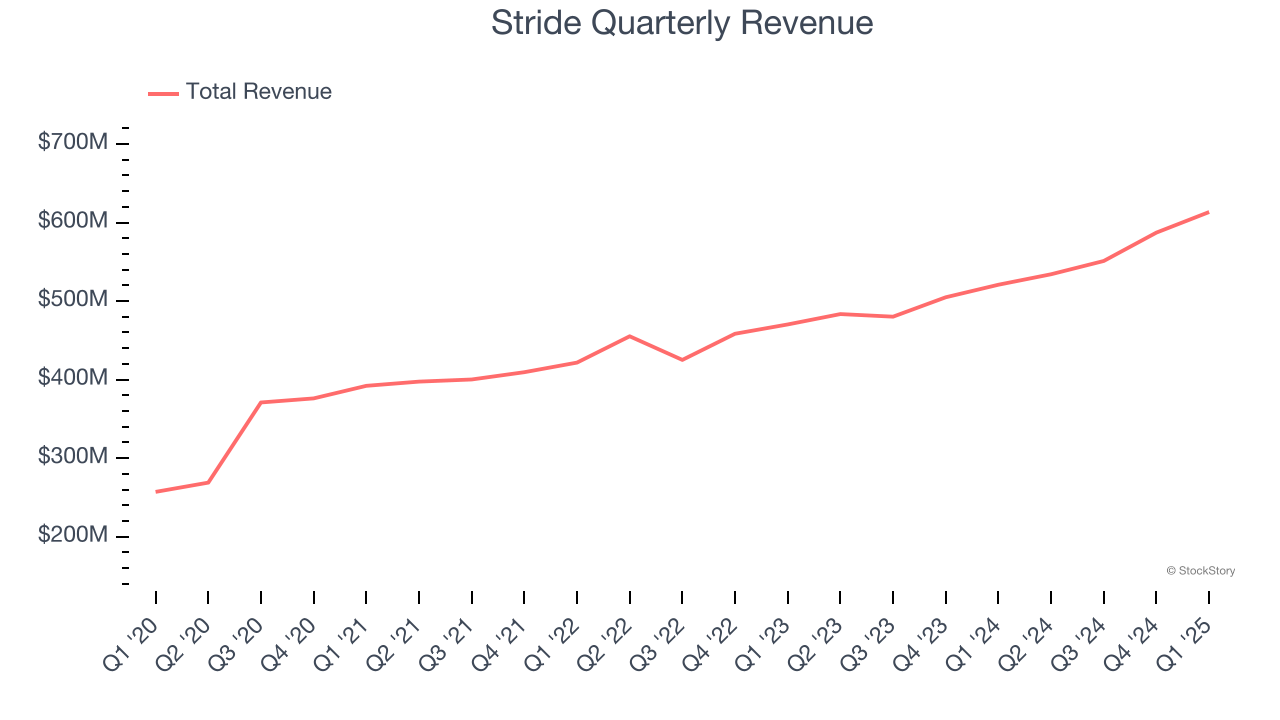

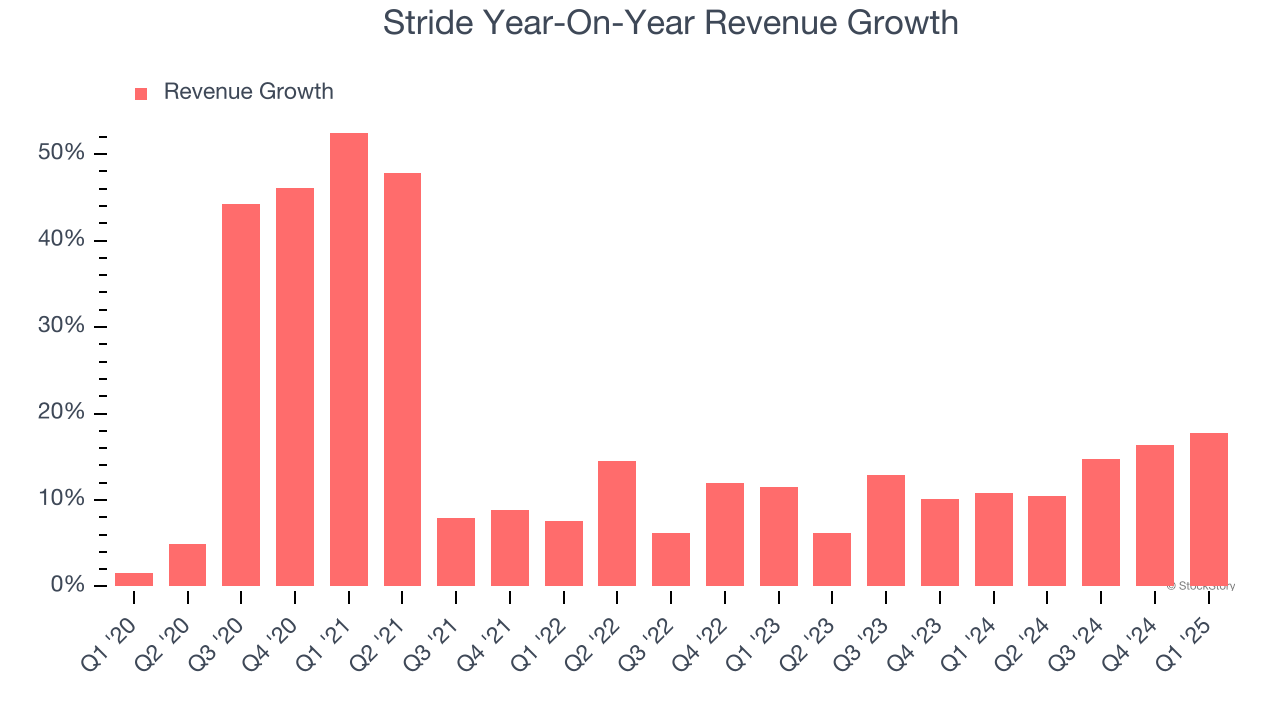

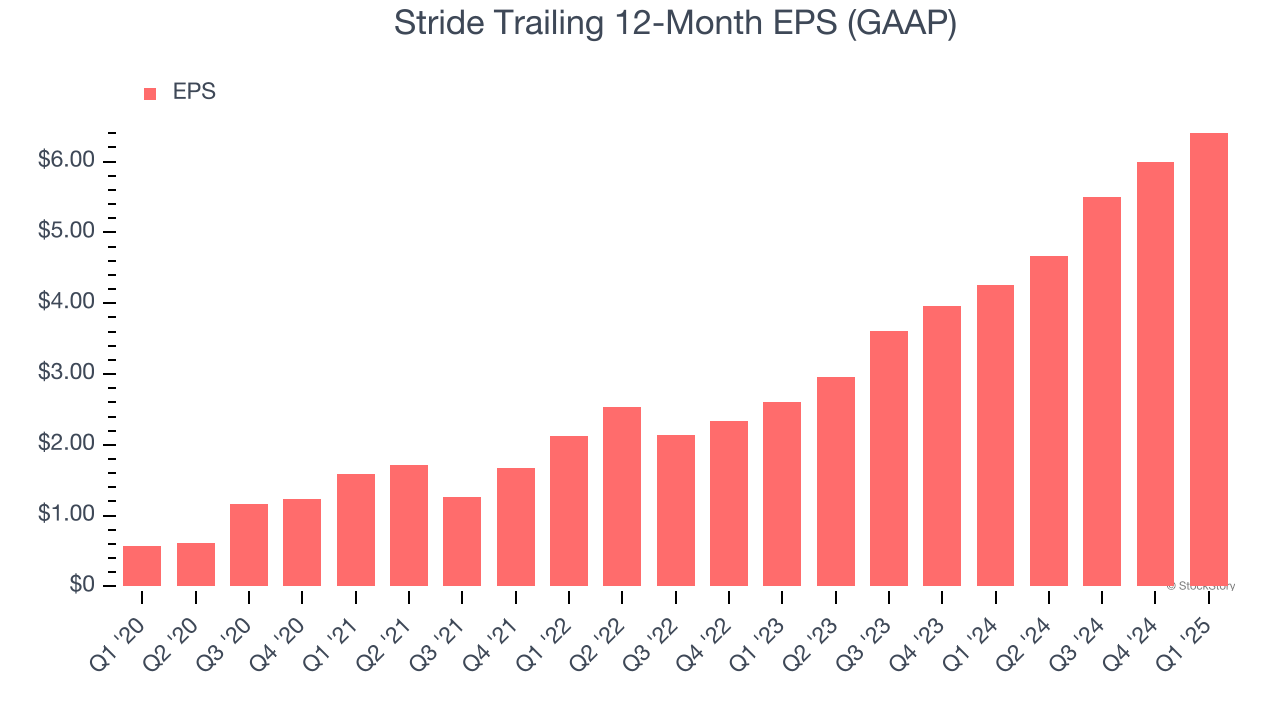

Online education Stride (NYSE: LRN) reported Q1 CY2025 results topping the market’s revenue expectations, with sales up 17.8% year on year to $613.4 million. The company’s full-year revenue guidance of $2.38 billion at the midpoint came in 1.6% above analysts’ estimates. Its GAAP profit of $2.02 per share was 0.7% above analysts’ consensus estimates.

Is now the time to buy Stride? Find out by accessing our full research report, it’s free.

Stride (LRN) Q1 CY2025 Highlights:

- Revenue: $613.4 million vs analyst estimates of $592.2 million (17.8% year-on-year growth, 3.6% beat)

- EPS (GAAP): $2.02 vs analyst estimates of $2.01 (0.7% beat)

- Adjusted EBITDA: $168.3 million vs analyst estimates of $159.7 million (27.4% margin, 5.4% beat)

- Operating Margin: 21.3%, up from 17% in the same quarter last year

- Market Capitalization: $6.02 billion

Company Overview

Formerly known as K12, Stride (NYSE: LRN) is an education technology company providing education solutions through digital platforms.

Sales Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $2.29 billion in revenue over the past 12 months, Stride is a mid-sized business services company, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale. On the bright side, it can still flex high growth rates because it’s working from a smaller revenue base.

As you can see below, Stride’s 17.3% annualized revenue growth over the last five years was incredible. This is a great starting point for our analysis because it shows Stride’s demand was higher than many business services companies.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. Stride’s annualized revenue growth of 12.4% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Stride reported year-on-year revenue growth of 17.8%, and its $613.4 million of revenue exceeded Wall Street’s estimates by 3.6%.

Looking ahead, sell-side analysts expect revenue to grow 7% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is healthy and suggests the market is baking in success for its products and services.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Stride has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 10.9%, higher than the broader business services sector.

Analyzing the trend in its profitability, Stride’s operating margin rose by 9.7 percentage points over the last five years, as its sales growth gave it immense operating leverage.

This quarter, Stride generated an operating profit margin of 21.3%, up 4.4 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Stride’s EPS grew at an astounding 62.3% compounded annual growth rate over the last five years, higher than its 17.3% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

We can take a deeper look into Stride’s earnings quality to better understand the drivers of its performance. As we mentioned earlier, Stride’s operating margin expanded by 9.7 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q1, Stride reported EPS at $2.02, up from $1.60 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects Stride’s full-year EPS of $6.41 to grow 7.9%.

Key Takeaways from Stride’s Q1 Results

We enjoyed seeing Stride beat analysts’ revenue, EPS, and EBITDA expectations this quarter. We were also glad its full-year revenue guidance exceeded Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 5.3% to $149.98 immediately following the results.

Stride had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.