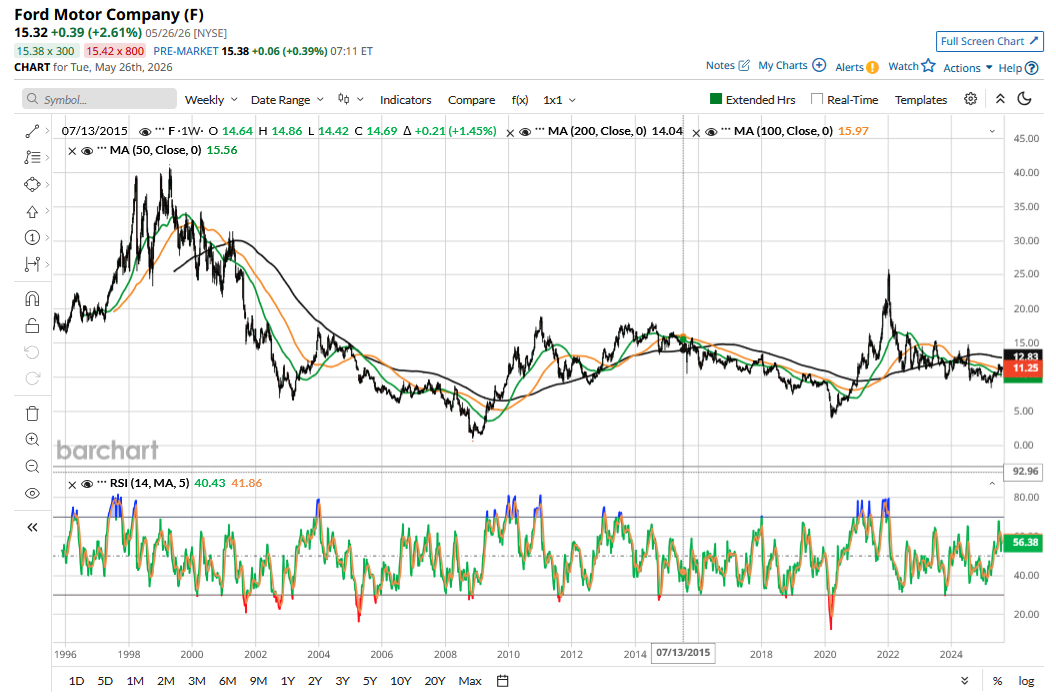

Ford (F) stock has traded in a tight price channel over the last five years. It has tended to bottom near $10, while witnessing selling pressure above $15. However, the stock has rallied over the last month and is now trading at the highest price level in nearly four years.

The rally is a welcome break for investors. The only succor has been the generous dividends, which the company has topped up with special dividends in the previous three years to meet its payout targets. However, even the fat dividends don’t make up for the massive underperformance versus the average S&P 500 Index ($SPX) constituent over the period.

Ford’s price action over the last month — in which it has added roughly a quarter to its market cap — is usually not something we associate with legacy automakers, but more like that of Tesla (TSLA). To be sure, the recent rally hasn’t been due to markets suddenly finding renewed love for its legacy automotive business, but rather due to its newly launched energy storage business, where it would compete with Tesla.

Notably, it's not only retail investors who are betting on Ford's energy pivot, and as fellow Barchart contributor Mark Hake argues, even institutions have been craving for a piece of the pie, considering the recent trades in long-term calls on Ford stock. In my previous article, I noted that there is scope for Ford stock to run higher on its energy push. With the stock now hitting a multi-year high, let's explore whether it is still a buy.

Ford’s Energy Storage Push Makes It an AI Play

Given the euphoria surrounding artificial intelligence (AI) its rare to find stocks seeing wild price moves (on either side) without a connection to the technology. There indeed is an ‘AI angle’ to Ford’s price action as it becomes an AI play with the nascent energy storage business.

The industry should see strong growth in the coming years, considering the power demand from data centers. Hyperscalers have been signing massive power purchase agreements to ensure their power-guzzling data centers have sufficient energy. Since data centers cannot afford any power disruption, they would also need energy storage systems to maintain 100% uptime and navigate grid constraints. As Ford noted in its blog, “The convergence of data center growth, renewable energy integration, and grid resilience requirements has created a gap in the market.”

Ford Plans Energy Storage System Deployments from 2027

Ford is planning its first customer deliveries from next year and is targeting an annual capacity of 20 GWh, which, for context, is less than half of what Tesla deployed last year. Tesla has an annual capacity of 80 GWh, split between the U.S. and Chinese plants, and is adding another 50 GWh capacity in Houston.

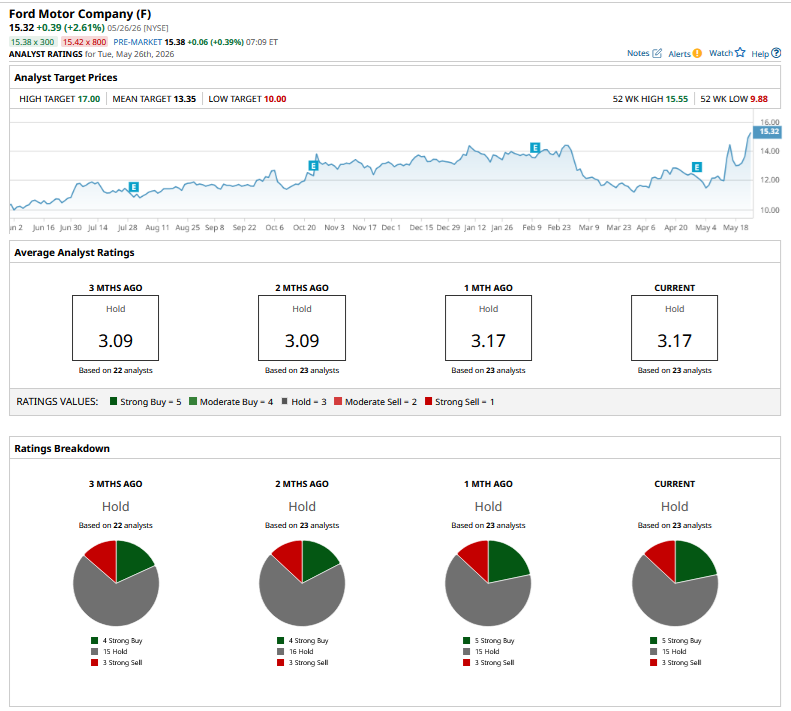

Morgan Stanley expects Ford's energy storage business to generate pre-tax profits of $588 million at 20 GWh annual production, at which point it predicts it would have a $10 billion enterprise value based on its assumption of a pre-tax earnings multiple of 17.5x. However, Ford has run ahead of the $14 target price that Morgan Stanley analyst Andrew Percoco has set for the automaker. Ford incidentally trades above its mean target price of $13.31, and while there is optimism over its energy storage business, Barclays believes the stock’s recent rally has been “overdone.”

Should You Buy Ford Stock?

Ford has been plagued by multiple issues. Its legacy internal combustion engine business has been doing reasonably well, but the company expects pricing to be flat this year. However, Ford expects higher commodity prices to be a headwind to the tune of $2 billion this year. Its electric vehicle (EV) business remains a drag on profitability with recurring losses. Moreover, higher warranty costs and frequent recalls have been a challenge for the Blue Oval.

That said, things should improve over the next year, and Ford expects $1 billion in savings from warranty cost improvement and materials this year. The gradual recovery at Novelis, which supplies aluminum to Ford, would also help buoy the company’s profits in the back half of the year.

Analysts expect Ford’s earnings per share (EPS) to rise by 47% in 2026 and 13% in 2027. Based on the expected 2027 EPS of $1.81, we get a 2027 price-to-earnings (P/E) multiple of 8.5x, which is higher than what the stock has traded at over the last couple of years.

The energy storage segment should add to Ford’s earnings once that business ramps up. However, for now, I believe it is tough to justify Ford’s rally as it seems to have moved from the realm of fundamentals to more of a speculative trade.

On the date of publication, Mohit Oberoi had a position in: F , TSLA . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Ford Stock Is Moving Like Tesla Now. Its Results Can’t Justify the Premium.

- 3 Dividend Kings to Buy Now to Replace the Social Security Income You're About to Lose

- This High-Yield Defense Stock Just Hiked Its Dividend Nearly 7%

- Bank of America Says Nvidia Is Still the Top AI Compute Stock to Buy Despite YTD Underperformance. Here’s Why.