While the broader market has struggled with the S&P 500 down 4.8% since September 2025, Provident Financial Services has surged ahead as its stock price has climbed by 7.9% to $20.80 per share. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is there a buying opportunity in Provident Financial Services, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is Provident Financial Services Not Exciting?

Despite the momentum, we're swiping left on Provident Financial Services for now. Here are three reasons why PFS doesn't excite us and a stock we'd rather own.

1. Projected Net Interest Income Growth Is Slim

Forecasted net interest income by Wall Street analysts signals a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Provident Financial Services’s net interest income to drop by 7.6%, a decrease from its 48.8% annualized growth for the past two years. This projection is below its 48.8% annualized growth rate for the past two years.

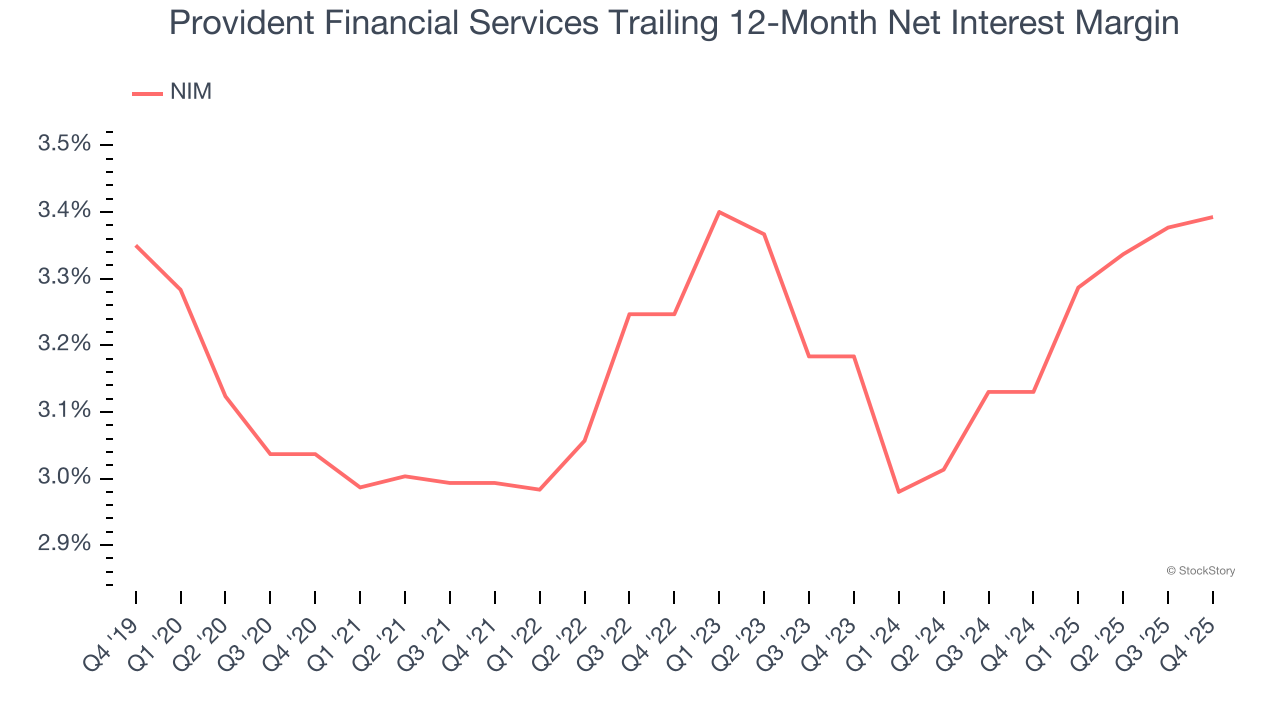

2. Low Net Interest Margin Reveals Weak Loan Book Profitability

The net interest margin (NIM) is a key profitability indicator that measures the difference between what a bank earns on its loans and what it pays on its deposits. This metric measures how efficiently one can generate income from its core lending activities.

Over the past two years, we can see that Provident Financial Services’s net interest margin averaged a subpar 3.3%, reflecting its high servicing and capital costs.

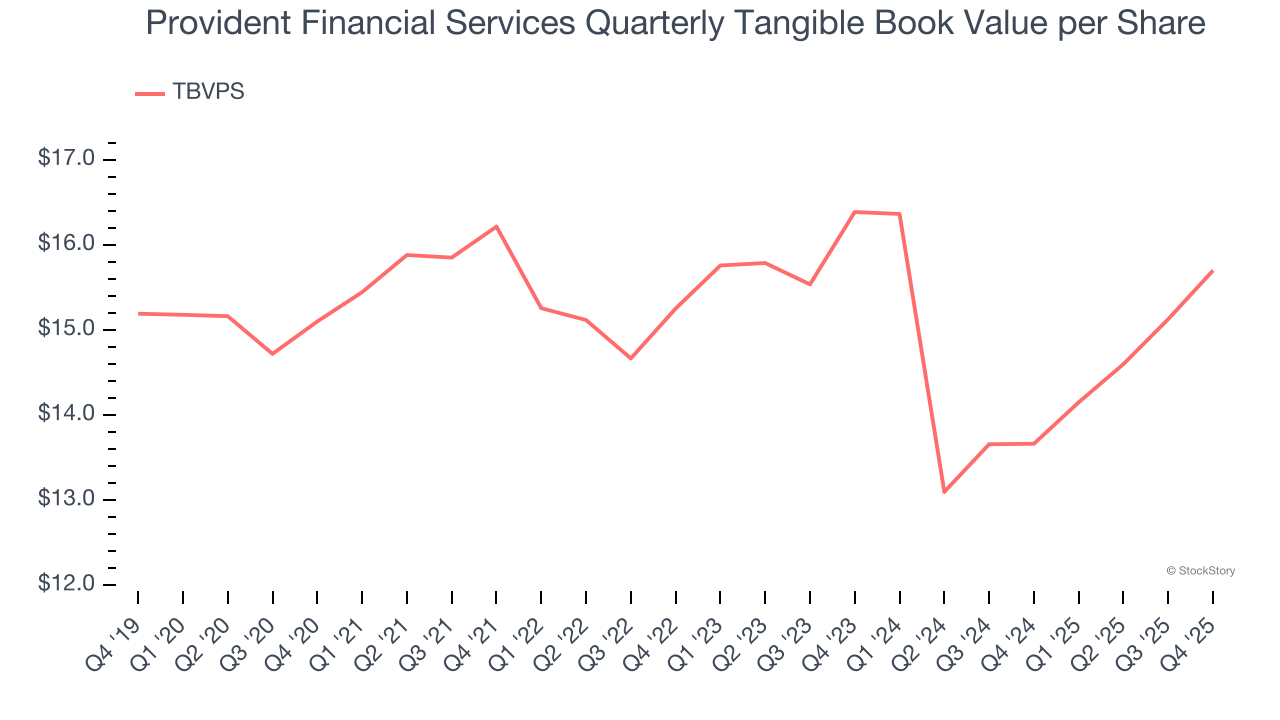

3. Declining TBVPS Reflects Erosion of Asset Value

In the banking industry, tangible book value per share (TBVPS) provides the clearest picture of shareholder value, as it focuses on concrete assets while excluding intangible items that may not hold value during challenging times.

Provident Financial Services’s TBVPS was flat over the last five years, and the past two years paint an even worse picture as TBVPS declined at a -2.1% annual clip (from $16.39 to $15.70 per share).

Final Judgment

Provident Financial Services isn’t a terrible business, but it doesn’t pass our bar. With its shares topping the market in recent months, the stock trades at 0.9× forward P/B (or $20.80 per share). This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're pretty confident there are more exciting stocks to buy at the moment. We’d recommend looking at one of our all-time favorite software stocks.

Stocks We Would Buy Instead of Provident Financial Services

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.