Avis Budget Group (CAR) is a premier provider of global mobility solutions. The company operates three of the most recognized brands in the industry, such as Avis, Budget, and Zipcar, alongside regional brands like Payless and Maggiore. Avis Budget Group serves a diverse customer base ranging from premium business travelers to price-sensitive renters and urban car-sharers. The company is currently focused on a multi-year transformation, leveraging advanced fleet management technology and data analytics to optimize vehicle utilization and transition toward a more sustainable, electric-ready global fleet.

Founded in 1946, the company has expanded to over 10,000 locations worldwide with its headquarters in Parsippany, New Jersey.

Avis Budget Stock in a Frenzy

Avis Budget Group's stock has essentially "pulled a GameStop (GME)," surging almost 700% in April alone after bottoming near $135 in late March. This parabolic move has been driven by a massive short squeeze, with short interest exceeding 26% of the float. While technical "Golden Cross" signals and momentum trading have pushed the price to record highs, the stock remains disconnected from its fundamental valuation.

In comparison to the S&P 400 MidCap Index ($IDX), Avis Budget Group has delivered astronomical outperformance in the short term. While the S&P 400 has remained relatively stable, Avis's 517% year-to-date (YTD) gain has completely decoupled from its index peers. Historically, the stock has been more volatile than the index (beta of 1.94), but the current gap reflects a rare "meme-stock" event in which CAR's daily price action frequently triggers circuit-breaker halts, leaving the steady growth of the S&P 400 far behind.

Avis reported Mixed Results

Avis Budget Group reported its fourth-quarter 2025 results on Feb. 18, 2026, posting revenues of $2.7 billion, consistent with the previous year. However, the company reported a significant net loss of $856 million, primarily driven by a $518 million impairment charge related to the aggressive revaluation and shortening of the useful life of its U.S. electric vehicle (EV) fleet.

Despite this GAAP loss, Adjusted EBITDA for the quarter was $5 million, a notable improvement from the prior year’s loss. For the full year 2025, revenues reached $11.7 billion, fueled by sustained demand across both the Americas and International segments.

Entering 2026, management is focused on "tightening fleet discipline" and strengthening the balance sheet. CEO Brian Choi highlighted that the challenging Q4 served as a catalyst for meaningful change, including the monetization of $183 million in tax credits through EV sales to a joint venture. The company ended the year with $818 million in liquidity and an additional $2.1 billion in fleet funding capacity.

Looking ahead, Avis expects to drive sustainable earnings growth by optimizing fleet costs and enhancing the customer experience, aiming to transition from the "restructuring" phase of 2025 into a high-margin operational cycle as the used-car market stabilizes throughout the remainder of 2026.

Analyst Downgrades Avis

Avis Budget Group shares have surged dramatically, climbing another 19% in recent premarket trading to extend a four-day winning streak. This rally is driven by a massive short squeeze, with S3 Partners data indicating that short interest accounts for a staggering 62% of the company's free float. Investors betting against the stock have been forced to buy shares to cover their positions, fueling a vertical rise of over 500% in the last month alone.

Despite these gains, Barclays has downgraded the stock to "Underweight," citing an extreme supply-demand mismatch. Analyst Dan Levy noted that two major holders control roughly 71% of the company’s ownership, creating highly volatile trading conditions.

While the technical squeeze is currently the dominant force behind the price action, Levy acknowledged that the underlying car rental business is actually showing healthy signs, with improving price trends and lower vehicle depreciation.

Ultimately, investors should be cautious. While the technical rally is historic, the stock’s current price is disconnected from traditional valuation, driven more by concentrated ownership and intense trading volume than fundamental business performance.

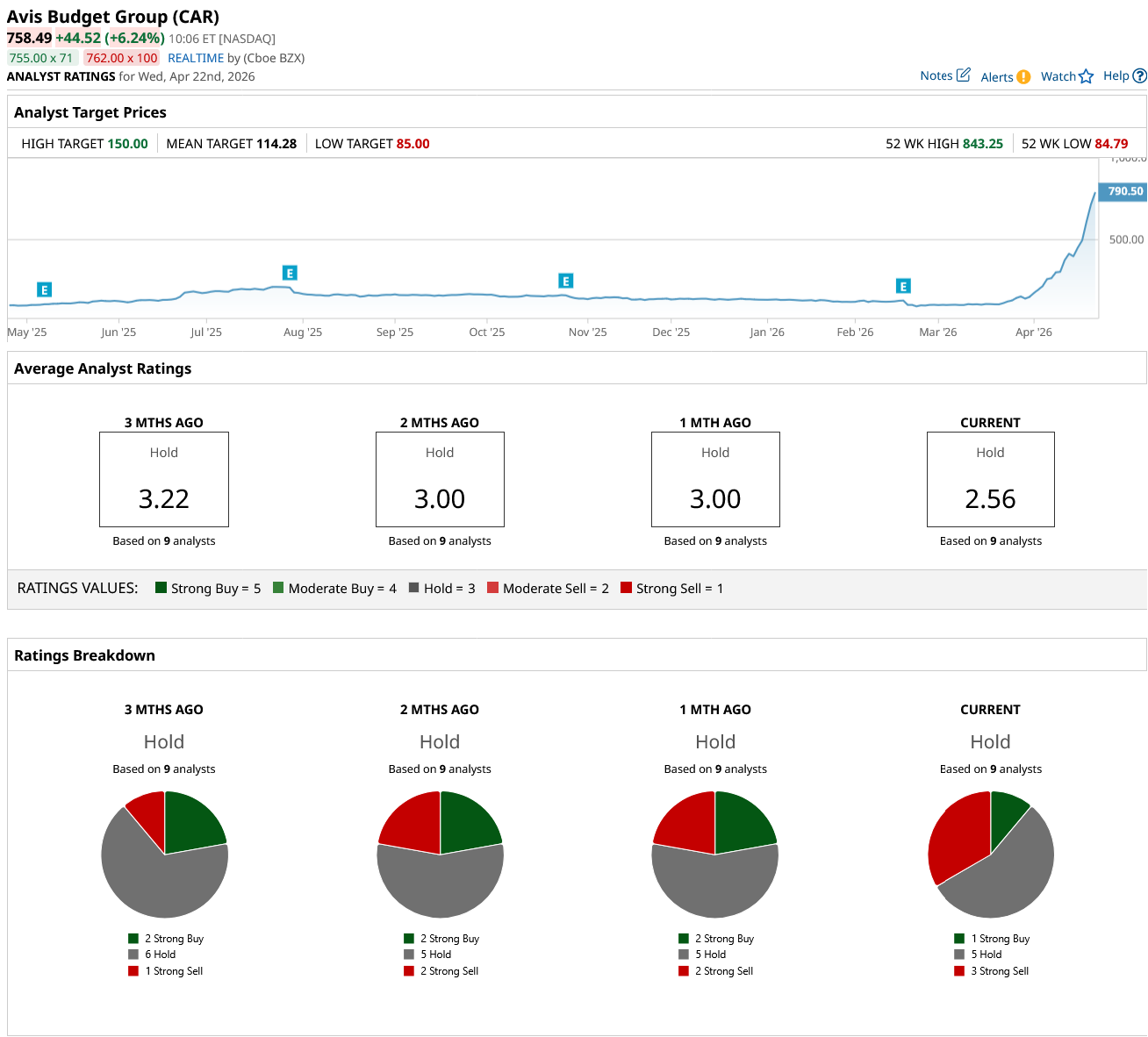

Should You Buy CAR Stock?

The current disconnect between CAR stock’s market price and professional sentiment is stark. Following the recent parabolic move, the stock carries a consensus "Hold" rating. Of the nine analysts covering the stock, one has a “Strong Buy” rating, three have issued a "Strong Sell" recommendation, and five have assigned a "Hold." The mean price target is $114.28, implying a staggering 85% downside from the current squeeze-inflated levels.

On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- This Delta Insider Just Slashed His Stake by More Than One-Fifth (21%). Is It Time to Follow Suit and Ditch DAL Stock?

- AMD Stock Just Hit New All-Time Highs. Should You Buy Shares Here?

- The ‘ChatGPT Moment’ for Cadence Design Systems Might Just Have Arrived, Says Needham. Should You Buy CDNS Stock Now?