Greenbrier has had an impressive run over the past six months as its shares have beaten the S&P 500 by 12.5%. The stock now trades at $50.56, marking a 19.6% gain. This run-up might have investors contemplating their next move.

Is now the time to buy Greenbrier, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is Greenbrier Not Exciting?

Despite the momentum, we're swiping left on Greenbrier for now. Here are three reasons you should be careful with GBX and a stock we'd rather own.

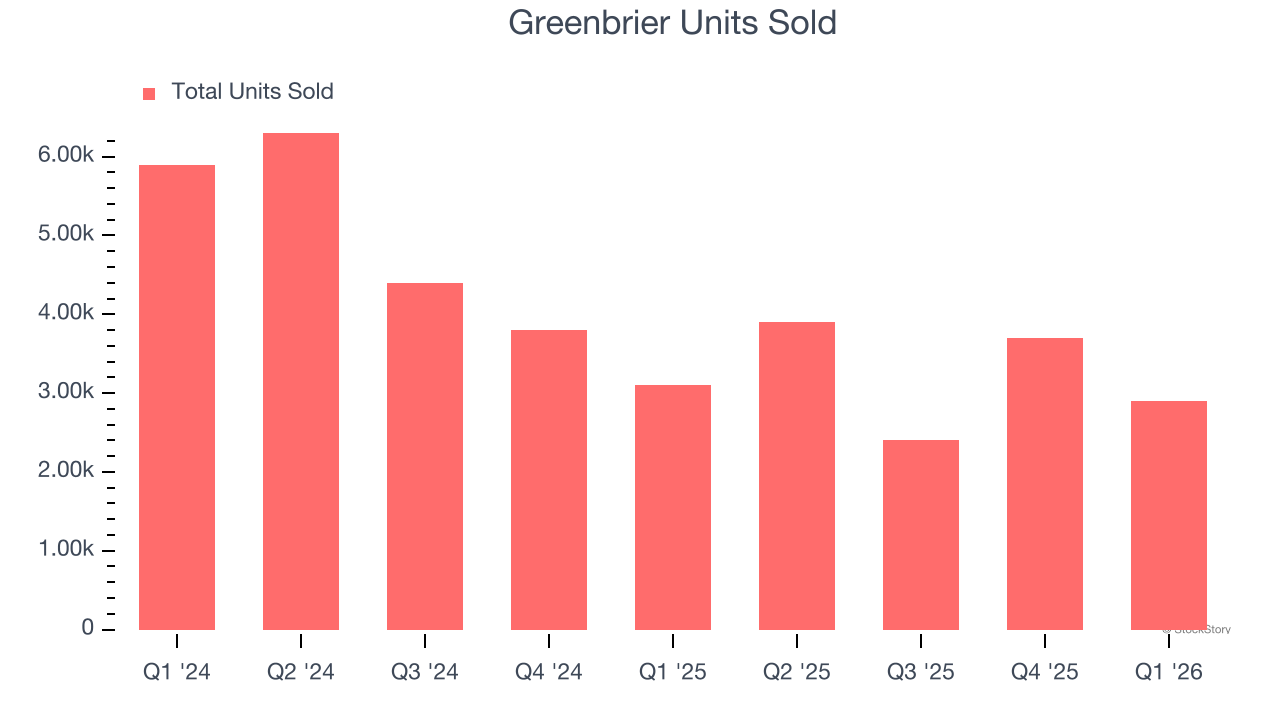

1. Demand Slips as Sales Volumes Slide

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful Heavy Transportation Equipment company because there’s a ceiling to what customers will pay.

Greenbrier’s units sold came in at 2,900 in the latest quarter, and they averaged 28% year-on-year declines over the last two years. This performance was underwhelming and implies there may be increasing competition or market saturation. It also suggests Greenbrier might have to lower prices or invest in product improvements to grow, factors that can hinder near-term profitability.

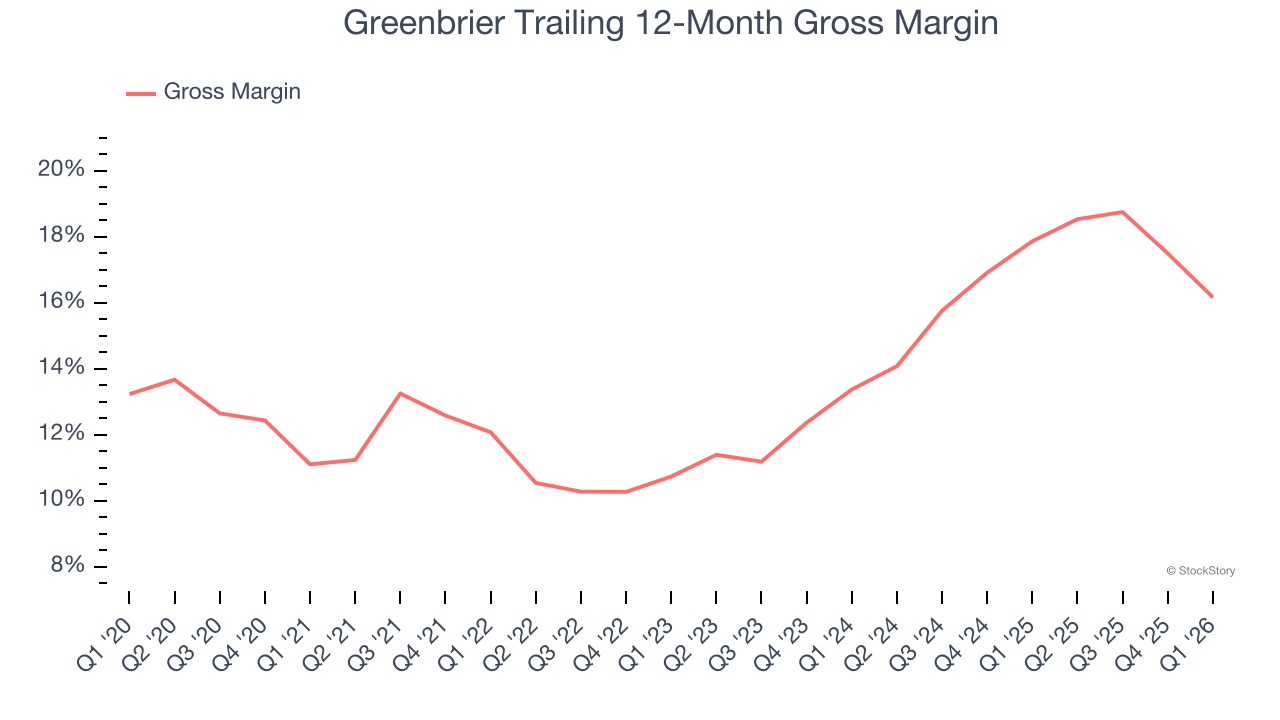

2. Low Gross Margin Reveals Weak Structural Profitability

Gross profit margin is a critical metric to track because it sheds light on its pricing power, complexity of products, and ability to procure raw materials, equipment, and labor.

Greenbrier has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 14.1% gross margin over the last five years. That means Greenbrier paid its suppliers a lot of money ($85.92 for every $100 in revenue) to run its business.

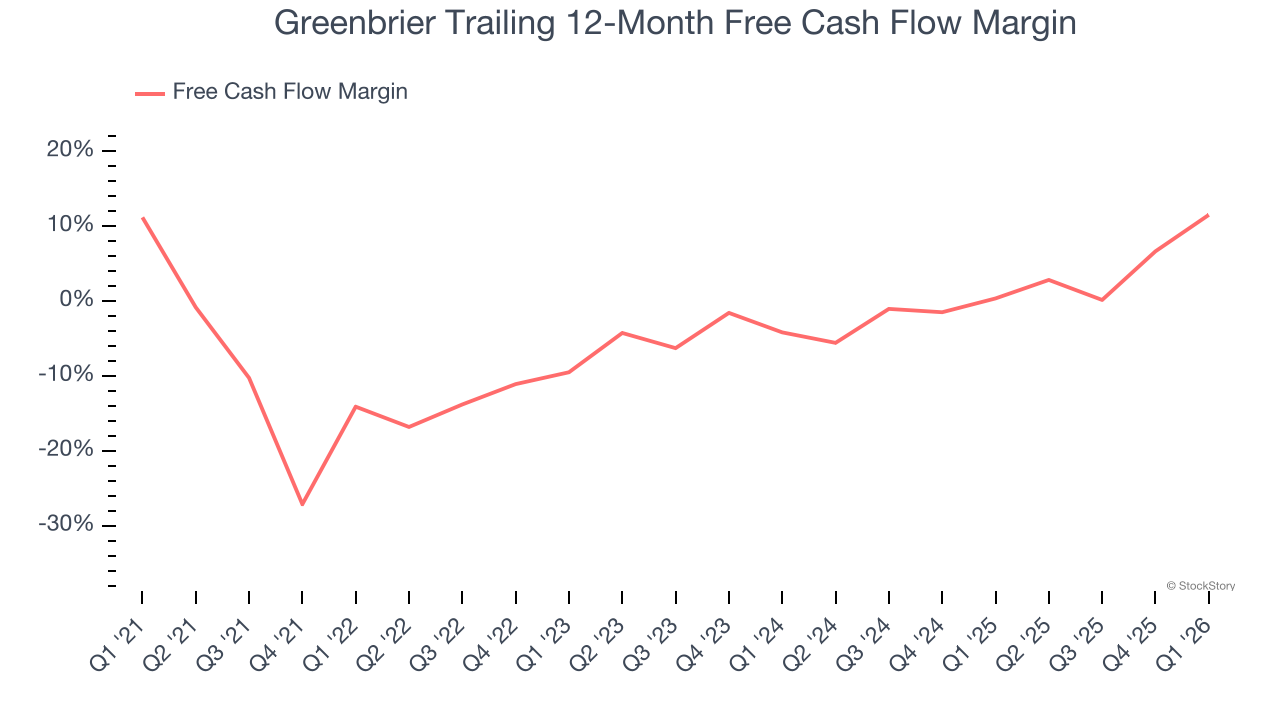

3. Cash Burn Ignites Concerns

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

While Greenbrier posted positive free cash flow this quarter, the broader story hasn’t been so clean. Greenbrier’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 3%, meaning it lit $2.98 of cash on fire for every $100 in revenue.

Final Judgment

Greenbrier isn’t a terrible business, but it doesn’t pass our quality test. With its shares beating the market recently, the stock trades at $50.56 per share (or a forward price-to-sales ratio of 0.6×). The market typically values companies like Greenbrier based on their anticipated profits for the next 12 months, but there aren’t enough published estimates to arrive at a reliable number. You should avoid this stock for now - better opportunities lie elsewhere. We’d suggest looking at one of our top digital advertising picks.

High-Quality Stocks for All Market Conditions

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum - both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks - FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.