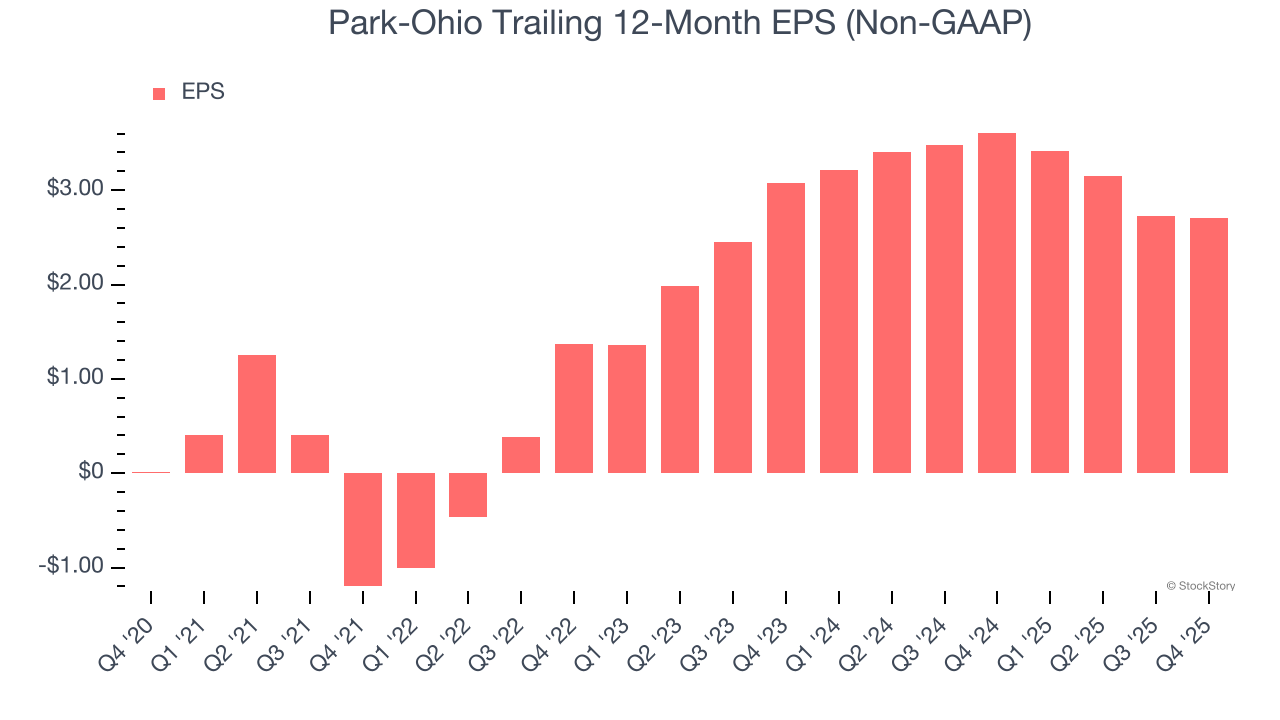

2. EPS Took a Dip Over the Last Two Years

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

Sadly for Park-Ohio, its EPS declined by more than its revenue over the last two years, dropping 6.2%. This tells us the company struggled to adjust to shrinking demand.

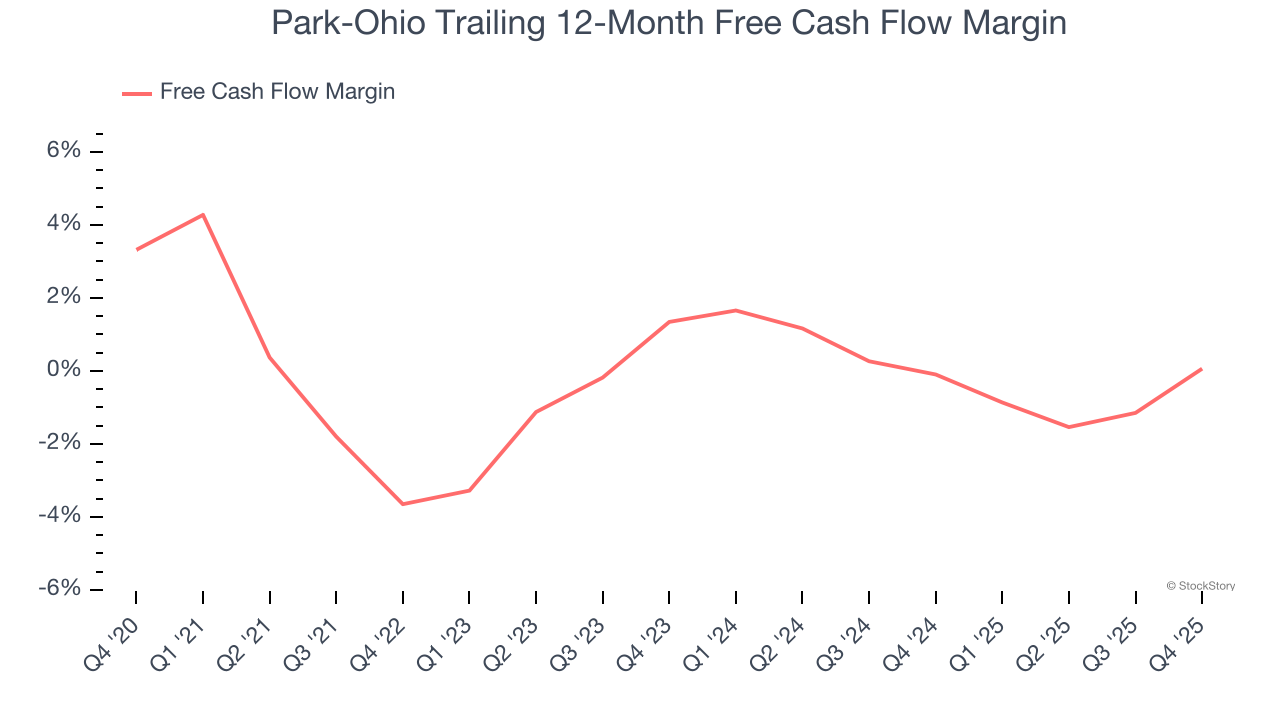

3. Cash Burn Ignites Concerns

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

While Park-Ohio posted positive free cash flow this quarter, the broader story hasn’t been so clean. Park-Ohio’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 1.1%, meaning it lit $1.12 of cash on fire for every $100 in revenue.

Final Judgment

Park-Ohio doesn’t pass our quality test. With its shares beating the market recently, the stock trades at 7.8× forward P/E (or $24.14 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better stocks to buy right now. Let us point you toward one of our top software and edge computing picks.

Stocks We Would Buy Instead of Park-Ohio

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.