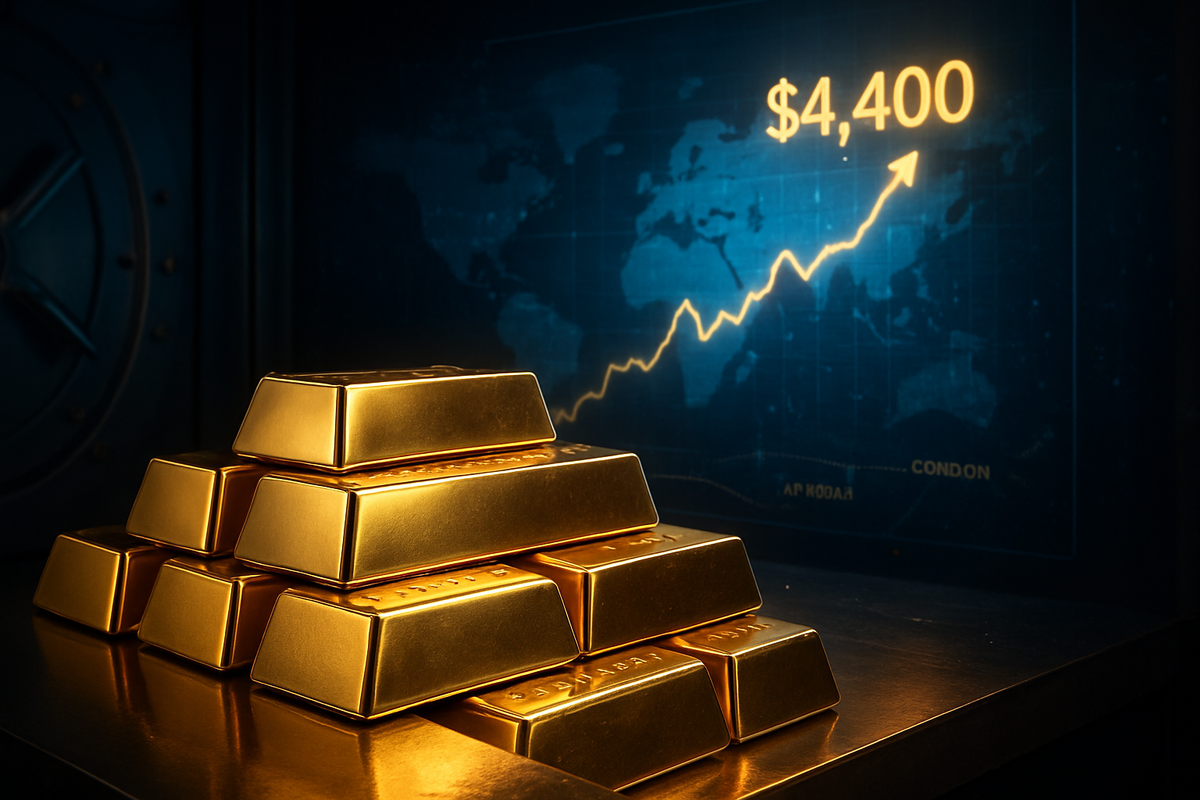

On December 22, 2025, the global financial landscape reached a psychological and economic tipping point as gold prices surged past the historic $4,400 per ounce mark. This monumental rally, representing a nearly 70% increase since the beginning of the year, is no longer being dismissed by analysts as a mere "fear trade." Instead, it is being hailed as the definitive signal of a structural shift in global monetary sentiment, reflecting a profound loss of confidence in traditional fiat currencies and a re-evaluation of long-term inflation expectations.

The immediate implications of this surge are being felt across the globe, from the halls of the Federal Reserve to the trading floors of Shanghai. As the U.S. dollar’s dominance faces its most significant challenge in decades, the "debasement trade" has moved from the fringes of macroeconomics to the center of institutional portfolio strategy. With gold now firmly established as a $4,400 asset, the market is pricing in a future where "hard money" is once again the cornerstone of the international financial system.

The Perfect Storm: A Timeline of the Ascent to $4,400

The journey to $4,400 was not an overnight phenomenon but the result of a "perfect storm" of fiscal fragility and geopolitical realignment. The rally began in earnest in October 2024, when gold set a then-record of $2,792 amid U.S. election uncertainty and escalating tensions in the Middle East. By April 2025, the metal breached the $3,000 level following a symbolic but impactful downgrade of U.S. sovereign debt by major rating agencies, who cited the ballooning $38 trillion federal debt and the unsustainable cost of servicing it.

The momentum accelerated in the second half of 2025 as the BRICS nations—led by China and India—aggressively expanded their gold reserves. The People’s Bank of China (PBoC) has been a relentless buyer, treating gold as a strategic shield against potential Western sanctions and currency volatility. By October 2025, a seven-day U.S. government shutdown acted as the final catalyst, pushing gold past $4,000. The current peak of $4,412 reached today follows a dovish pivot by the Federal Reserve, which has signaled that interest rate cuts are likely in 2026 to combat cooling labor data, even as "sticky" inflation persists in the energy and services sectors.

Initial market reactions have been a mix of euphoria and caution. While retail investors have flooded into gold-backed ETFs, institutional desks are grappling with the reality that gold is no longer just a hedge—it is becoming a primary reserve asset. The "fear premium" has been replaced by a "solvency premium," as investors look past short-term interest rate fluctuations and focus on the long-term purchasing power of the dollar.

Winners and Losers in the Era of Hard Money

The dramatic rise in bullion has created a sharp divide in the corporate world, distinguishing those who control the supply from those who depend on it as a raw material. The primary winners are the senior mining giants, led by Newmont (NYSE: NEM). As the world’s largest producer, Newmont has seen its margins explode; while its All-In Sustaining Costs (AISC) have risen modestly due to energy inflation, the gap between production costs and the $4,400 spot price has generated record-breaking free cash flow. Similarly, Barrick Gold (NYSE: GOLD) and Agnico Eagle Mines (NYSE: AEM) have become darlings of the S&P 500, with Agnico Eagle particularly noted for maintaining one of the lowest cost profiles in the industry, allowing its profits to outpace the gold rally itself.

Royalty and streaming companies have arguably fared even better. Firms like Franco-Nevada (NYSE: FNV) and Wheaton Precious Metals (NYSE: WPM) have enjoyed the full upside of the price surge without the operational risks of mining inflation. Because these companies own rights to a percentage of a mine’s production for a fixed or minimal cost, their business models have become "cash-flow machines" in this high-price environment.

Conversely, the "losers" are found in sectors where gold is a non-negotiable input. Jewelry giant Signet Jewelers (NYSE: SIG), the parent company of Kay and Zales, has struggled with "sticker shock" among mid-market consumers, forcing a pivot toward lab-grown alternatives and lower-karat alloys. In the technology sector, the impact is more subtle but equally pervasive. Apple (NASDAQ: AAPL) and Nvidia (NASDAQ: NVDA) use gold in high-performance semiconductors and AI server components for its superior conductivity. While the amount per unit is small, the aggregate cost across millions of devices is beginning to weigh on hardware margins. Industrial conglomerates like Panasonic (OTC: PCRFY) have already reported profit headwinds, as they find it increasingly difficult to pass the soaring costs of precious metals used in printed circuit boards (PCBs) onto the end consumer.

A Structural Shift: Comparing 2025 to the 1970s

To understand the significance of $4,400 gold, one must look back to the 1970s gold rush. However, the current environment is fundamentally different. While the 1970s rally was driven by cyclical inflation and oil shocks, the 2025 surge is rooted in structural de-dollarization. In 1971, the catalyst was the end of the gold standard; today, the catalyst is the perceived weaponization of the dollar and the unsustainable trajectory of U.S. fiscal policy.

This event fits into a broader trend of "multipolarity" in the global economy. The ripple effects are being felt by U.S. competitors and partners alike, as central banks move from a 1.5% gold allocation to nearly 3% or higher. This shift has significant regulatory and policy implications; we are seeing renewed discussions in Washington about "fiscal responsibility" and the potential for new digital currency frameworks that might incorporate "hard asset" backing to restore international trust.

Historically, gold rallies were often followed by sharp corrections when the Federal Reserve raised interest rates to double digits—the "Volcker moment." In 2025, however, the massive interest burden on the $38 trillion U.S. debt makes such high rates nearly impossible without triggering a sovereign default. This "fiscal dominance" means that gold has likely established a much higher permanent floor than in previous eras.

The Road to $5,000: What Comes Next?

In the short term, market participants should expect heightened volatility. After a 70% run, a period of consolidation is natural as some investors take profits. However, the long-term outlook remains overwhelmingly bullish. Major financial institutions, including Goldman Sachs and Bank of America, have already revised their 2026 targets upward to the $4,900–$5,000 range. The primary challenge for the market will be "inelastic supply"—it takes years to bring new gold mines online, and current production cannot keep pace with the surge in central bank demand.

Strategic pivots are already underway. Mining companies are expected to use their massive cash piles to initiate a new wave of Mergers and Acquisitions (M&A) to replenish their reserves. On the tech side, we may see an accelerated search for gold alternatives in industrial applications, though the metal’s unique chemical properties make it difficult to replace in high-end electronics. For the public, the "gold standard" is no longer a relic of history but a modern reality that will dictate everything from mortgage rates to the price of a smartphone.

Final Thoughts for the 2026 Investor

The breach of $4,400 gold is a watershed moment that marks the end of the "easy fiat" era. The key takeaway for investors is that the primary driver of gold is no longer just inflation—it is the systemic risk of a debt-saturated global economy. As we move into 2026, the market will be watching for any signs of a "BRICS currency" backed by gold or further downgrades of Western sovereign debt.

Moving forward, the significance of this event lies in the permanence of the shift. Gold has reclaimed its status as the ultimate arbiter of value. For the savvy investor, the coming months will require a focus on "quality" producers and royalty plays that can weather potential volatility while capturing the long-term upside of a world that is once again hungry for hard assets. The era of $4,400 gold is not just a peak; it is the new baseline for a changing global order.

This content is intended for informational purposes only and is not financial advice.