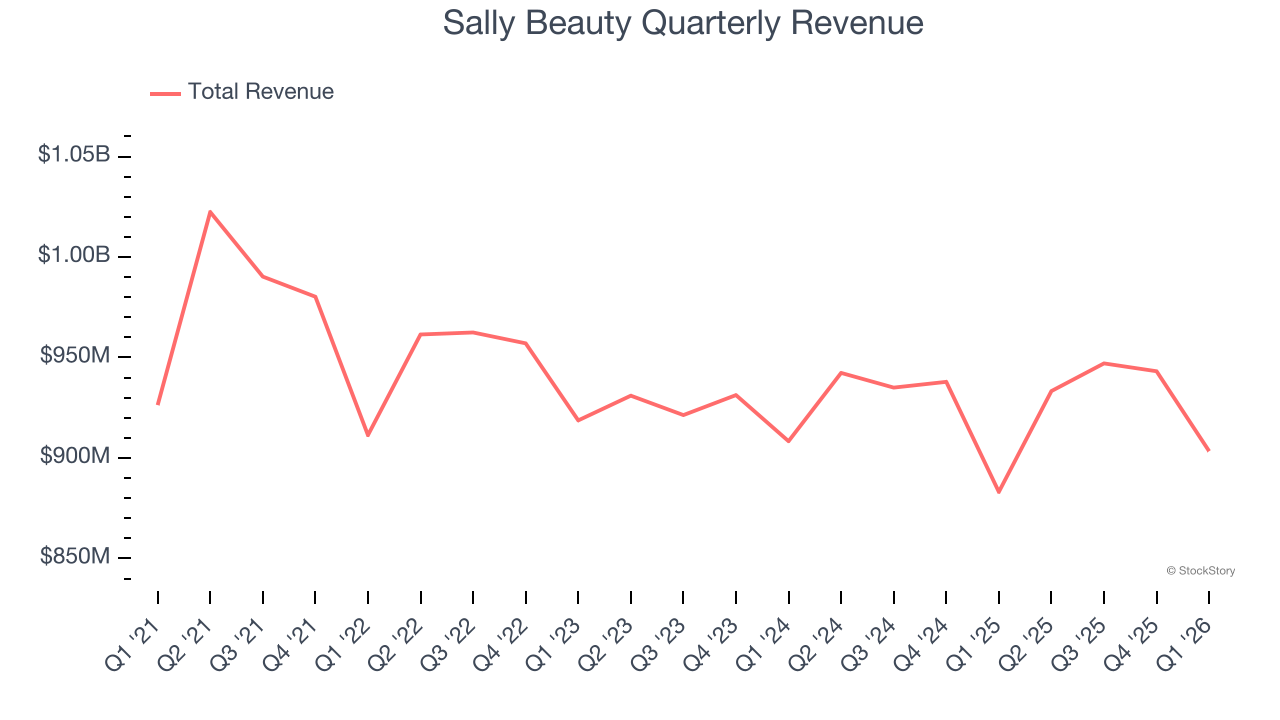

Beauty supply retailer Sally Beauty (NYSE: SBH) met Wall Street’s revenue expectations in Q1 CY2026, with sales up 2.3% year on year to $903.4 million. On the other hand, next quarter’s revenue guidance of $937 million was less impressive, coming in 1.2% below analysts’ estimates. Its non-GAAP profit of $0.44 per share was 7.3% above analysts’ consensus estimates.

Is now the time to buy Sally Beauty? Find out by accessing our full research report, it’s free.

Sally Beauty (SBH) Q1 CY2026 Highlights:

- Revenue: $903.4 million vs analyst estimates of $899.5 million (2.3% year-on-year growth, in line)

- Adjusted EPS: $0.44 vs analyst estimates of $0.41 (7.3% beat)

- Adjusted EBITDA: $104.3 million vs analyst estimates of $99.35 million (11.5% margin, 5% beat)

- The company reconfirmed its revenue guidance for the full year of $3.74 billion at the midpoint

- Management reiterated its full-year Adjusted EPS guidance of $2.06 at the midpoint

- Operating Margin: 8%, in line with the same quarter last year

- Free Cash Flow Margin: 4.9%, up from 3.6% in the same quarter last year

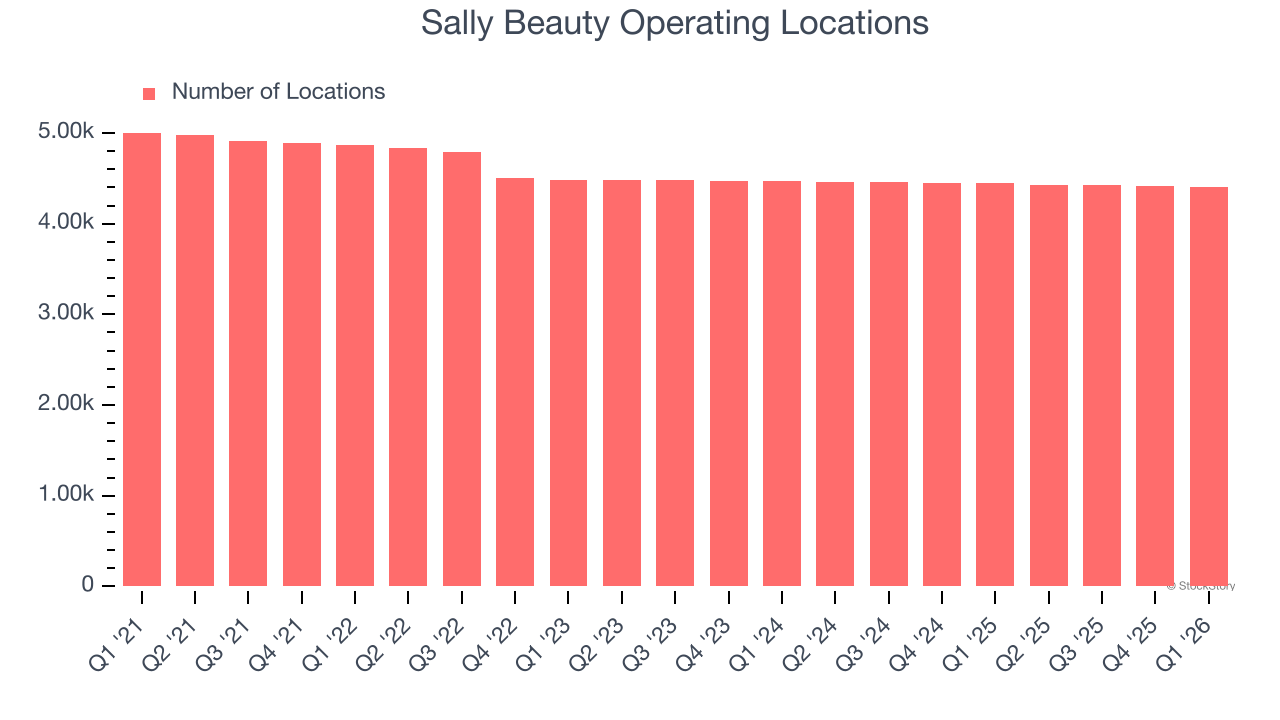

- Locations: 4,399 at quarter end, down from 4,446 in the same quarter last year

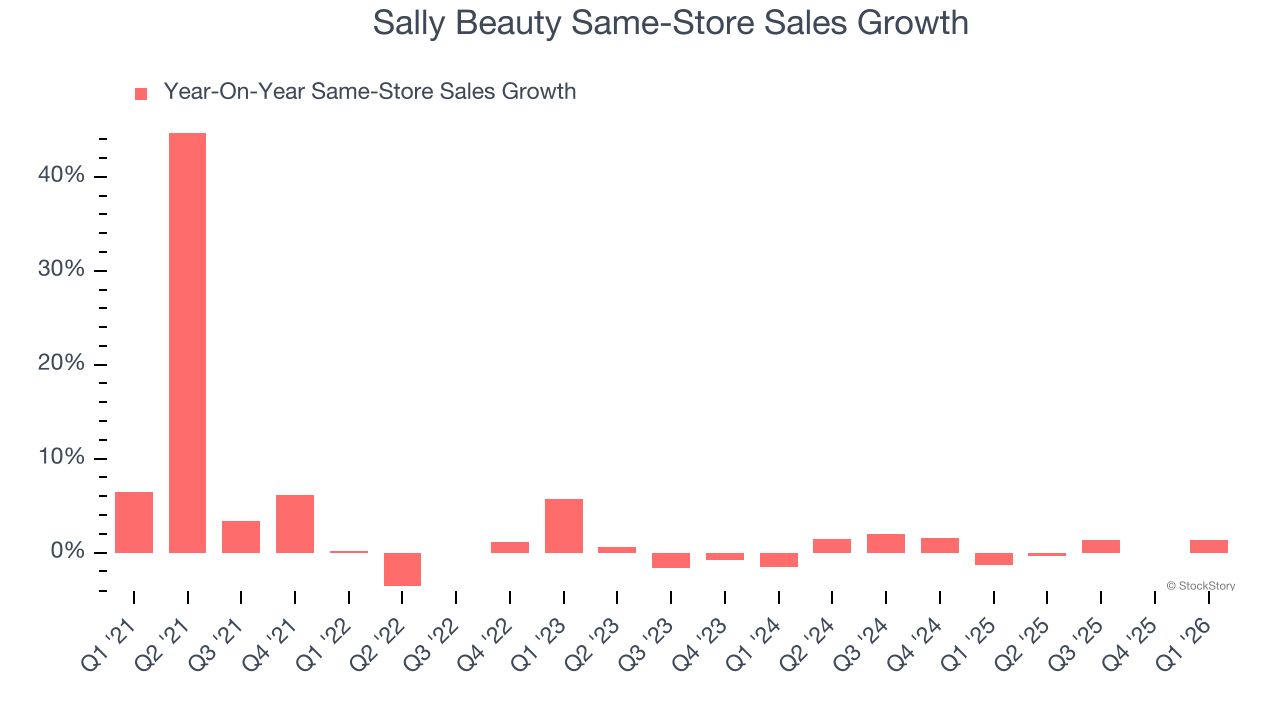

- Same-Store Sales rose 1.3% year on year (-1.3% in the same quarter last year)

- Market Capitalization: $1.36 billion

Company Overview

Catering to both everyday consumers as well as salon professionals, Sally Beauty (NYSE: SBH) is a retailer that sells salon-quality beauty products such as makeup and haircare products.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $3.73 billion in revenue over the past 12 months, Sally Beauty is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers.

As you can see below, Sally Beauty struggled to increase demand as its $3.73 billion of sales for the trailing 12 months was close to its revenue three years ago. This was mainly because it didn’t open many new stores.

This quarter, Sally Beauty grew its revenue by 2.3% year on year, and its $903.4 million of revenue was in line with Wall Street’s estimates. Company management is currently guiding for flat sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 1.5% over the next 12 months. While this projection implies its newer products will fuel better top-line performance, it is still below the sector average.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Store Performance

Number of Stores

A retailer’s store count often determines how much revenue it can generate.

Sally Beauty operated 4,399 locations in the latest quarter, and over the last two years, has kept its store count flat while other consumer retail businesses have opted for growth.

When a retailer keeps its store footprint steady, it usually means demand is stable and it’s focusing on operational efficiency to increase profitability.

Same-Store Sales

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales is an industry measure of whether revenue is growing at those existing stores and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Sally Beauty’s demand within its existing locations has barely increased over the last two years as its same-store sales were flat. This performance isn’t ideal, and we’d be skeptical if Sally Beauty starts opening new stores to artificially boost revenue growth.

In the latest quarter, Sally Beauty’s same-store sales rose 1.3% year on year. This performance was more or less in line with its historical levels.

Key Takeaways from Sally Beauty’s Q1 Results

We enjoyed seeing Sally Beauty beat analysts’ EBITDA expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its EPS guidance for next quarter missed and its revenue guidance for next quarter fell slightly short of Wall Street’s estimates. Overall, this was a mixed quarter. The stock traded up 2.2% to $14.34 immediately after reporting.

So should you invest in Sally Beauty right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).