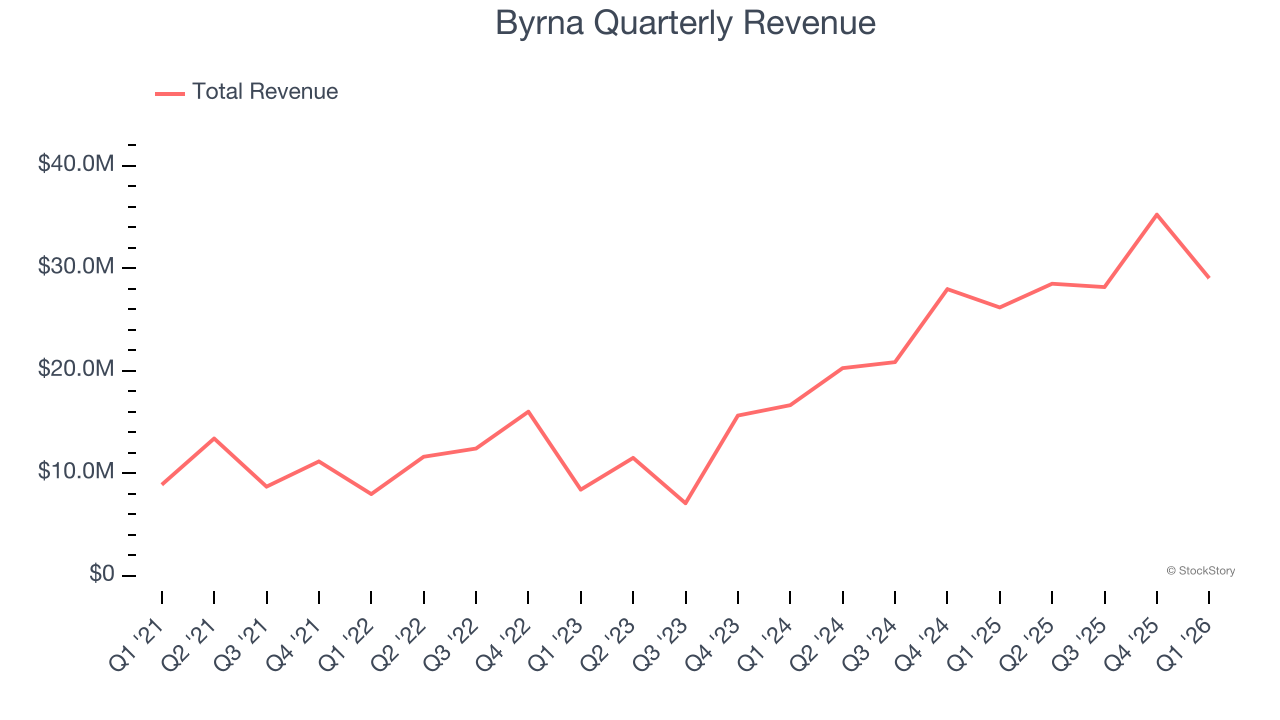

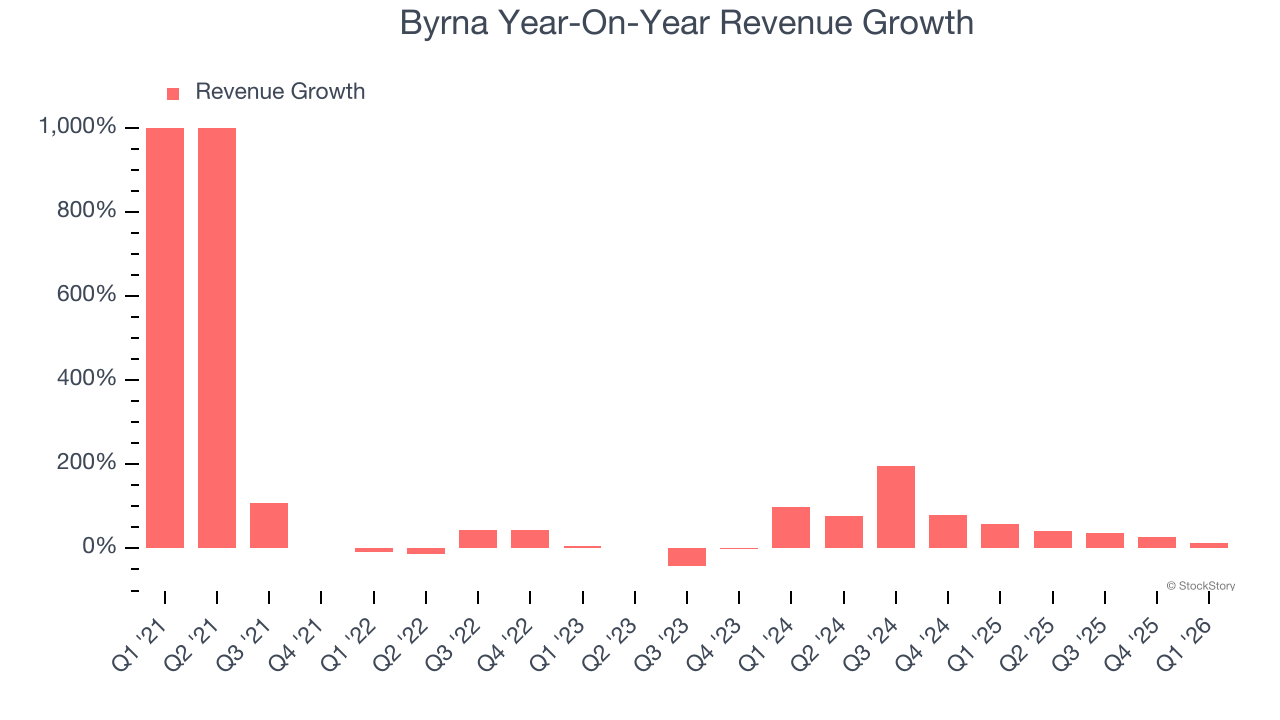

Non-lethal weapons company Byrna (NASDAQ: BYRN) missed Wall Street’s revenue expectations in Q1 CY2026, but sales rose 10.9% year on year to $29.05 million. Its GAAP profit of $0.03 per share was 57.1% below analysts’ consensus estimates.

Is now the time to buy Byrna? Find out by accessing our full research report, it’s free.

Byrna (BYRN) Q1 CY2026 Highlights:

- Revenue: $29.05 million vs analyst estimates of $29.75 million (10.9% year-on-year growth, 2.3% miss)

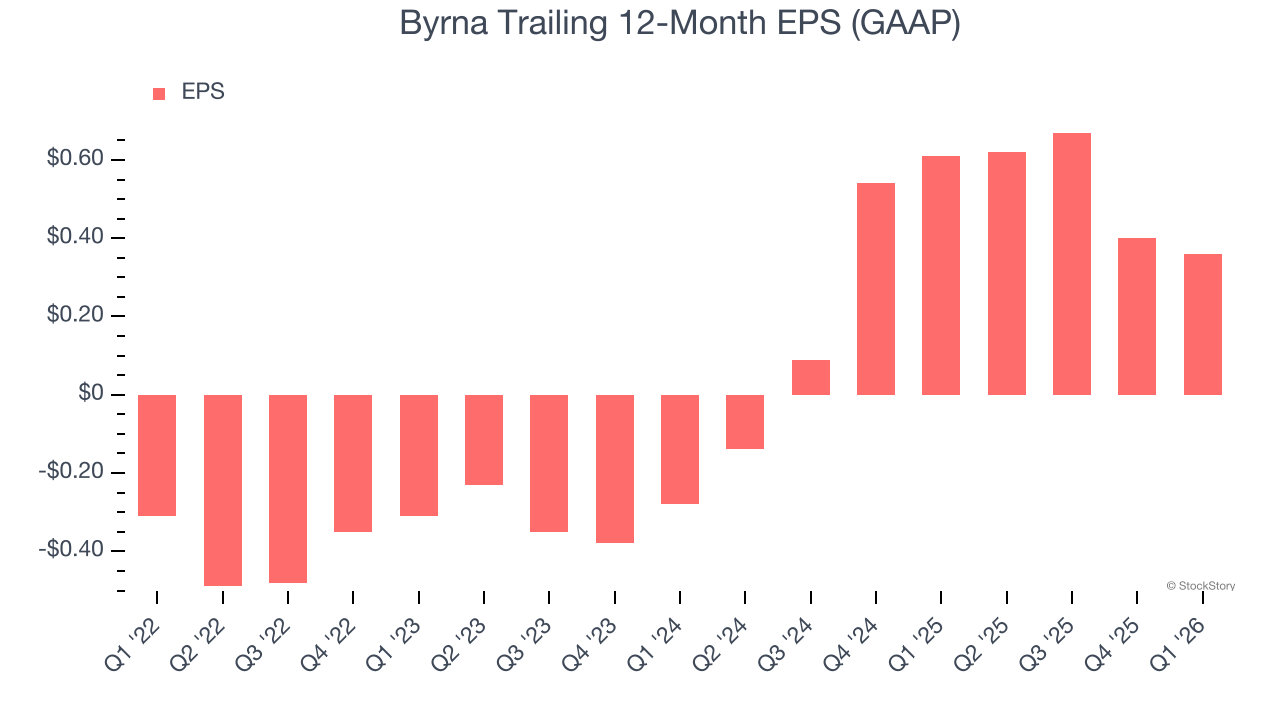

- EPS (GAAP): $0.03 vs analyst expectations of $0.07 (57.1% miss)

- Adjusted EBITDA: $2.21 million vs analyst estimates of $3.33 million (7.6% margin, 33.6% miss)

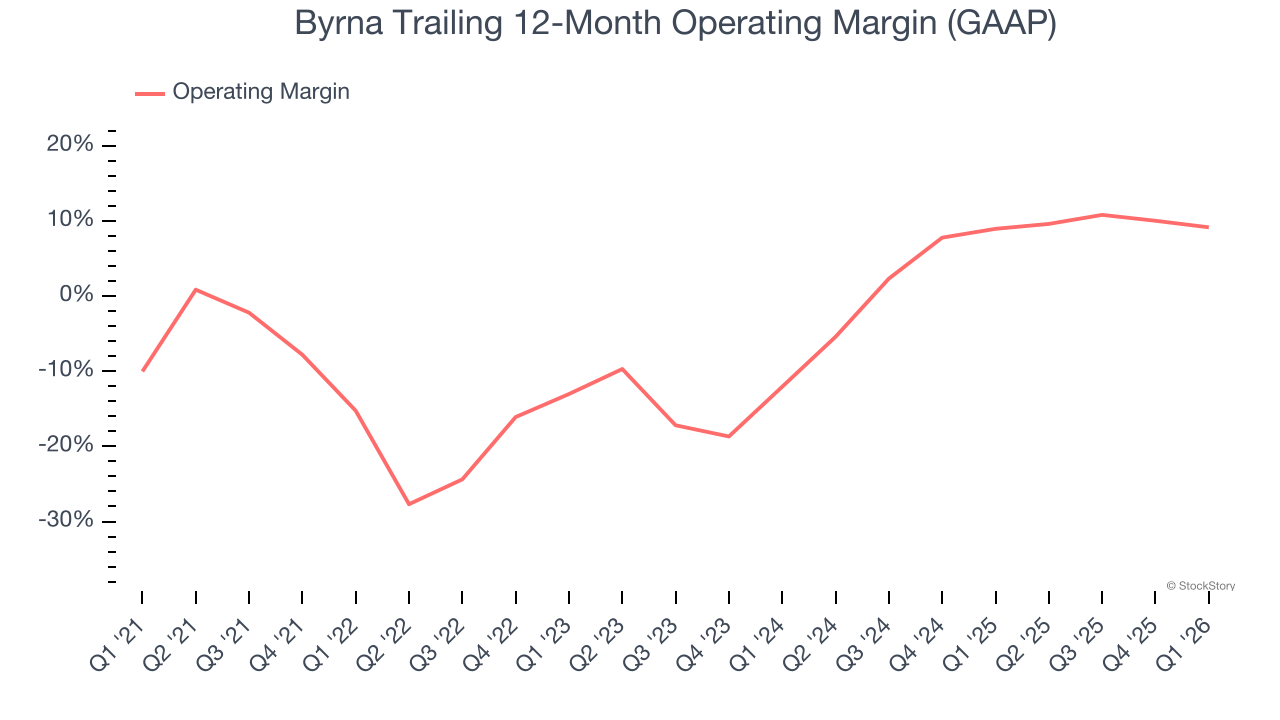

- Operating Margin: 3.2%, down from 6.5% in the same quarter last year

- Market Capitalization: $208.6 million

Management CommentaryByrna CEO Conn Davis stated: “Byrna has important strengths already in place, including a differentiated product offering, a strong balance sheet, a domestic manufacturing footprint, and a growing retail and dealer presence. At the same time, it is clear to me that the next phase of value creation will be defined by sharper execution across marketing, e-commerce, retail productivity, and operating discipline. That is where our focus is today.

Company Overview

Providing civilians with tools to disable, disarm, and deter would-be assailants, Byrna (NASDAQ: BYRN) is a provider of non-lethal weapons.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Luckily, Byrna’s sales grew at an incredible 36.7% compounded annual growth rate over the last five years. Its growth beat the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Byrna’s annualized revenue growth of 54.2% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Byrna’s revenue grew by 10.9% year on year to $29.05 million but fell short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 13.5% over the next 12 months, a deceleration versus the last two years. Still, this projection is admirable and suggests the market is baking in success for its products and services.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Operating Margin

Byrna was roughly breakeven when averaging the last five years of quarterly operating profits, inadequate for an industrials business.

On the plus side, Byrna’s operating margin rose by 24.4 percentage points over the last five years, as its sales growth gave it immense operating leverage.

In Q1, Byrna generated an operating margin profit margin of 3.2%, down 3.3 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Byrna’s full-year EPS flipped from negative to positive over the last four years. This is a good sign and shows it’s at an inflection point.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Byrna, its two-year annual EPS growth of 81.3% was higher than its four-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q1, Byrna reported EPS of $0.03, down from $0.07 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from Byrna’s Q1 Results

We struggled to find many positives in these results. Its revenue missed and its EBITDA fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 4.2% to $8.85 immediately after reporting.

Byrna underperformed this quarter, but does that create an opportunity to invest right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).