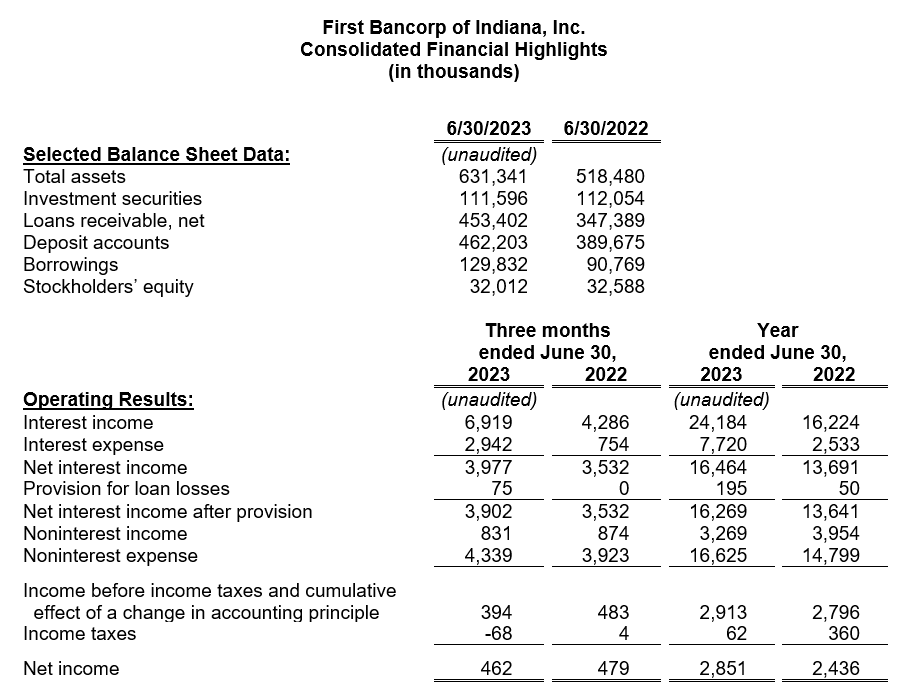

EVANSVILLE, Ind. - Aug. 5, 2023 - PRLog -- First Bancorp of Indiana, Inc. (OTCPK:FBPI), the holding company (the Company) for First Federal Savings Bank (the Bank), reported earnings of $462,000 ($0.28 per diluted common share) for the fourth fiscal quarter ended June 30, 2023, compared to $479,000 ($0.28 per diluted common share) for the same quarter a year ago. Earnings for Fiscal 2023 totaled $2.85 million ($1.70 per diluted common share), compared to $2.44 million ($1.40 per diluted common share) last fiscal year. Earnings for the twelve-month period yield a return on average assets (ROA) of 0.50% and a return on average equity (ROE) of 9.07%. This compares to an annualized ROA of 0.51% and an annualized ROE of 6.35% for Fiscal 2022.

Net interest income for the 2023 fiscal year was 20.3% higher than the previous year. Improved yields on earning assets, thanks to the higher interest rates on newly originated and variable rate loans and investments, were compounded by balance sheet growth. Conversely, funding costs have also risen in recent quarters as depositors migrated to higher-yielding CD products. The Company's Net Interest Margin (NIM), as a percentage of average interest-earning assets, was 2.85% for the current quarter and 3.13% for the fiscal year ending June 30, 2023. Noninterest income was reduced for the same timeframe, primarily by lower gains on loan sales. Total noninterest expense was 12.3% higher year over year – predominantly increased personnel costs, occupancy expenses, and FDIC insurance premiums between the comparative periods. The bank's efficiency ratio for Fiscal 2023 improved to 77.8% from 80.3% last fiscal year.

"As we close the books on one fiscal year, we appreciate the confidence that our customers have placed in us, as demonstrated by the significant balance sheet growth," stated Michael H. Head, President and CEO. "We expanded the Bank's geographic footprint to reach new markets and offered new technologies and attentive customer service to grow existing relationships. We usher in the new fiscal year with optimism and plan to increase those ties."

During the prior fiscal year, the board of directors approved a leveraging strategy to increase earnings. The elevated deposit and liquidity levels at that time were utilized to increase investment securities holdings and meet loan demand. Proceeds from the Company's $12 million subordinated debt offering and wholesale deposits acquired by the Bank funded additional growth. The securities portfolio, primarily composed of investment-grade municipal bonds or obligations of US government agencies, totaled $111.6 million on June 30, 2023.

Despite the rising interest rate environment, net loans outstanding have increased $106.0 million, or 30.5%, during the fiscal year. The $453.4 million of net loans on June 30, 2023, included $2.6 million of loans committed for sale to either Fannie Mae or the Federal Home Loan Bank (FHLB).

Loan origination volume for the twelve months ended June 30, 2023, increased 29.1% year over year. Commercial loan production, including $12.9 million participated with other banks, rose to $102.1 million for the period. Single-family mortgage loan production totaled $86.0 million during the same timeframe. A lack of housing supply in the local market has been largely offset by increased housing construction activity. Consumer lending originations, which included auto loans, personal loans, and home equity loans and lines of credit, added $22.3 million.

Despite an uptick in nonperforming loans on June 30, 2023, charged off loans totaled less than $1,000 for the quarter, and a net recovery was recorded for the fiscal year. The ratio of nonperforming loans 90 days or more delinquent to total loans was 0.53% on June 30, 2023, compared to 0.13% a year ago. Due to growth in the loan portfolio, $195,000 of provisions for loan losses were recorded during the fiscal year. The allowance for loan losses, at $3.69 million, represented 0.85% of at-risk loans. Although management believes that the allowance is adequate, a slowing economy, removal of government stimulus, and persistent inflation may have an adverse effect on the credit quality of our loan portfolio. Management remains in close contact with our most vulnerable borrowers and will make additional provisions to the allowance, as necessary.

Deposit accounts, totaling $462.2 million on June 30, 2023, have increased 18.6% since the beginning of the fiscal year. Competition for funding, both in local markets and at the wholesale level, has driven deposit rates higher and pushed the Bank's cost of deposits to an annualized 1.19% for the year. Similarly, the Company's total cost of funds, including higher-costing FHLB advances and debt of the holding company, increased to an annualized 1.47% for the fiscal year ended June 30, 2023.

As a part of the Bank's Liquidity Management Plan, contingency funding sources are maintained, and liquidity stress scenarios are reviewed. First Federal Savings Bank maintains lines of credit at multiple institutions and additional borrowing capacity at FHLB. The Bank also has access to, but has not utilized, the Federal Reserve's discount window and the Bank Term Funding Program.

Stockholders' equity totaled $32.0 million on June 30, 2023, which includes a $10.5 million fair value reduction to the available for sale securities portfolio given the rapid rise in market interest rates. Notably, this adjustment is excluded from regulatory capital calculations, and gains or losses are only realized if a security is sold. Based on the 1,672,429 outstanding common shares on June 30, 2023, the book value per share of FBPI stock was $19.14. Shareholders were rewarded with a 3.23% increase in the quarterly dividend rate, beginning with the September 2022 dividend, and 27,987 shares of treasury stock were repurchased during the fiscal year.

On June 30, 2023, First Federal Savings Bank's Community Bank Leverage Ratio (CBLR) was 8.72%. The Bank comfortably exceeds the applicable regulatory standards to be considered "well-capitalized".

This news release may contain forward-looking statements within the meaning of the federal securities laws. Statements in this release that are not strictly historical are forward-looking and are based upon current expectations that may differ materially from actual results. These forward-looking statements, identified by words such as "will," "expected," "believe," and "prospects," involve risks and uncertainties that could cause actual results to differ materially from those anticipated by the statements made herein. These risks and uncertainties involve general economic trends and changes in interest rates, increased competition, changes in consumer demand for financial services, the possibility of unforeseen events affecting the industry generally, the uncertainties associated with newly developed or acquired operations, market disruptions and the potential effects of the COVID-19 pandemic on the local and national economic environment, on our customers and on our operations as well as any changes to federal, state and local government laws, regulations and orders in connection with the pandemic. The Company undertakes no obligation to release revisions to these forward-looking statements publicly to reflect events or circumstances after the date hereof or to reflect the occurrence of unforeseen events, except as required to be reported by applicable law.

Photos: (Click photo to enlarge)

Source: First Bancorp of Indiana Inc (OTCPK:FBPI)

Read Full Story - First Bancorp of Indiana, Inc. Announces Financial Results June 2023 | More news from this source

Press release distribution by PRLog