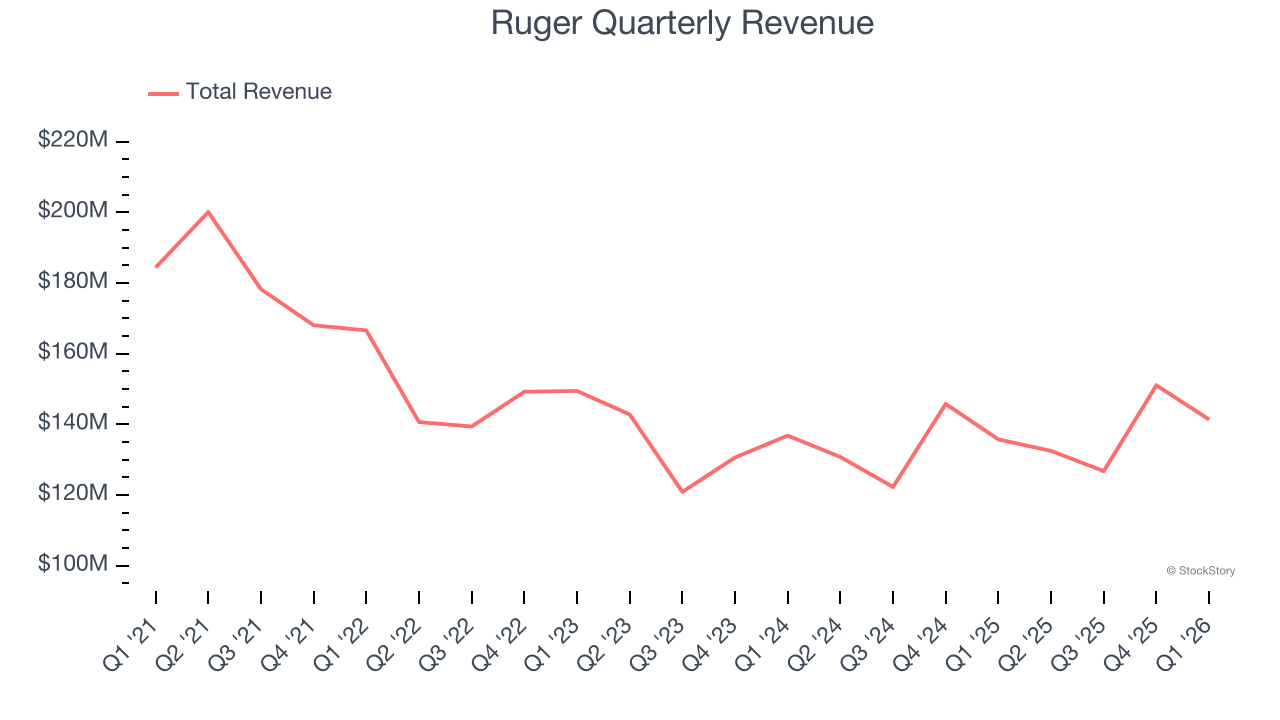

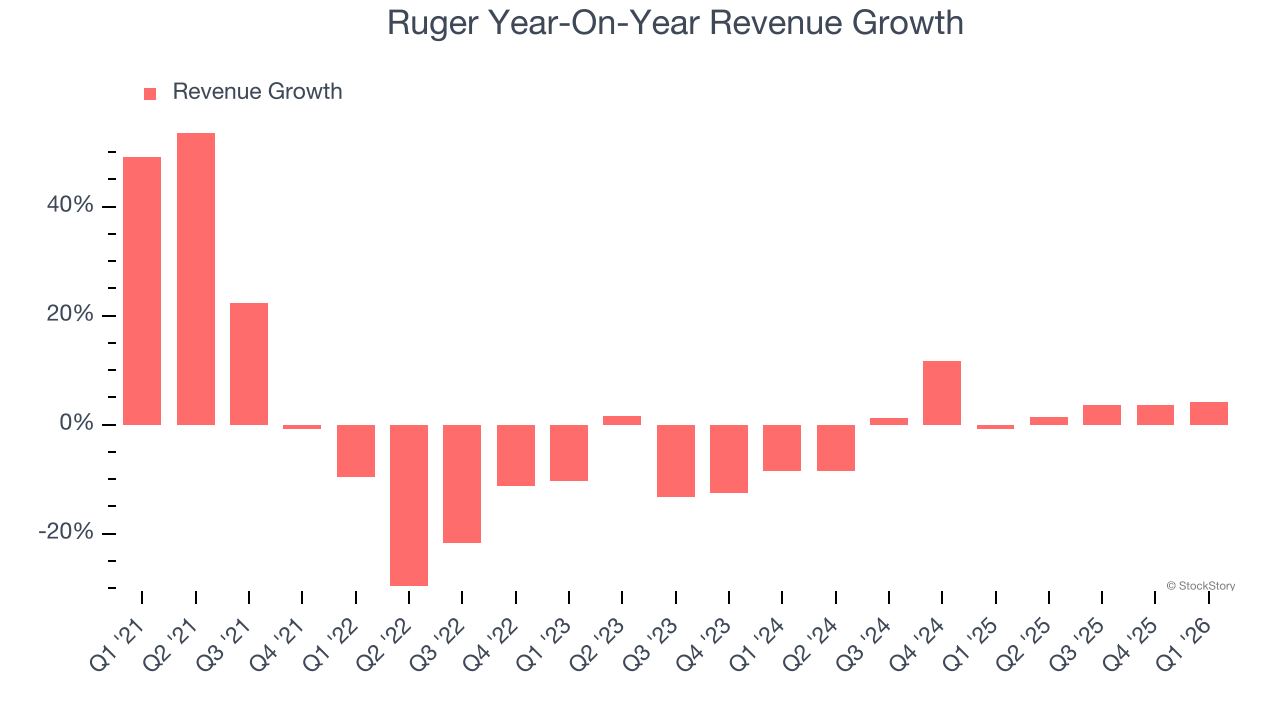

American firearm manufacturing company Ruger (NYSE: RGR) reported Q1 CY2026 results beating Wall Street’s revenue expectations, with sales up 4.1% year on year to $141.4 million. Its non-GAAP profit of $0.27 per share was 20.6% below analysts’ consensus estimates.

Is now the time to buy Ruger? Find out by accessing our full research report, it’s free.

Ruger (RGR) Q1 CY2026 Highlights:

- Revenue: $141.4 million vs analyst estimates of $137.3 million (4.1% year-on-year growth, 3% beat)

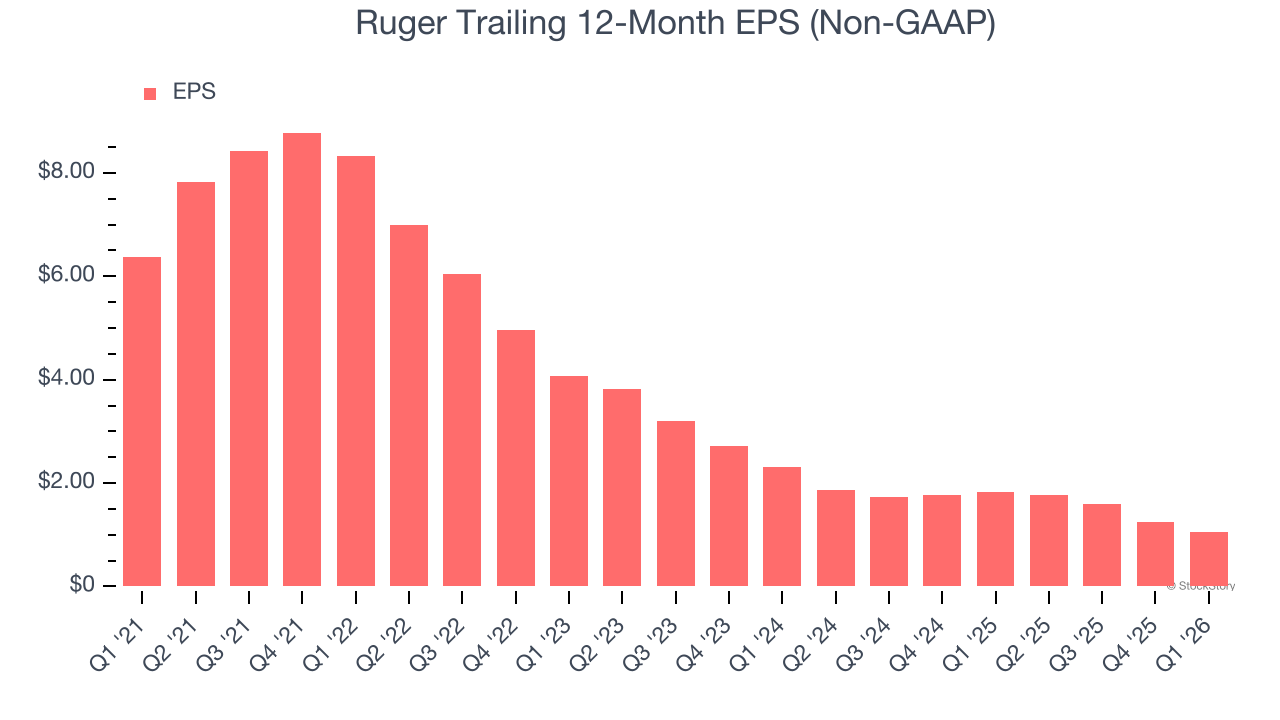

- Adjusted EPS: $0.27 vs analyst expectations of $0.34 (20.6% miss)

- Adjusted EBITDA: $10.88 million vs analyst estimates of $11.87 million (7.7% margin, 8.3% miss)

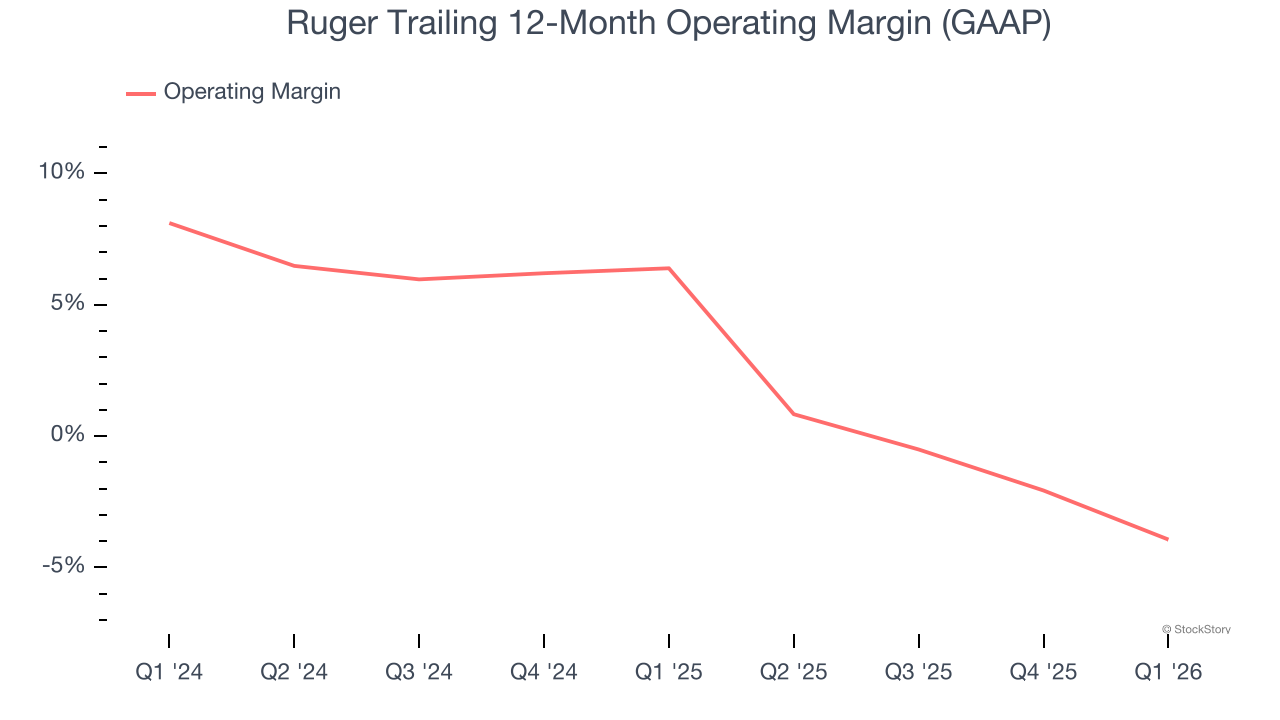

- Operating Margin: -1.4%, down from 6.2% in the same quarter last year

- Free Cash Flow Margin: 9.9%, up from 7.4% in the same quarter last year

- Market Capitalization: $666.2 million

Company Overview

Founded in 1949, Ruger (NYSE: RGR) is an American manufacturer of firearms for the commercial sporting market.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Ruger’s demand was weak over the last five years as its sales fell at a 2.6% annual rate. This was below our standards and is a sign of poor business quality.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Ruger’s annualized revenue growth of 1.9% over the last two years is above its five-year trend, which is encouraging.

This quarter, Ruger reported modest year-on-year revenue growth of 4.1% but beat Wall Street’s estimates by 3%.

Looking ahead, sell-side analysts expect revenue to grow 1.4% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and implies its newer products and services will not lead to better top-line performance yet.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Ruger’s operating margin has been trending down over the last 12 months and averaged 1.1% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

In Q1, Ruger generated an operating margin profit margin of negative 1.4%, down 7.6 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Ruger, its EPS declined by 30.3% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

In Q1, Ruger reported adjusted EPS of $0.27, down from $0.46 in the same quarter last year. This print missed analysts’ estimates. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from Ruger’s Q1 Results

It was encouraging to see Ruger beat analysts’ revenue expectations this quarter. On the other hand, its adjusted operating income missed and its EPS fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 2% to $39.78 immediately following the results.

Ruger didn’t show it’s best hand this quarter, but does that create an opportunity to buy the stock right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).