What a brutal six months it’s been for Regal Rexnord. The stock has dropped 38.4% and now trades at $103.43, rattling many shareholders. This was partly driven by its softer quarterly results and may have investors wondering how to approach the situation.

Is there a buying opportunity in Regal Rexnord, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Even with the cheaper entry price, we don't have much confidence in Regal Rexnord. Here are three reasons why RRX doesn't excite us and a stock we'd rather own.

Why Is Regal Rexnord Not Exciting?

Headquartered in Milwaukee, Regal Rexnord (NYSE: RRX) provides power transmission and industrial automation products.

1. Core Business Falling Behind as Demand Declines

In addition to reported revenue, organic revenue is a useful data point for analyzing Engineered Components and Systems companies. This metric gives visibility into Regal Rexnord’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Regal Rexnord’s organic revenue averaged 6.6% year-on-year declines. This performance was underwhelming and implies it may need to improve its products, pricing, or go-to-market strategy. It also suggests Regal Rexnord might have to lean into acquisitions to grow, which isn’t ideal because M&A can be expensive and risky (integrations often disrupt focus).

2. EPS Took a Dip Over the Last Two Years

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

Sadly for Regal Rexnord, its EPS declined by 7.9% annually over the last two years while its revenue grew by 7.5%. This tells us the company became less profitable on a per-share basis as it expanded.

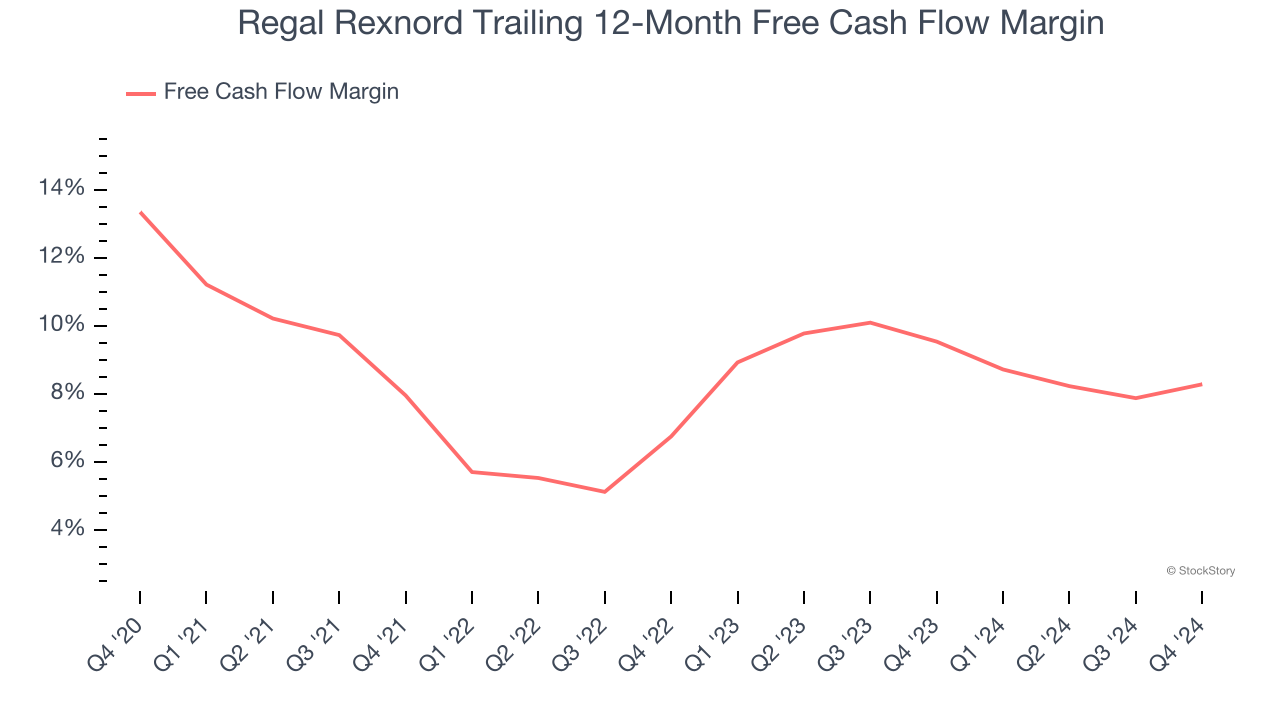

3. Free Cash Flow Margin Dropping

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Regal Rexnord’s margin dropped by 5.1 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. Regal Rexnord’s free cash flow margin for the trailing 12 months was 8.3%.

Final Judgment

Regal Rexnord isn’t a terrible business, but it doesn’t pass our quality test. Following the recent decline, the stock trades at 9.8× forward price-to-earnings (or $103.43 per share). While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're pretty confident there are superior stocks to buy right now. Let us point you toward one of our all-time favorite software stocks.

Stocks We Would Buy Instead of Regal Rexnord

The market surged in 2024 and reached record highs after Donald Trump’s presidential victory in November, but questions about new economic policies are adding much uncertainty for 2025.

While the crowd speculates what might happen next, we’re homing in on the companies that can succeed regardless of the political or macroeconomic environment. Put yourself in the driver’s seat and build a durable portfolio by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.