Carter's has gotten torched over the last six months - since November 2024, its stock price has dropped 34.9% to $32.77 per share. This may have investors wondering how to approach the situation.

Is now the time to buy Carter's, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think Carter's Will Underperform?

Even though the stock has become cheaper, we don't have much confidence in Carter's. Here are three reasons why we avoid CRI and a stock we'd rather own.

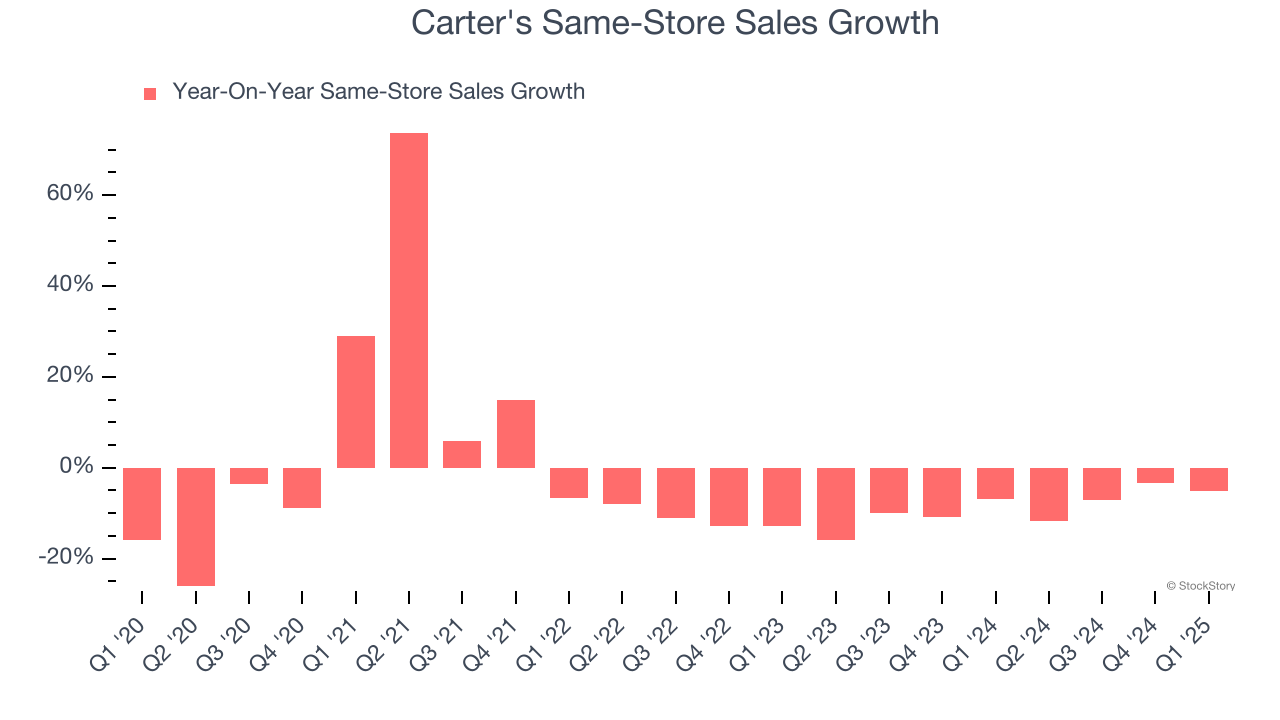

1. Shrinking Same-Store Sales Indicate Waning Demand

In addition to reported revenue, same-store sales are a useful data point for analyzing Apparel and Accessories companies. This metric measures the change in sales at brick-and-mortar locations that have existed for at least a year, giving visibility into Carter’s underlying demand characteristics.

Over the last two years, Carter’s same-store sales averaged 8.9% year-on-year declines. This performance was underwhelming and implies there may be increasing competition or market saturation. It also suggests Carter's might have to close some locations or change its strategy and pricing, which can disrupt operations.

2. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Carter’s revenue to drop by 2.1%. While this projection is better than its two-year trend, it's tough to feel optimistic about a company facing demand difficulties.

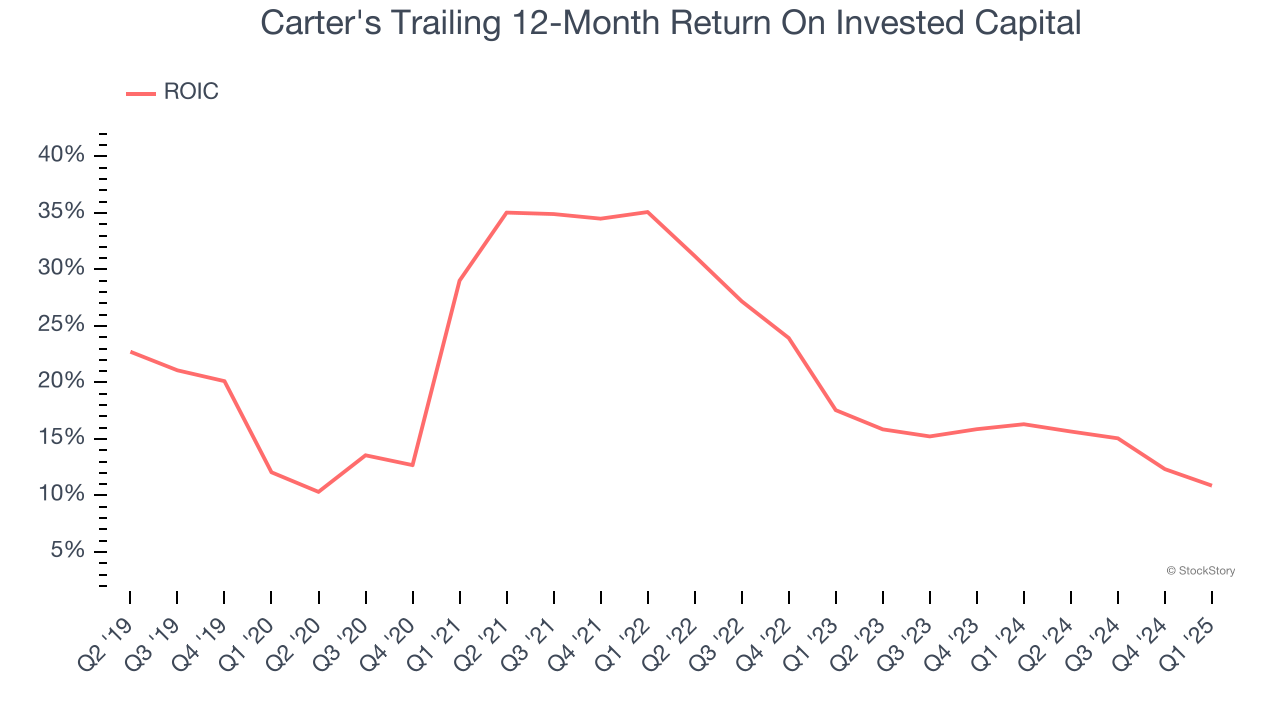

3. New Investments Fail to Bear Fruit as ROIC Declines

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Carter’s ROIC has unfortunately decreased significantly. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

Final Judgment

Carter's doesn’t pass our quality test. Following the recent decline, the stock trades at 9.2× forward P/E (or $32.77 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are superior stocks to buy right now. We’d recommend looking at an all-weather company that owns household favorite Taco Bell.

Stocks That Overcame Trump’s 2018 Tariffs

Market indices reached historic highs following Donald Trump’s presidential victory in November 2024, but the outlook for 2025 is clouded by new trade policies that could impact business confidence and growth.

While this has caused many investors to adopt a "fearful" wait-and-see approach, we’re leaning into our best ideas that can grow regardless of the political or macroeconomic climate. Take advantage of Mr. Market by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today.