Reed Hastings, co-founder and former chief executive of Netflix (NFLX), just sold more than 400,000 shares worth roughly $40 million, and that kind of insider move always gets people talking. He also executed another large sale on Dec. 1, 2025, unloading about 377,570 shares for roughly $40.7 million in a single transaction, which adds to the unease around his latest move.

His timing also stands out because the company remains one of the most closely watched names in streaming and media. The scrutiny has only grown after deal drama tied to Warner Bros. (WBD) pushed sentiment lower and raised fresh doubts about where the business goes next.

Even so, the market has not treated the story like a collapse, because the stock is still up 20.46% over the past month. Still, Netflix remains a global streaming heavyweight, so the real question is whether Hastings is simply taking profits or quietly signaling tougher days ahead. Let's dive in.

Netflix’s Numbers Behind Hastings’ Sale

Streaming giant Netflix, based in Los Gatos, California, operates a global subscription platform for films, series, and live content and commands roughly $419 billion in equity value.

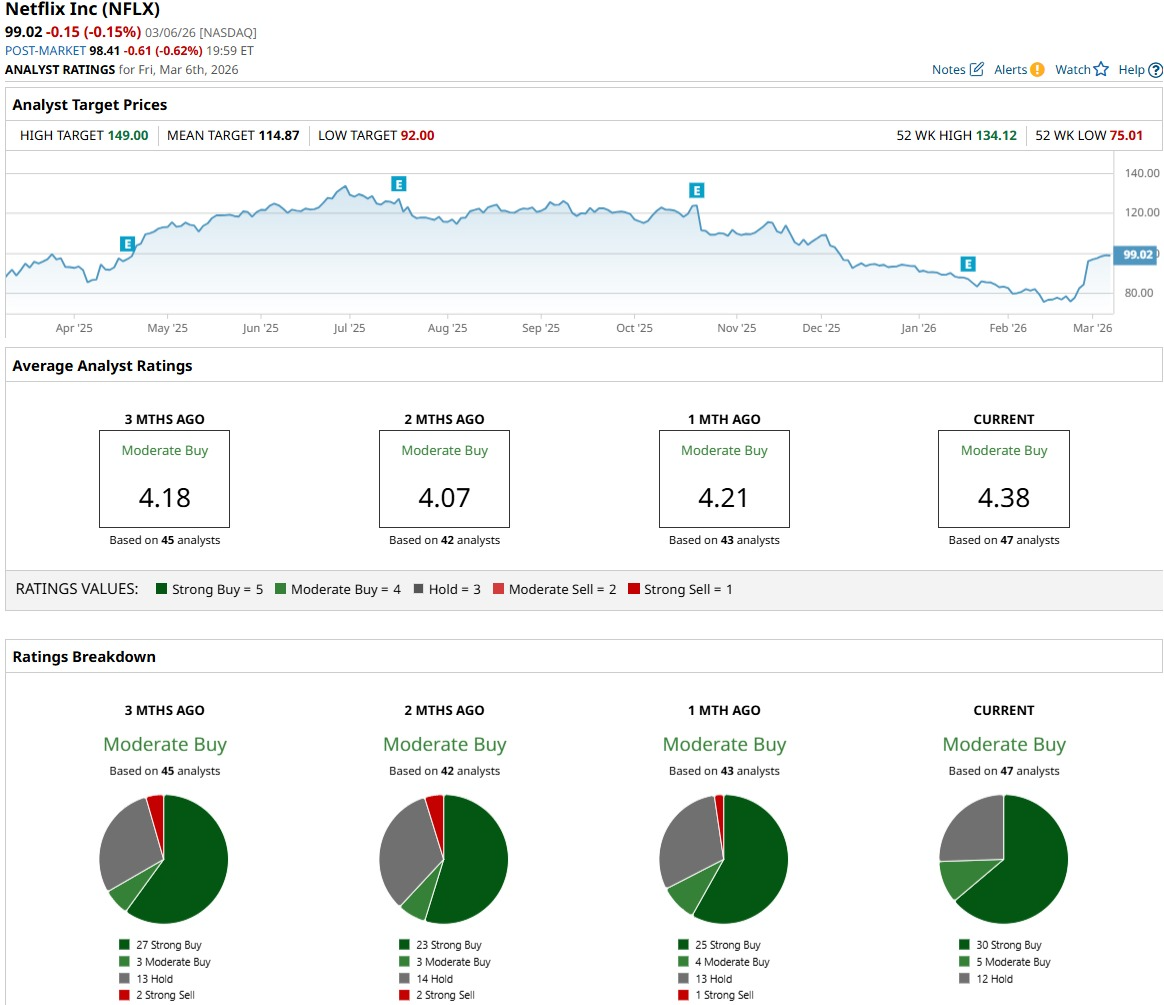

NFLX stock changes hands at $99.02 as of March 6, up 5.61% year‑to‑date (YTD) and 9.25% over the past 52 weeks.

That valuation now reflects a business investors are willing to pay up for, with a forward P/E of 31.40x versus a sector median of 13.82x and a PEG ratio of 1.40x against a sector median of 0.68x.

This earnings story most recently showed up on Jan. 20, 2026, when Netflix reported Q4 2025 GAAP EPS of $0.56, edging past the $0.55 consensus estimate for a 1.82% upside surprise. Their top line for that December 2025 quarter reached about $12.1 billion in sales, representing 4.70% year‑on‑year (YoY) growth. This confirms that the company can still expand revenue even as the streaming market matures and competition intensifies, with net income at roughly $2.4 billion, down 5.04% from the prior year.

The cash flow picture is stronger, with operating cash flow jumping to about $10.1 billion in December 2025, up 26.27% and showing better conversion of revenue into cash, but the net cash flow figure was less impressive. It came in at about $1.23 billion, down 16.96% from the prior period. That decline suggests cash movement was not uniformly strong across the board.

Growth Story Hastings Is Selling Into

Netflix now serves about 325 million paying subscribers worldwide, a milestone that cements its status as the default streaming choice for a huge slice of the global audience and gives it meaningful pricing power over time. This subscriber base feeds a flywheel of engagement, content investment, and recurring cash flow that long‑term holders continue to lean on when insiders decide to sell stock and diversify.

Another key development is the 10‑for‑1 stock split that was announced to take effect on Nov. 17. That move did not change the business, but it did make each share far cheaper on a per‑unit basis and therefore more accessible to smaller investors who were put off when the stock traded above $1,000. The split is also expected to improve liquidity and broaden ownership.

Analyst Expectations Keep the Bull Case Alive

Netflix’s next big checkpoint is circled on the calendar for April 16, 2026, when Netflix will report results for the current quarter ending March 2026. This upcoming print carries an average EPS estimate of $0.76, up from $0.66 in the same quarter a year ago, which works out to an estimated YoY growth rate of 15.15%.

There is also a useful read‑through on how other growth investors have treated the stock on weakness. Cathie Wood’s ARKW ETF (ARKW) bought 15,756 Netflix shares worth about $17.5 million after the stock dropped 10% following third‑quarter earnings. That purchase made Netflix the fund’s 40th largest holding, with a 0.77% allocation.

That positive stance shows up clearly in the broader ratings picture, as the consensus rating on NFLX stands at “Moderate Buy,” based on 47 analysts. Their average price target clocks in at $114.87, implying about 16% upside from here if those forecasts play out. It effectively says that, while some insiders are cashing in past gains, the analyst consensus still sees room for Netflix to deliver further value.

Conclusion

Reed Hastings cashing out $40 million is a headline, not a smoking gun. His sale looks more like ultra‑rich portfolio housekeeping than a verdict that Netflix is done. With earnings still growing, cash flow climbing, and analysts projecting upside from around $99 to roughly $115, the setup tilts more toward “hold or nibble on dips” than “rush for the exit.” NFLX stock is more likely to grind higher than collapse from here, though the ride probably will not be smooth.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- The Real Winner from Broadcom’s Q1 Earnings Is This 1 Lesser-Known Stock

- Drone Contract Wins Are Sending Red Cat Stock Higher. Should You Buy RCAT Here?

- This Software Stock Is Shrugging Off Apocalypse Fears. Should You Chase the Rally Here?

- Berkshire Hathaway Is Buying Back Stock. Why That’s a Key Signal for Investors to Watch Now.