Popular health insurance provider UnitedHealth Group (UNH) is down nearly 50% over the past year amid multiple issues, including a U.S. Department of Justice (DOJ) investigation and rising Medicare costs. The Centers for Medicare & Medicaid Services (CMS) proposed that Medicare Advantage payment rates would increase by 0.09% in 2027, significantly lower than the 4%-6% increase Wall Street had expected, leading to a selloff in UNH’s stock. Moreover, a subdued 2026 top line guidance has spooked investors.

However, in this situation, Raymond James analysts upgraded UnitedHealth from “Market Perform” to “Outperform” and set a $330 price target, implying a 20.4% upside from current levels. Analyst John Ransom believes that artificial intelligence (AI) can reduce the company’s general and administrative costs and improve margin visibility in the Optum Health segment.

Additionally, the analyst noted that UnitedHealth management’s recent comments suggest there is a “material opportunity” to right-size the company’s cost structure, and given its large organizational structure, it is more likely to realize AI-led cost savings than its peers.

We take a deeper look at UnitedHealth now.

About UnitedHealth Stock

Based in Eden Prairie, Minnesota, UnitedHealth Group is a U.S.-based health insurance and health services company, operating in the four broad segments of Optum Health, Optum Insight, Optum Rx, and UnitedHealthcare.

The Optum division provides technology-driven healthcare services, data tools, and support for providers and patients, while the UnitedHealthcare business offers a range of health benefit plans to individuals, employers, and government programs. It has a market capitalization of $248.69 billion.

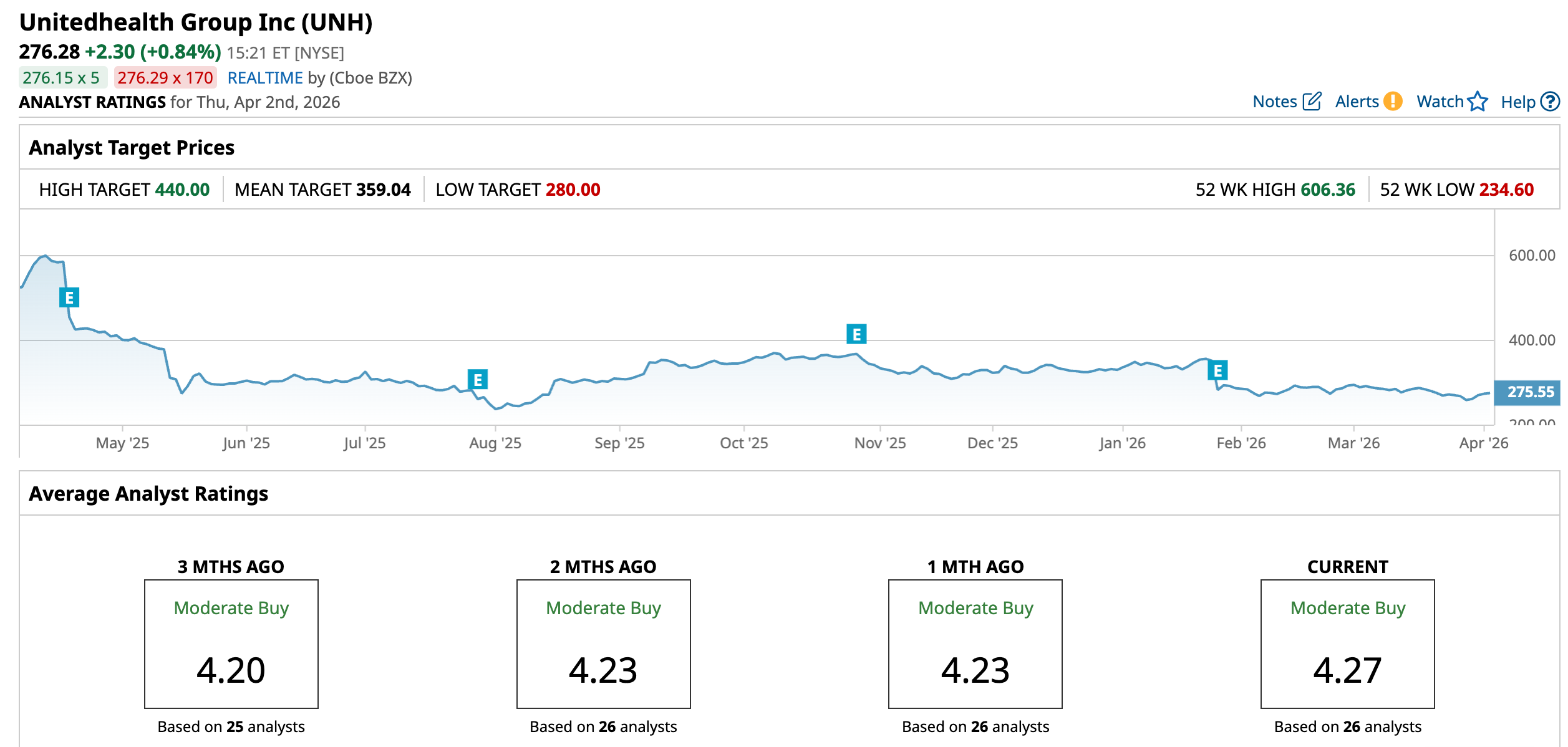

UnitedHealth’s stock has declined 47.24% over the past 52 weeks, as the company faces pressure from rising Medical Care Ratio (MCR). This implied that Medicare Advantage members started using more medical services than anticipated, and when claim payouts rise, it puts pressure on margins if revenue growth is not skyrocketing.

On top of that, in January, a U.S. Senate Committee report stated that UnitedHealth has used aggressive risk-adjustment coding tactics to increase U.S. government reimbursement for patients enrolled in its Medicare Advantage healthcare plans, although the company has disagreed with these characterizations. This year, the stock is down 16.38%. It reached a 52-week high of $606.36 back in April 2025, but is down 54.4% from that level.

The selloff has made UnitedHealth’s stock relatively cheaper. Its forward-adjusted price-to-earnings (non-GAAP) ratio of 15.30 times is lower than the industry average of 17.16 times.

UnitedHealth Reported Mixed Fourth-Quarter Results

For the fourth quarter of fiscal 2025, UnitedHealth reported a 12.3% year-over-year (YOY) growth in total revenues to $113.22 billion, which modestly missed the $113.26 billion that Street analysts had expected.

This was, of course, based on premium revenue increasing 16.1% from the prior-year period to $88.81 billion. However, as operating costs increased, UnitedHealth’s adjusted EPS dropped from $6.81 in Q4 2024 to $2.11 in Q4 2025. However, the EPS figure was higher than the $2.09 that analysts had expected.

The company’s annual revenue grew 11.8% YOY to $447.57 billion. Optum’s total revenue increased 7% from the prior year to $270.62 billion. The segment also supported more than 123 million consumers across its businesses.

UnitedHealth’s medical care ratio for 2025 was 88.9%, higher than the 85.5% that it had reported in 2024. The increase was primarily due to CMS’s cuts to Medicare funding, the payment changes introduced by the Inflation Reduction Act, and the ongoing acceleration of medical care cost increases. Its 2025 adjusted EPS dropped by 40.9% YOY to $16.35.

Wall Street analysts are moderately optimistic about UnitedHealth’s future earnings. For the current fiscal year, EPS is projected to surge 8% annually to $17.65, followed by a 12.6% growth to $19.87 in the 2027 fiscal year. However, analysts expect the company’s EPS to drop by 10.3% YOY to $6.46 for the first quarter of 2026 (to be reported on Apr. 21, before the market opens).

What Do Analysts Think About UnitedHealth Stock?

Apart from Raymond James analysts, Wall Street analysts have also expressed similar bullish sentiment toward UnitedHealth’s stock. In February, analysts at Mizuho maintained the stock with a “Outperform” rating, despite the company being under investigation by the DoJ. Mizuho's analysts believe the issue has already been addressed by regulatory measures initiated by the CMS.

Additionally, in the same month, JP Morgan analyst Lisa Gill maintained an “Overweight” rating for UnitedHealth, but lowered the price target from $425 to $389. Truist Securities analyst David Macdonald also kept a “Buy” rating but reduced the price target from $410 to $370. In January, Wells Fargo analyst Stephen Baxter also did the same, maintaining an “Overweight” rating but cutting the price target from $400 to $370.

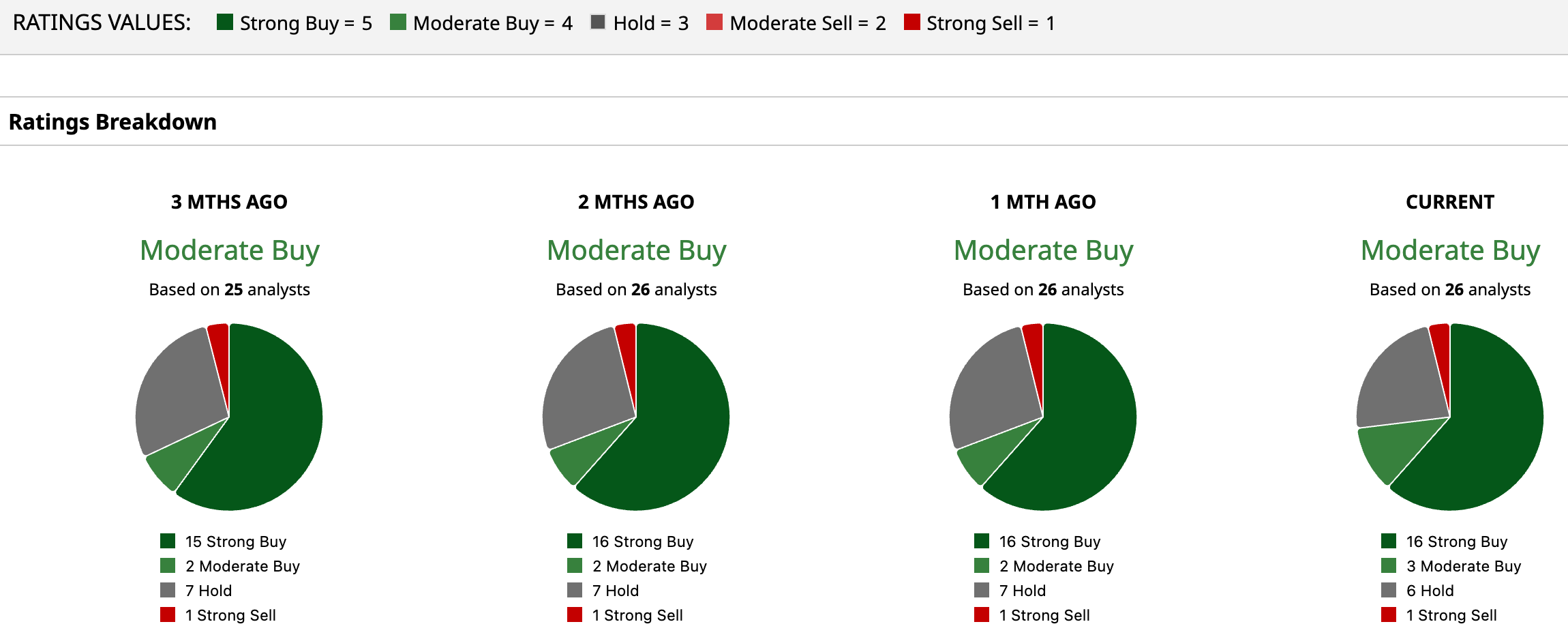

UnitedHealth has long been a popular name on Wall Street, with analysts awarding it a consensus “Moderate Buy” rating overall. Of the 26 analysts rating the stock, a majority of 16 analysts have given it a “Strong Buy” rating, three analysts rated it “Moderate Buy,” six analysts are playing it safe with a “Hold” rating, while one recommended “Strong Sell.” The consensus price target of $359.04 represents 29% upside from current levels.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Sysco Just Announced a $29.1 Billion Acquisition and Wall Street Is Nervous. Can a 3% Dividend Sweeten the Deal?

- Plug Power Just Scored a New Deal in Canada. Should You Buy Plug Stock Here?

- Why Bernstein Thinks You Should Buy the Dip in Sandisk Stock Here

- Should You Chase the Amazon-Driven Rally in Globalstar Stock Today?