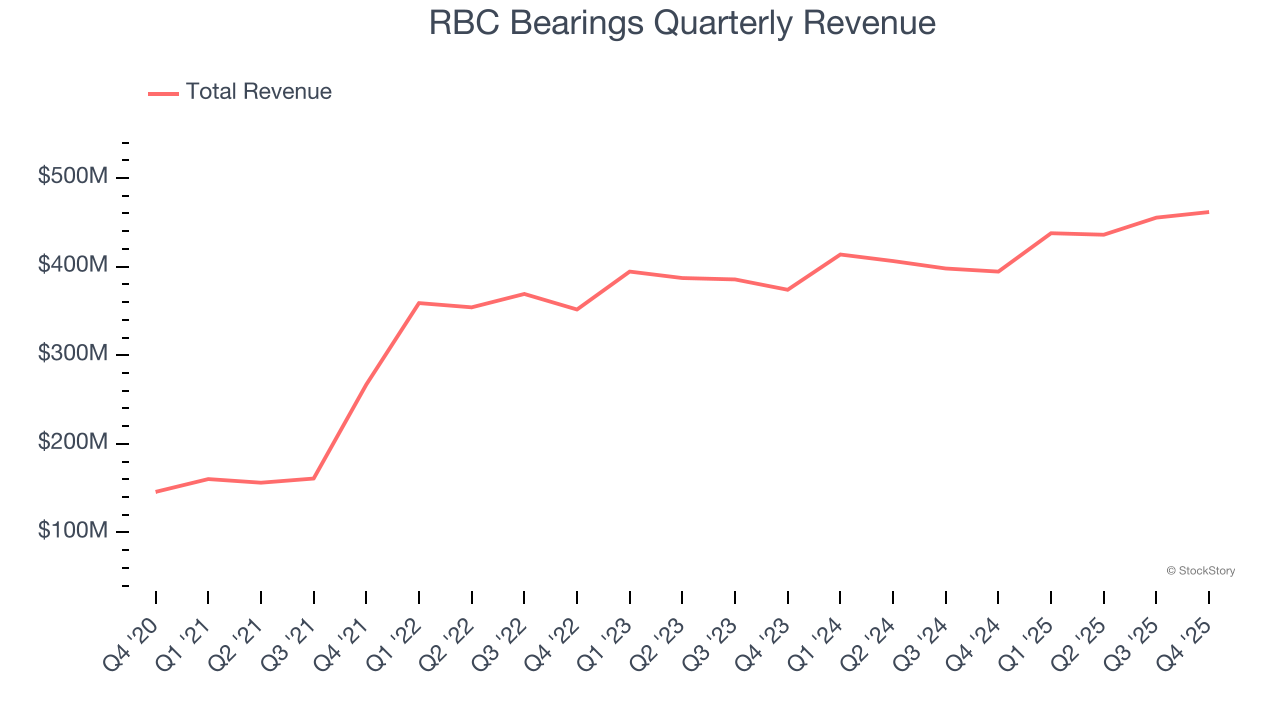

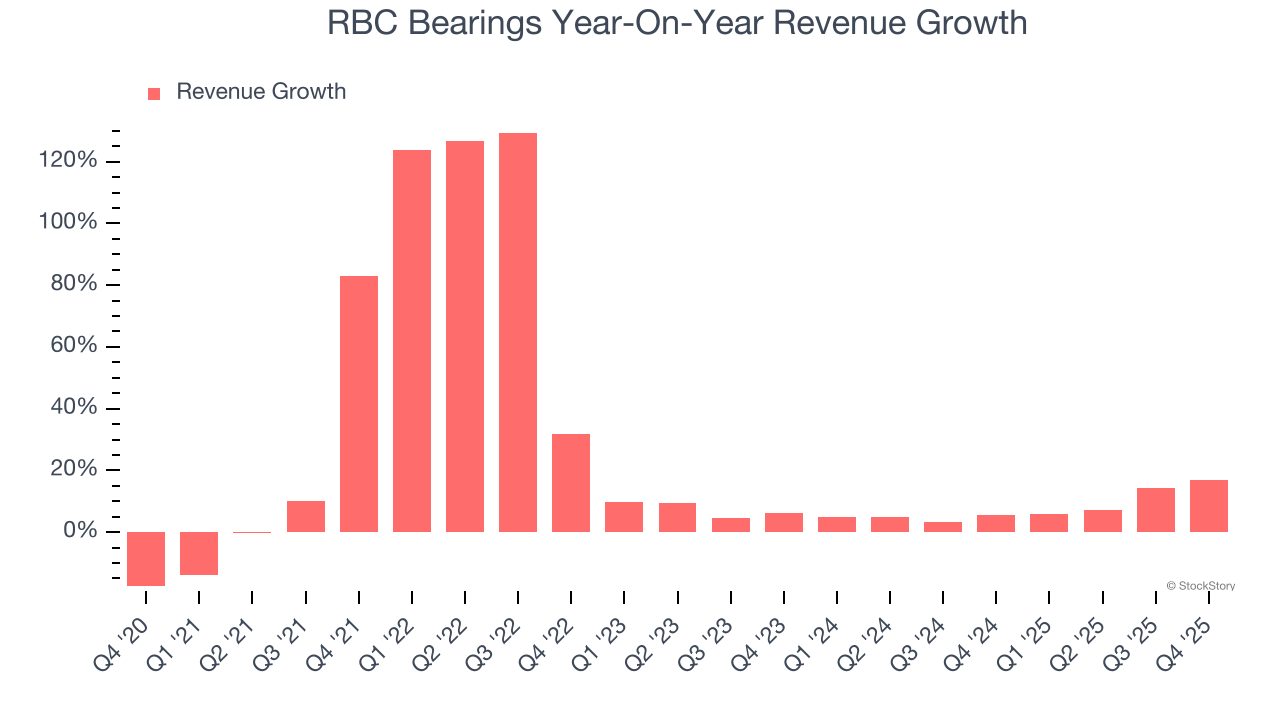

Bearings manufacturer RBC Bearings (NYSE: RBC) met Wall Street’s revenue expectations in Q4 CY2025, with sales up 17% year on year to $461.6 million. On the other hand, next quarter’s revenue guidance of $500 million was less impressive, coming in 1.6% below analysts’ estimates. Its non-GAAP profit of $3.04 per share was 6.2% above analysts’ consensus estimates.

Is now the time to buy RBC Bearings? Find out by accessing our full research report, it’s free.

RBC Bearings (RBC) Q4 CY2025 Highlights:

- Revenue: $461.6 million vs analyst estimates of $460.3 million (17% year-on-year growth, in line)

- Adjusted EPS: $3.04 vs analyst estimates of $2.86 (6.2% beat)

- Adjusted EBITDA: $149.6 million vs analyst estimates of $143.6 million (32.4% margin, 4.2% beat)

- Revenue Guidance for Q1 CY2026 is $500 million at the midpoint, below analyst estimates of $508 million

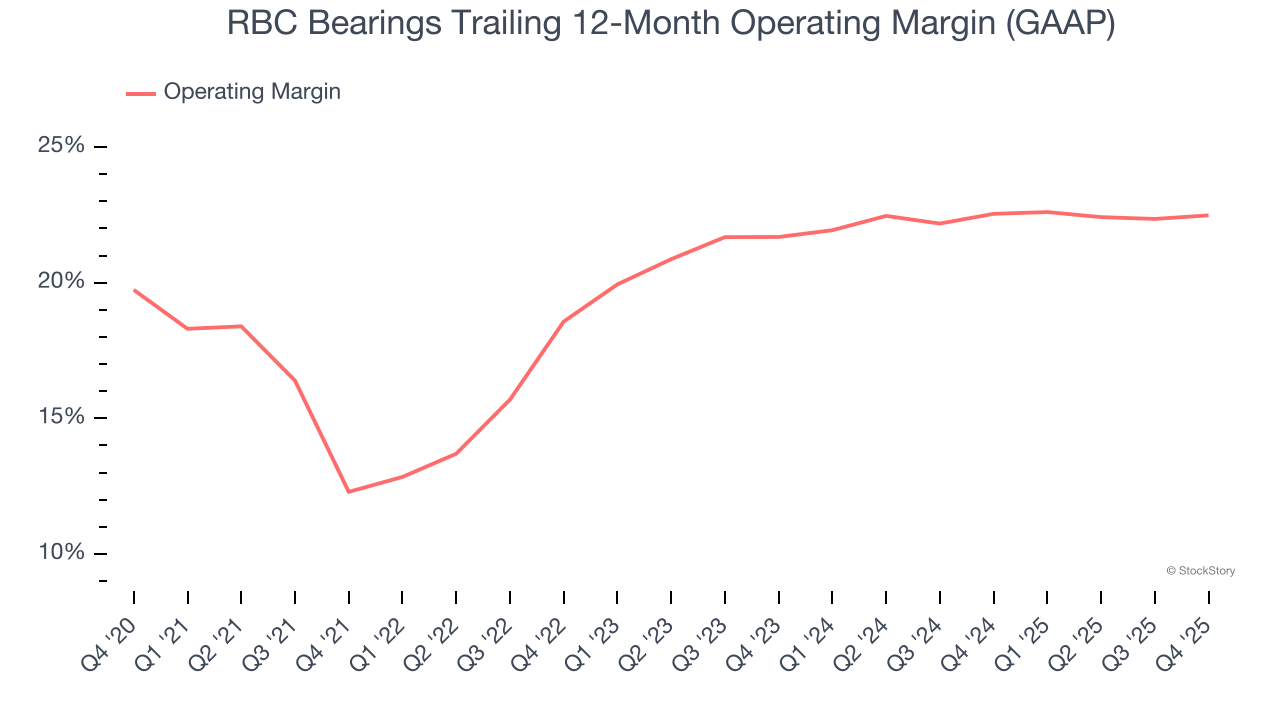

- Operating Margin: 22.3%, in line with the same quarter last year

- Free Cash Flow Margin: 21.5%, up from 18.7% in the same quarter last year

- Market Capitalization: $16.27 billion

Dr. Michael J. Hartnett, Chairman and Chief Executive Officer, stated, “We are pleased that we were able to deliver another strong quarter of results, driven by continued momentum in our Aerospace & Defense business and steady performance in our Industrial business. We are well-positioned for growth in calendar year 2026 and beyond, given our robust, growing backlog, which has continued to benefit from recent contract wins within the A&D space. As we look ahead, we are continuing to remain focused on strategic, profitable growth, increasing our production capacity, and delivering strong free cash flow that will help create long-term value for all our stakeholders. I would like to thank our employees for their continued dedication and disciplined execution, which has been key in helping deliver the strong performance we have achieved over the past several quarters that has positioned RBC for a record year.”

Company Overview

With a Guinness World Record for engineering the largest spherical plain bearing, RBC Bearings (NYSE: RBC) is a manufacturer of bearings and related components for the aerospace & defense, industrial, and transportation industries.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, RBC Bearings’s 23.1% annualized revenue growth over the last five years was incredible. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. RBC Bearings’s annualized revenue growth of 7.8% over the last two years is below its five-year trend, but we still think the results were respectable.

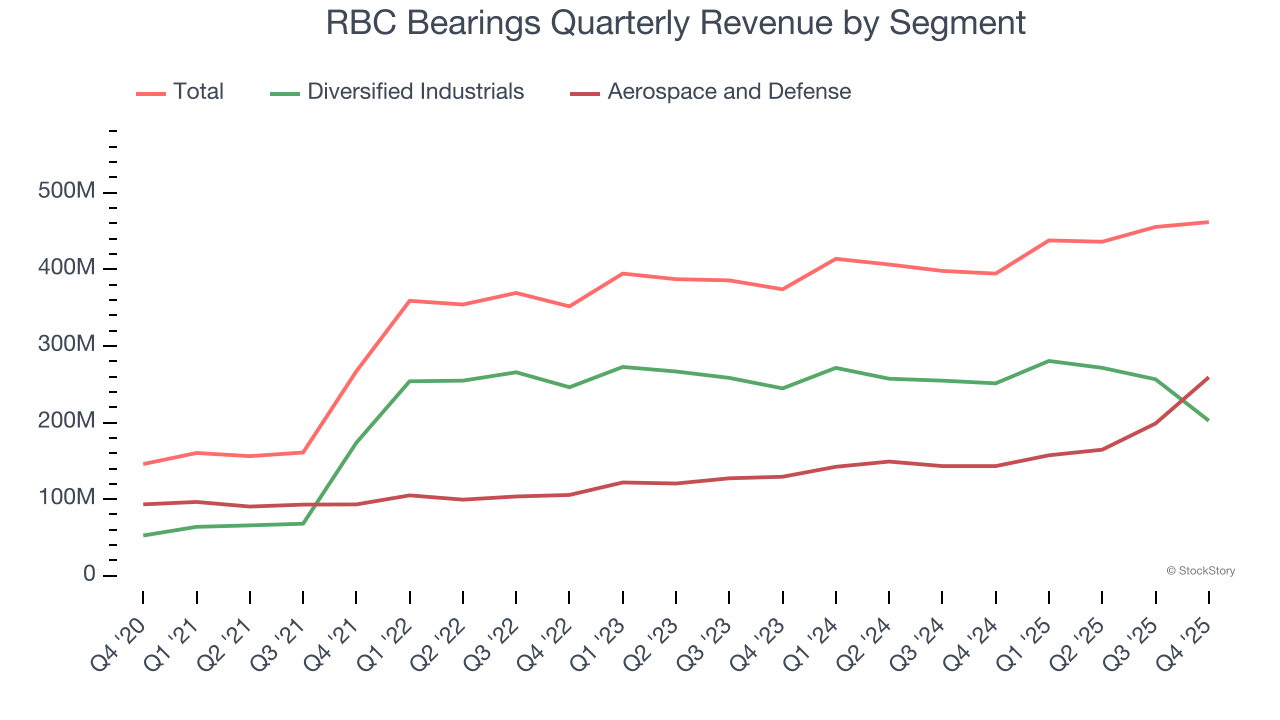

We can better understand the company’s revenue dynamics by analyzing its most important segments, Diversified Industrials and Aerospace and Defense, which are 43.9% and 56.1% of revenue. Over the last two years, RBC Bearings’s Diversified Industrials revenue (general industrial equipment) averaged 1.6% year-on-year declines. On the other hand, its Aerospace and Defense revenue (aircraft equipment, radar, missiles) averaged 25.6% growth.

This quarter, RBC Bearings’s year-on-year revenue growth was 17%, and its $461.6 million of revenue was in line with Wall Street’s estimates. Company management is currently guiding for a 14.2% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 12.8% over the next 12 months, an improvement versus the last two years. This projection is commendable and implies its newer products and services will spur better top-line performance.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

RBC Bearings has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 20.5%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, RBC Bearings’s operating margin rose by 10.2 percentage points over the last five years, as its sales growth gave it immense operating leverage.

In Q4, RBC Bearings generated an operating margin profit margin of 22.3%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

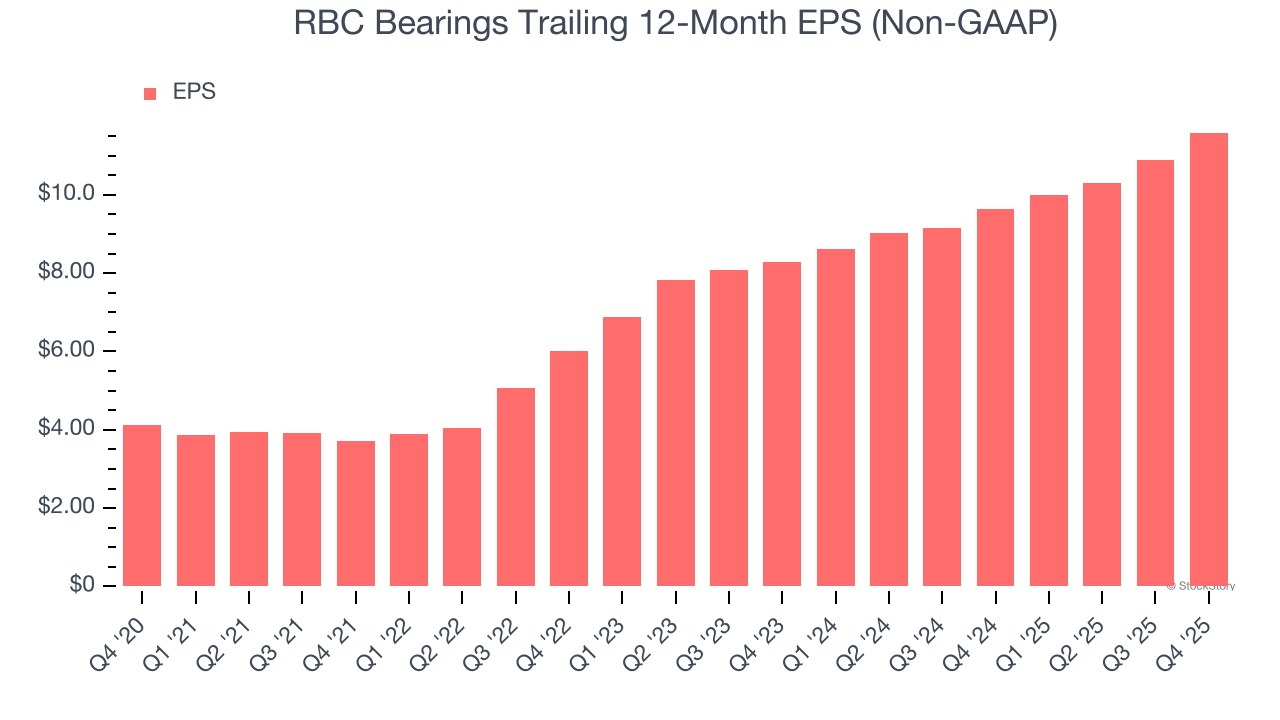

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

RBC Bearings’s astounding 23% annual EPS growth over the last five years aligns with its revenue performance. This tells us its incremental sales were profitable.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

RBC Bearings’s two-year annual EPS growth of 18.3% was fantastic and topped its 7.8% two-year revenue growth.

We can take a deeper look into RBC Bearings’s earnings to better understand the drivers of its performance. While we mentioned earlier that RBC Bearings’s operating margin was flat this quarter, a two-year view shows its margin has expanded. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, RBC Bearings reported adjusted EPS of $3.04, up from $2.34 in the same quarter last year. This print beat analysts’ estimates by 6.2%. Over the next 12 months, Wall Street expects RBC Bearings’s full-year EPS of $11.59 to grow 14.1%.

Key Takeaways from RBC Bearings’s Q4 Results

We were impressed by how significantly RBC Bearings blew past analysts’ Aerospace and Defense revenue expectations this quarter. We were also glad its EBITDA outperformed Wall Street’s estimates. On the other hand, its Diversified Industrials revenue missed and its revenue guidance for next quarter fell short of Wall Street’s estimates. Overall, this print was mixed but still had some key positives. The market seemed to be hoping for more, and the stock traded down 5% to $491.00 immediately after reporting.

Is RBC Bearings an attractive investment opportunity at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).