What a fantastic six months it’s been for SM Energy. Shares of the company have skyrocketed 82.3%, hitting $33.72. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Following the strength, is SM a buy right now? Or is the market overestimating its value? Find out in our full research report, it’s free.

Why Are We Positive On SM Energy?

Operating across three key regions with over 328,000 net acres under its control, SM Energy (NYSE: SM) explores for, develops, and produces oil, natural gas, and natural gas liquids primarily from shale formations in Texas and Utah.

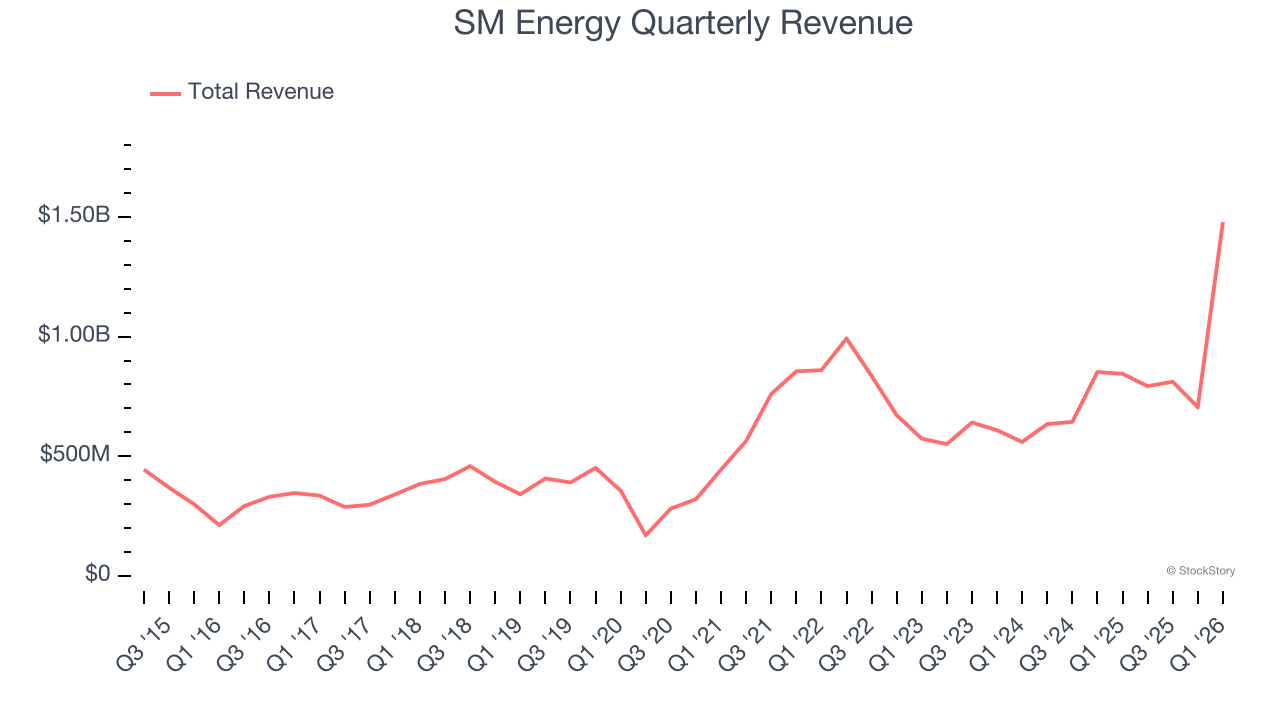

1. Skyrocketing Revenue Shows Strong Momentum

Cyclical industries such as Energy can make mediocre companies look great for a time, but a long-term view reveals which businesses can actually withstand and adapt to changing conditions. Luckily, SM Energy’s sales grew at an incredible 25.5% compounded annual growth rate over the last five years. Its growth surpassed the average energy upstream and integrated energy company and shows its offerings resonate with customers.

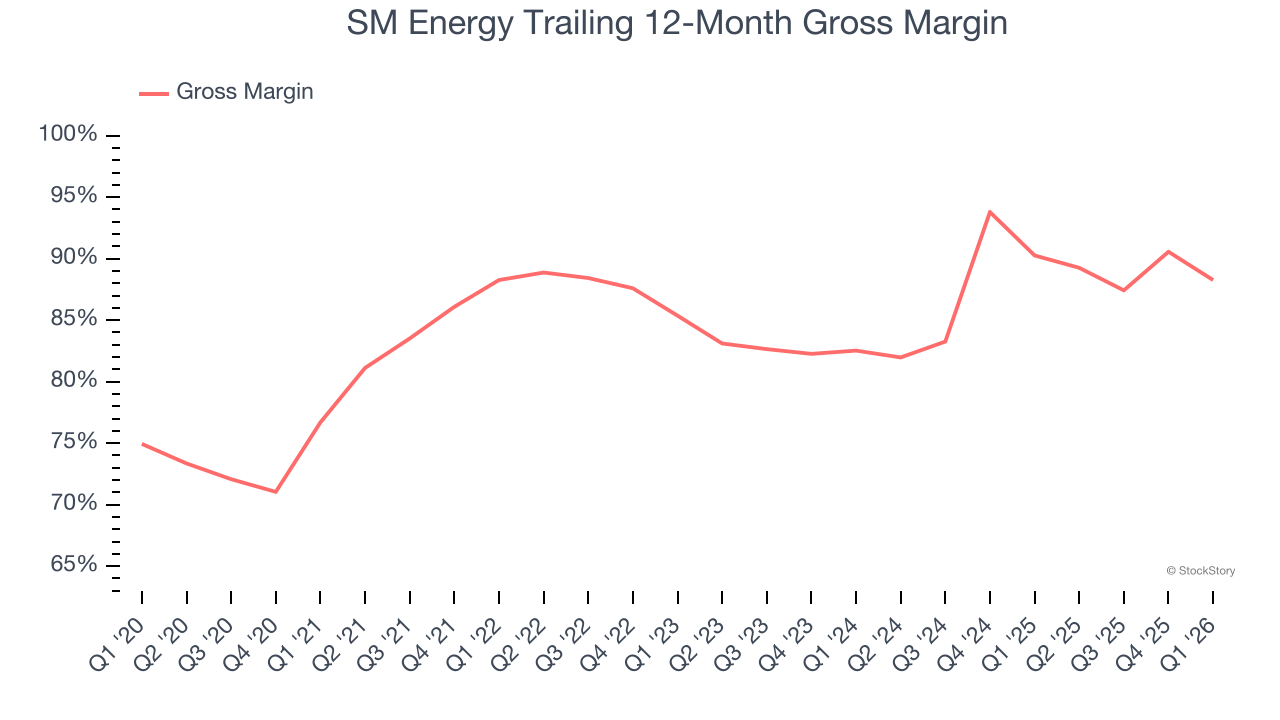

2. Elite Gross Margin Powers Best-In-Class Business Model

In any given year, energy gross margins are heavily influenced by prices, hedging, and cost inflation, but over a full cycle these gross margins reveal which producers are structurally advantaged through superior “rock” quality, infrastructure access, and cost position.

SM Energy, which averaged 87.2% gross margin over the last five years, exhibits enviable unit economics in the sector. It means the company will remain profitable at lower commodity prices than peers with inferior gross margins and serves as an advantaged starting point for ultimate operating profits and free cash flow generation.

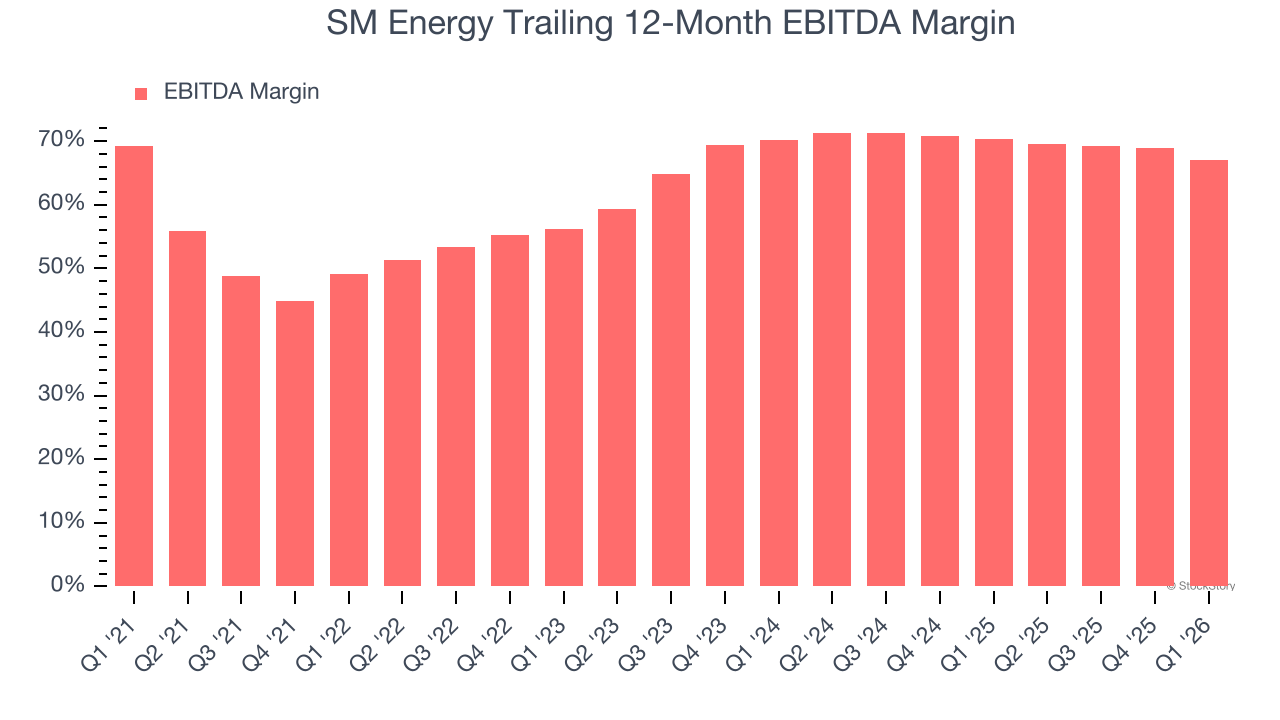

3. EBITDA Margin Rising, Profits Up

Adjusted EBITDA margin strips out accounting distortions tied to depletion and historical drilling spend, providing a clearer view of the cash-generating power of the underlying asset base before financing and reinvestment decisions.

Looking at the trend in its profitability, SM Energy’s EBITDA margin rose by 18 percentage points over the last year, as its sales growth gave it immense operating leverage. Its EBITDA margin for the trailing 12 months was 67%.

Final Judgment

These are just a few reasons why SM Energy ranks near the top of our list, and after the recent surge, the stock trades at 4.3× forward P/E (or $33.72 per share). Is now the right time to buy? See for yourself in our comprehensive research report, it’s free.

High-Quality Stocks for All Market Conditions

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum - both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks - FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.