Looking back on analog semiconductors stocks’ Q3 earnings, we examine this quarter’s best and worst performers, including Vishay Intertechnology (NYSE: VSH) and its peers.

Demand for analog chips is generally linked to the overall level of economic growth, as analog chips serve as the building blocks of most electronic goods and equipment. Unlike digital chip designers, analog chip makers tend to produce the majority of their own chips, as analog chip production does not require expensive leading edge nodes. Less dependent on major secular growth drivers, analog product cycles are much longer, often 5-7 years.

The 15 analog semiconductors stocks we track reported a satisfactory Q3. As a group, revenues beat analysts’ consensus estimates by 0.8% while next quarter’s revenue guidance was 7,676% above.

In light of this news, share prices of the companies have held steady as they are up 2.8% on average since the latest earnings results.

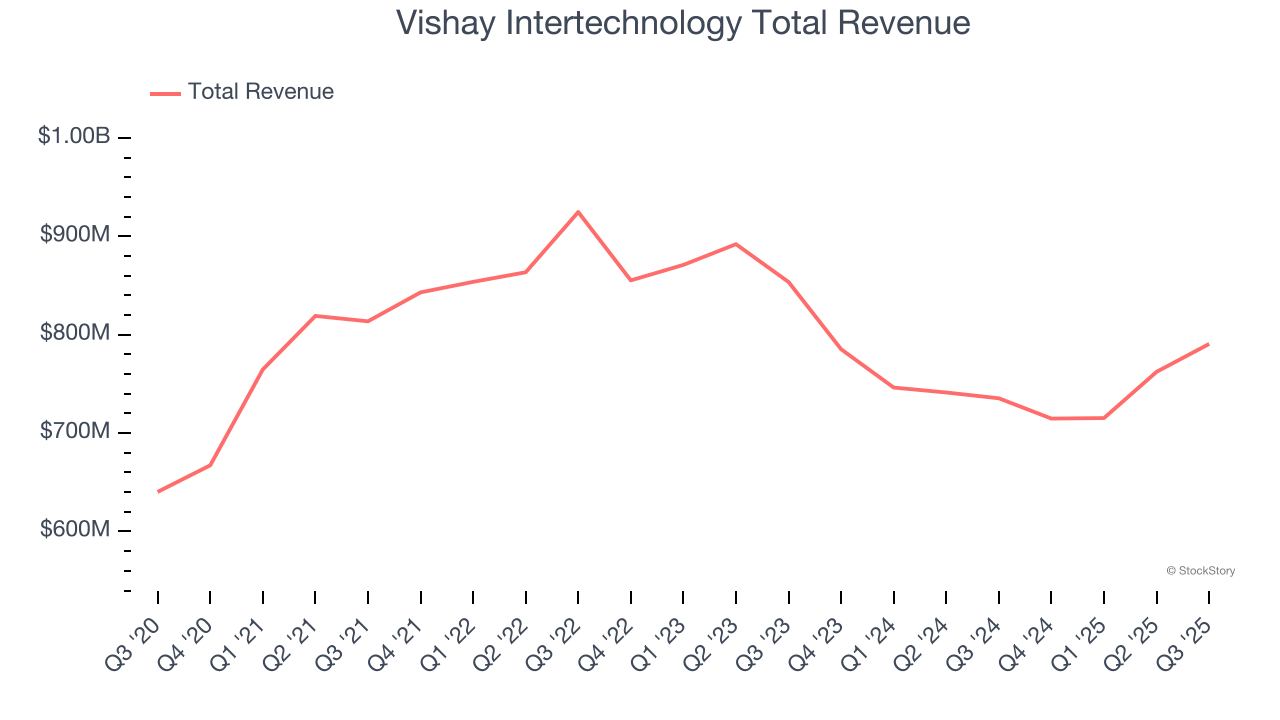

Vishay Intertechnology (NYSE: VSH)

Named after the founder's ancestral village in present-day Lithuania, Vishay Intertechnology (NYSE: VSH) manufactures simple chips and electronic components that are building blocks of virtually all types of electronic devices.

Vishay Intertechnology reported revenues of $790.6 million, up 7.5% year on year. This print exceeded analysts’ expectations by 1.2%. Despite the top-line beat, it was still a mixed quarter for the company with a solid beat of analysts’ adjusted operating income estimates but EPS in line with analysts’ estimates.

“Our third quarter revenue growth demonstrates Vishay’s alignment with high growth markets including smart grid infrastructure, AI related power requirements, automotive and aerospace/defense while the market overall continues to gradually recover,” said Joel Smejkal, president and CEO.

The market was likely pricing in the results, and the stock is flat since reporting. It currently trades at $16.17.

Is now the time to buy Vishay Intertechnology? Access our full analysis of the earnings results here, it’s free.

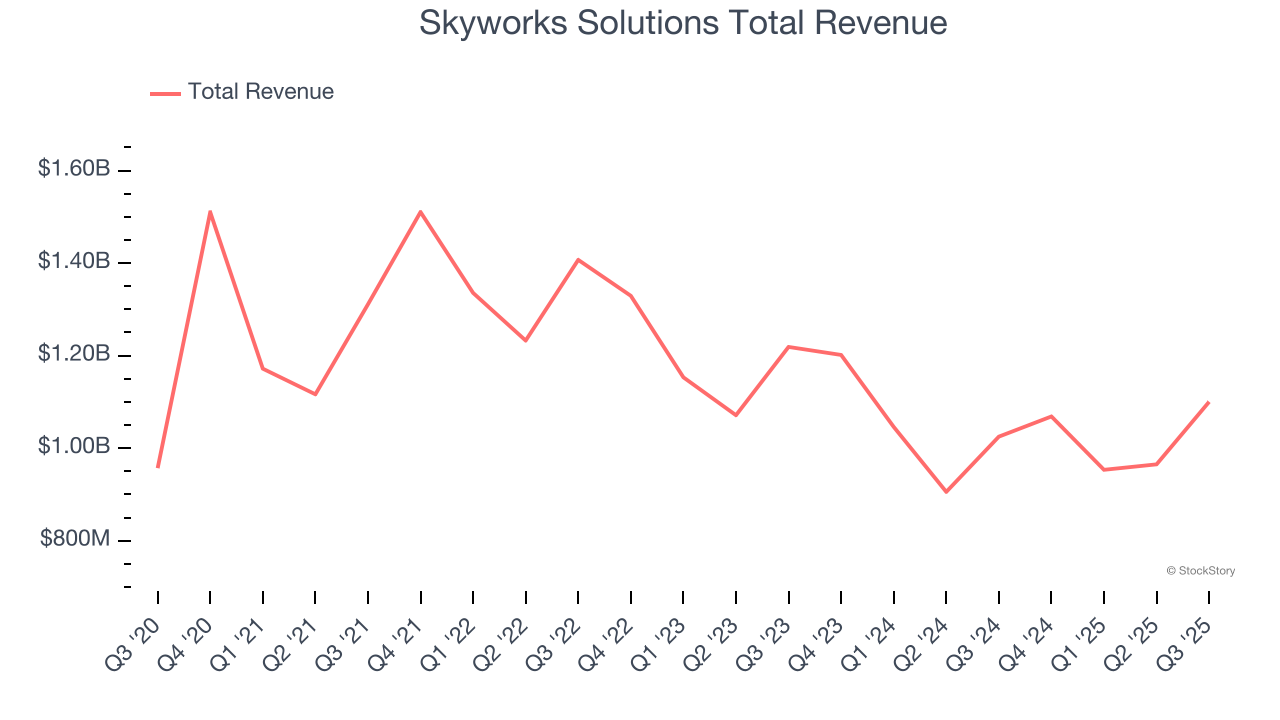

Best Q3: Skyworks Solutions (NASDAQ: SWKS)

Result of a merger of Alpha Industries and the wireless communications division of Conexant, Skyworks Solutions (NASDAQ: SWKS) is a designer and manufacturer of chips used in smartphones, autos, and industrial applications to amplify, filter, and process wireless signals.

Skyworks Solutions reported revenues of $1.1 billion, up 7.3% year on year, outperforming analysts’ expectations by 5.4%. The business had a stunning quarter with a beat of analysts’ EPS estimates and revenue guidance for next quarter exceeding analysts’ expectations.

Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 15.5% since reporting. It currently trades at $60.82.

Is now the time to buy Skyworks Solutions? Access our full analysis of the earnings results here, it’s free.

Weakest Q3: Universal Display (NASDAQ: OLED)

Serving major consumer electronics manufacturers, Universal Display (NASDAQ: OLED) is a provider of organic light emitting diode (OLED) technologies used in display and lighting applications.

Universal Display reported revenues of $139.6 million, down 13.6% year on year, falling short of analysts’ expectations by 15.9%. It was a disappointing quarter as it posted a significant miss of analysts’ revenue estimates and a significant miss of analysts’ adjusted operating income estimates.

Universal Display delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 8.1% since the results and currently trades at $124.51.

Read our full analysis of Universal Display’s results here.

Analog Devices (NASDAQ: ADI)

Founded by two MIT graduates, Ray Stata and Matthew Lorber in 1965, Analog Devices (NASDAQ: ADI) is one of the largest providers of high performance analog integrated circuits used mainly in industrial end markets, along with communications, autos, and consumer devices.

Analog Devices reported revenues of $3.08 billion, up 25.9% year on year. This number surpassed analysts’ expectations by 2.1%. It was a strong quarter as it also produced revenue guidance for next quarter beating analysts’ expectations and a decent beat of analysts’ revenue estimates.

The stock is up 25% since reporting and currently trades at $299.14.

Read our full, actionable report on Analog Devices here, it’s free.

Sensata Technologies (NYSE: ST)

Originally a temperature sensor control maker and a subsidiary of Texas Instruments for 60 years, Sensata Technology Holdings (NYSE: ST) is a leading supplier of analog sensors used in industrial and transportation applications, best known for its dominant position in the tire pressure monitoring systems in cars.

Sensata Technologies reported revenues of $932 million, down 5.2% year on year. This print topped analysts’ expectations by 1.1%. Taking a step back, it was a mixed quarter as it also logged a beat of analysts’ EPS estimates but revenue guidance for next quarter slightly missing analysts’ expectations.

The stock is up 14.2% since reporting and currently trades at $35.22.

Read our full, actionable report on Sensata Technologies here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.