BJ's currently trades at $117.98 and has been a dream stock for shareholders. It’s returned 351% since May 2020, blowing past the S&P 500’s 96.1% gain. The company has also beaten the index over the past six months as its stock price is up 37.8%.

Is there a buying opportunity in BJ's, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is BJ's Not Exciting?

We’re happy investors have made money, but we're cautious about BJ's. Here are three reasons why there are better opportunities than BJ and a stock we'd rather own.

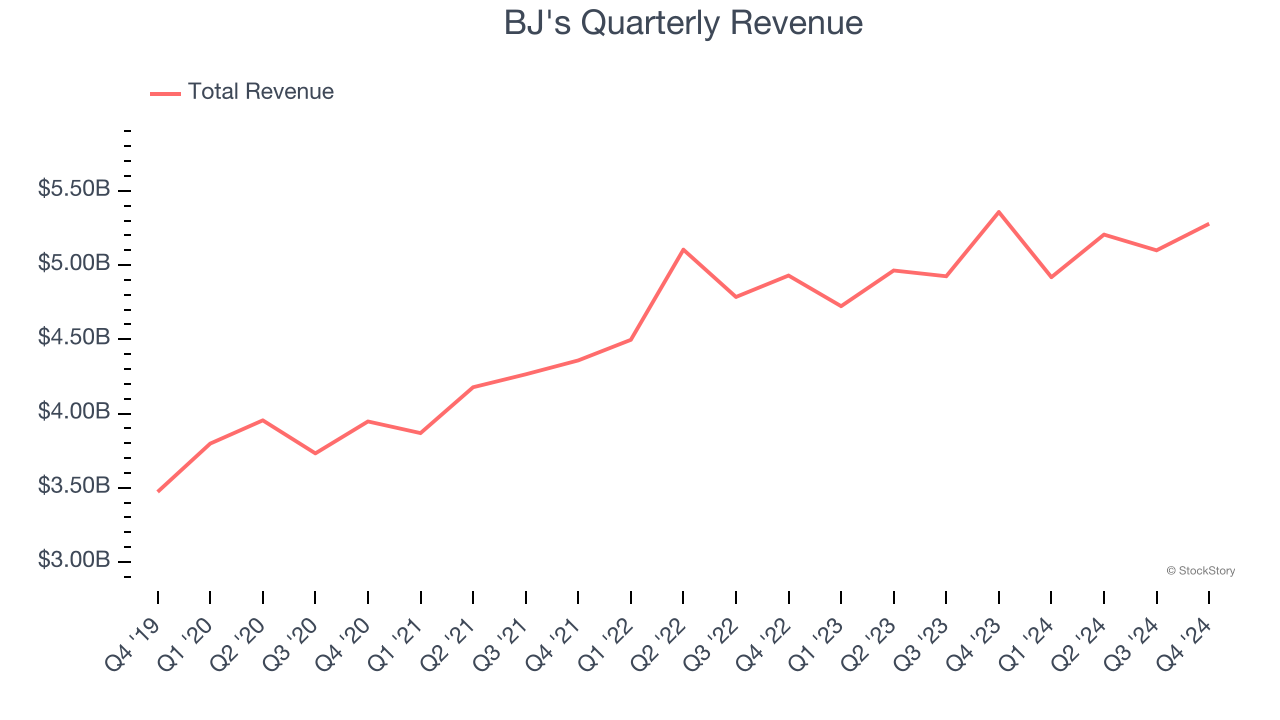

1. Long-Term Revenue Growth Disappoints

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, BJ’s sales grew at a mediocre 9.2% compounded annual growth rate over the last five years. This fell short of our benchmark for the consumer retail sector.

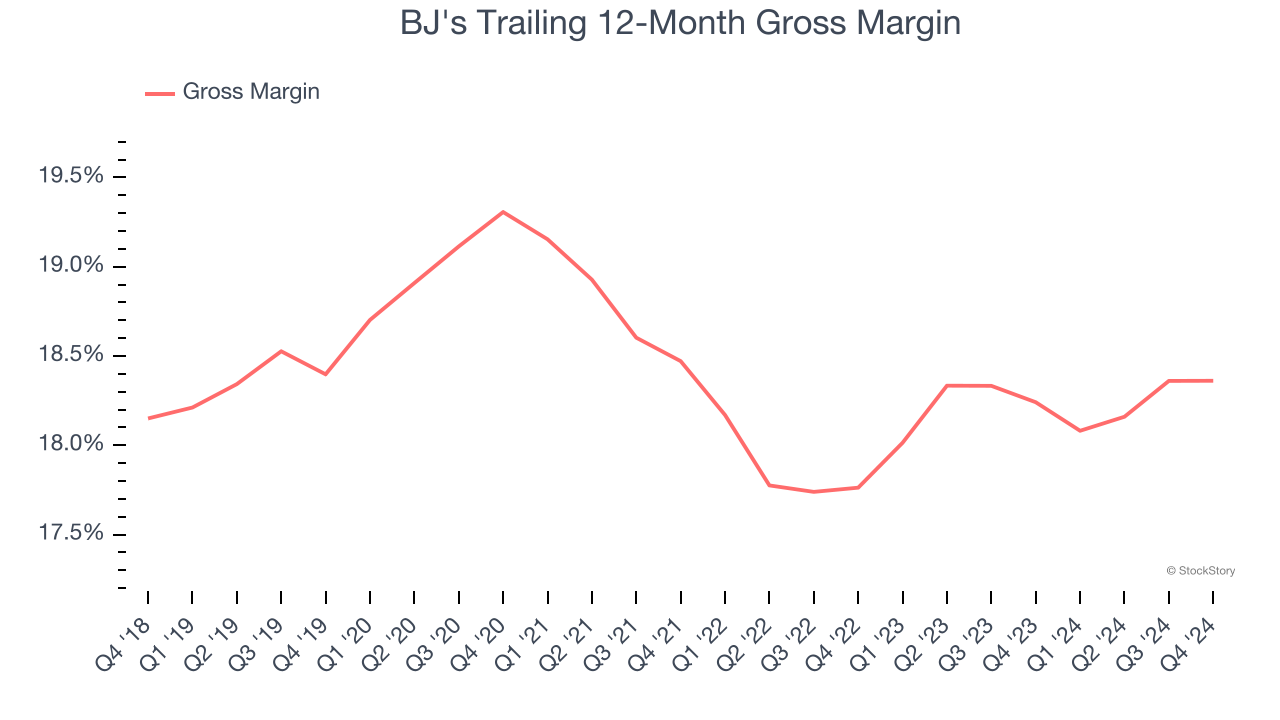

2. Low Gross Margin Reveals Weak Structural Profitability

Gross profit margins are an important measure of a retailer’s pricing power, product differentiation, and negotiating leverage.

BJ's has bad unit economics for a retailer, signaling it operates in a competitive market and lacks pricing power because its inventory is sold in many places. As you can see below, it averaged a 18.3% gross margin over the last two years. That means BJ's paid its suppliers a lot of money ($81.70 for every $100 in revenue) to run its business.

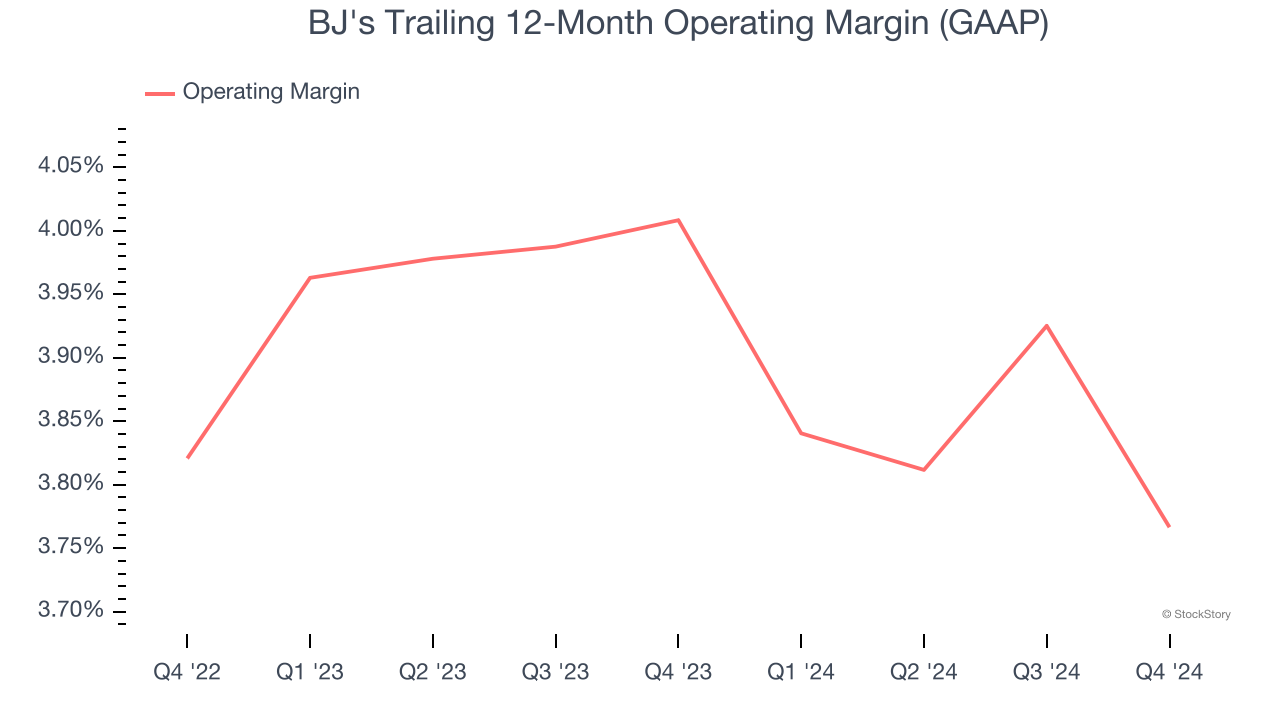

3. Weak Operating Margin Could Cause Trouble

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

BJ's was profitable over the last two years but held back by its large cost base. Its average operating margin of 3.9% was weak for a consumer retail business. This result isn’t too surprising given its low gross margin as a starting point.

Final Judgment

BJ’s business quality ultimately falls short of our standards. With its shares topping the market in recent months, the stock trades at 27.6× forward price-to-earnings (or $117.98 per share). This valuation tells us a lot of optimism is priced in - you can find better investment opportunities elsewhere. Let us point you toward an all-weather company that owns household favorite Taco Bell.

Stocks We Would Buy Instead of BJ's

Market indices reached historic highs following Donald Trump’s presidential victory in November 2024, but the outlook for 2025 is clouded by new trade policies that could impact business confidence and growth.

While this has caused many investors to adopt a "fearful" wait-and-see approach, we’re leaning into our best ideas that can grow regardless of the political or macroeconomic climate. Take advantage of Mr. Market by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.