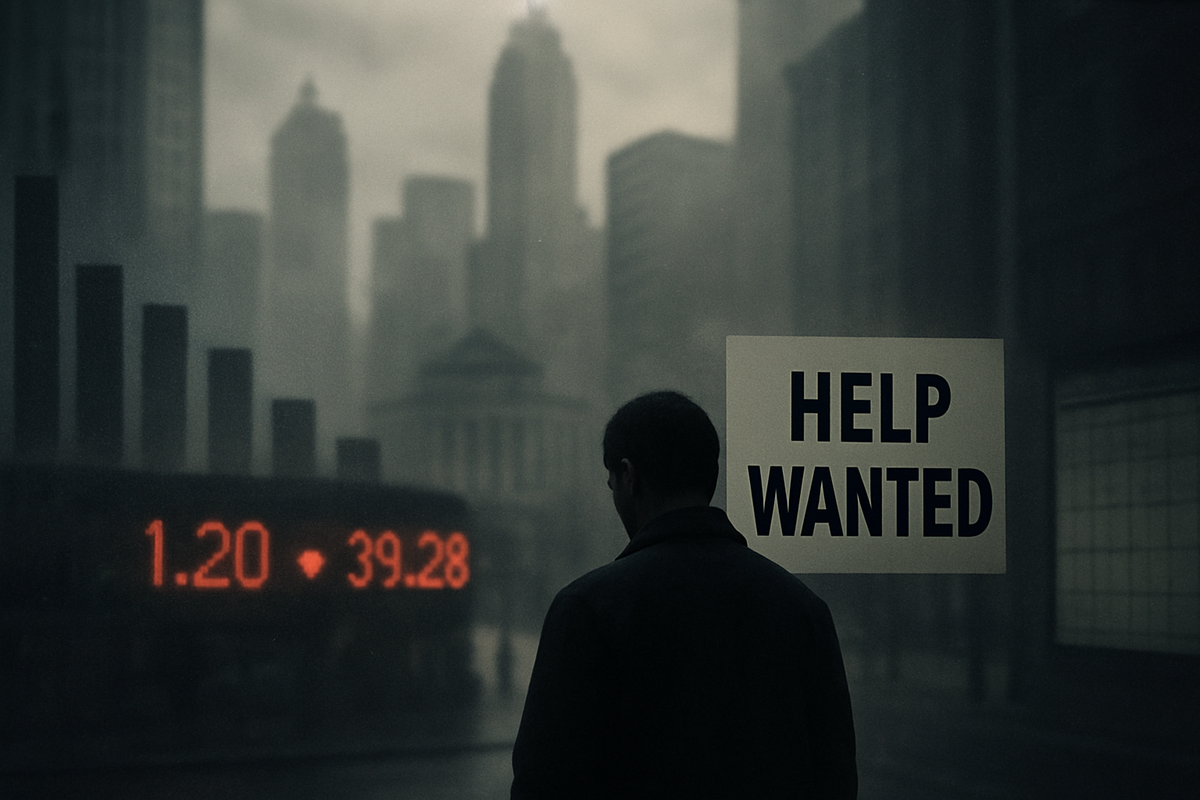

The financial markets are grappling with a turbulent period as recent labor market reports, particularly those reflecting October 2025 data, paint a picture of a weakening economy. With official government statistics delayed due to a federal shutdown, investors have been left to piece together a fragmented narrative from alternative data sources, which largely point to increasing job cuts, slowing hiring, and a potential uptick in the unemployment rate. This uncertainty has triggered a noticeable downturn in stock markets, influenced bond yields, and led to mixed currency movements, signaling a collective apprehension about the economic path ahead and the Federal Reserve's potential responses. The immediate implication for investors is a heightened need for caution and a re-evaluation of portfolio strategies in an environment increasingly leaning towards slower growth and potential monetary policy shifts.

A Fractured Picture: Decoding October's Labor Landscape Amidst Government Paralysis

The U.S. labor market entered a period of significant turbulence in October 2025, exacerbated by a federal government shutdown that commenced in early October. This shutdown critically impacted the release of official data from the U.S. Bureau of Labor Statistics (BLS), including the vital unemployment rate and non-farm payrolls report. As a result, market participants were forced to rely on a patchwork of private-sector reports and economic forecasts to gauge the health of the job market.

Estimates from various sources painted a concerning picture. The Chicago Federal Reserve suggested the unemployment rate likely rounded up to 4.4% in October, a notable increase from 4.35% in September and 4.3% in August, potentially marking the highest rate in four years. This uptick was attributed to a combination of slower hiring and an increase in layoffs. Further solidifying these fears, Challenger, Gray & Christmas reported a staggering 153,074 job cuts in October, a 175% increase from October 2024 and the highest October total since 2003. This report also highlighted that total job cuts for 2025 had surpassed 1 million through October, a level not seen since 2020. Conversely, the ADP National Employment Report, released on November 5, 2025, offered a glimmer of positive news, indicating a private-sector employment increase of 42,000 jobs in October, exceeding consensus expectations and marking the first monthly gain after two consecutive declines. However, this was overshadowed by more pessimistic outlooks, with Goldman Sachs estimating a decline of 50,000 in total U.S. nonfarm payrolls for October, a figure that would represent the largest monthly drop since late 2020.

The timeline leading up to this moment saw a gradual cooling in the labor market throughout the latter half of 2025, with job openings consistently declining to their lowest levels since 2021, according to data from Indeed. The federal shutdown, however, injected a new layer of uncertainty, delaying crucial official data that typically provides a clear direction for market sentiment and Federal Reserve policy. Key players involved in this evolving narrative include the Federal Reserve, closely monitoring economic indicators for its monetary policy decisions; the U.S. Department of Labor, responsible for collecting and disseminating official labor statistics; and various private economic research firms and consultancies whose alternative data became paramount during the official data blackout.

Initial market reactions were swift and largely negative. Wall Street experienced a significant tumble on November 6, 2025, with the S&P 500 (SPX) falling 1.1% and the tech-heavy Nasdaq Composite (IXIC) dropping 1.9%. This downturn was primarily driven by intensified fears of a slowing U.S. economy, fueled by the alarming job cut figures from Challenger, Gray & Christmas. Treasury yields generally declined as weaker job data firmed expectations for future interest rate cuts by the Federal Reserve, though some fluctuations were observed as news of a potential end to the government shutdown emerged. The U.S. dollar experienced mixed movements, initially finding some support from the absence of official data but later seeing a cautious rebound as investor expectations for a December rate cut began to wane slightly.

Corporate Crossroads: Winners and Losers in a Shifting Labor Landscape

The current labor market dynamics, characterized by rising unemployment and increasing job cuts, are poised to create distinct winners and losers across various corporate sectors. Companies highly sensitive to consumer spending and economic growth are likely to face significant headwinds, while those benefiting from cost-cutting measures or operating in more resilient industries may find opportunities.

On the losing side, consumer discretionary companies are particularly vulnerable. As job security diminishes and unemployment rises, consumer confidence typically wanes, leading to reduced spending on non-essential goods and services. Retailers, automotive manufacturers like General Motors (NYSE: GM) and Ford (NYSE: F), and hospitality chains such as Marriott International (NASDAQ: MAR) could see a significant slowdown in demand. Similarly, the housing market and related sectors, including construction companies like D.R. Horton (NYSE: DHI) and home improvement retailers like Home Depot (NYSE: HD), are likely to suffer from reduced consumer purchasing power and potentially tighter lending conditions as economic uncertainty persists. Furthermore, companies with high fixed costs and those heavily reliant on robust hiring, such as many technology firms that have recently undergone significant expansion, might face pressure to further streamline operations or implement hiring freezes, impacting their growth trajectories. The initial market reaction, with the Nasdaq Composite (IXIC) falling, underscores the vulnerability of the tech sector.

Conversely, some sectors and companies may find themselves in a relatively stronger position or even benefit from the economic climate. Companies offering essential goods and services in the consumer staples sector, such as Procter & Gamble (NYSE: PG) or Walmart (NYSE: WMT), tend to be more resilient during economic downturns as demand for their products remains relatively stable. The healthcare sector, including pharmaceutical giants like Johnson & Johnson (NYSE: JNJ) and medical device companies, also typically exhibits defensive characteristics. Furthermore, companies specializing in cost-cutting solutions, automation, or workforce management tools could see increased demand from businesses looking to optimize their operations in a challenging environment. Financial institutions, particularly those with strong balance sheets and diversified revenue streams, might navigate the turbulence better, though rising loan defaults could pose a risk. The shift in bond yields, signaling potential future rate cuts, could offer some relief to highly leveraged companies, but the overall economic slowdown presents a more dominant challenge.

Broader Implications: A Shifting Economic Paradigm

The current labor market downturn and the market's reaction are not isolated events but rather fit into a broader narrative of economic rebalancing following a period of post-pandemic recovery and inflationary pressures. This event highlights the ongoing struggle between persistent inflation and the Federal Reserve's aggressive monetary tightening, which now appears to be manifesting in a tangible slowdown in employment. The delayed official data due to the government shutdown further underscores the fragility of economic sentiment and the critical role of timely, transparent information in market stability.

The potential ripple effects on competitors and partners are significant. In a weakening demand environment, competition intensifies, potentially leading to price wars and reduced profit margins across industries. Supply chain partners, particularly those with less diversified client bases, could face reduced orders and increased financial strain. Regulatory or policy implications are also paramount. A sustained weakening of the labor market could increase pressure on the Federal Reserve to pivot towards more accommodative monetary policies, potentially halting rate hikes or even initiating cuts sooner than anticipated. This shift would have profound effects on borrowing costs, corporate investments, and asset valuations. Furthermore, the government shutdown itself highlights systemic risks related to political gridlock and its impact on economic data reliability, potentially prompting calls for reforms to ensure the continuity of essential economic reporting.

Historically, periods of significant job market weakening often precede broader economic slowdowns or recessions. Comparing the current situation to the early 2000s dot-com bust or the 2008 financial crisis, while not identical, offers valuable insights. In both instances, a deterioration in employment figures served as a leading indicator of deeper economic troubles, prompting significant policy responses. The current scenario, with a government shutdown adding a layer of complexity, presents a unique challenge, as the lack of clear official data obfuscates the true extent of the economic contraction, forcing markets to react to partial information. This historical context suggests that the current labor market jitters are more than just a momentary blip; they could be a harbinger of a more prolonged period of economic adjustment.

The Path Ahead: Navigating Uncertainty and Emerging Opportunities

Looking ahead, the market faces a period of heightened uncertainty, with both short-term and long-term possibilities heavily contingent on the resolution of the government shutdown and the subsequent release of comprehensive official labor market data. In the short term, investors will be keenly watching for any signs of an end to the shutdown, as this would pave the way for the delayed BLS reports. These official figures will either confirm the pessimistic outlook gleaned from alternative data or offer a more nuanced picture, thereby providing clearer direction for market sentiment and Federal Reserve expectations. Should the official data corroborate a significant slowdown, further market volatility and downward pressure on equities are likely, while bond yields could continue to decline as rate cut expectations firm.

In the long term, the trajectory of the labor market will dictate the pace of economic recovery. A prolonged period of high unemployment and weak job growth could lead to a sustained economic slowdown, potentially pushing the Federal Reserve to implement more aggressive monetary easing measures. This could create opportunities in sectors that benefit from lower interest rates, such as growth stocks, but also pose challenges for industries sensitive to overall economic health. Potential strategic pivots for businesses might include a renewed focus on efficiency, automation, and cost control, alongside a careful re-evaluation of expansion plans. Market opportunities could emerge in defensive sectors, dividend-paying stocks, and potentially in distressed assets if the downturn deepens. Conversely, challenges will persist for highly leveraged companies and those reliant on robust consumer spending.

Several potential scenarios and outcomes could unfold. One scenario involves a relatively quick resolution to the shutdown and official data revealing a less severe labor market contraction than feared, leading to a market rebound and a re-evaluation of the Fed's rate path. Another, more pessimistic scenario sees the official data confirming a deep slowdown, potentially triggering a broader market correction and increasing the likelihood of a recession, prompting significant monetary and fiscal stimulus. A third scenario involves a prolonged period of uncertainty due to continued political gridlock, leading to sustained market choppiness and a "wait-and-see" approach from both investors and businesses. The critical factor will be the interplay between economic data, political developments, and the Federal Reserve's response.

Conclusion: A Market at a Crossroads

The recent labor market reports, though fragmented and delayed by a federal government shutdown, unequivocally signal a significant turning point for the U.S. economy and financial markets. The key takeaway is a palpable shift towards a weakening job market, characterized by increasing layoffs and slowing hiring, which has instilled a deep sense of caution among investors. The immediate market reaction, marked by tumbling stock prices and fluctuating bond yields, underscores the profound impact of labor market health on overall economic sentiment and asset valuations.

Moving forward, the market is at a crossroads, with its trajectory heavily dependent on the resolution of political impasses and the subsequent release of comprehensive official economic data. Investors should brace for continued volatility and remain highly attuned to incoming economic indicators, particularly the official unemployment rate and non-farm payrolls once they become available. The Federal Reserve's response to these evolving conditions will be paramount, as any shift in its monetary policy stance—whether towards further tightening or easing—will send significant ripples through all asset classes.

The lasting impact of this period of uncertainty could be a recalibration of growth expectations and a heightened focus on corporate fundamentals and resilience. Investors should watch for signs of stabilization in the labor market, clarity on the Federal Reserve's path, and any governmental actions aimed at stimulating economic activity. Diversification, a focus on high-quality assets, and a long-term perspective will be crucial in navigating the challenges and opportunities that will undoubtedly emerge in the coming months as the market grapples with this evolving economic landscape.

This content is intended for informational purposes only and is not financial advice