Wrapping up Q3 earnings, we look at the numbers and key takeaways for the generic pharmaceuticals stocks, including Viatris (NASDAQ: VTRS) and its peers.

The generic pharmaceutical industry operates on a volume-driven, low-cost business model, producing bioequivalent versions of branded drugs once their patents expire. These companies benefit from consistent demand for affordable medications, as they are critical to reducing healthcare costs. Generics typically face lower R&D expenses and shorter regulatory approval timelines compared to branded drug makers, enabling cost efficiencies. However, the industry is highly competitive, with intense pricing pressures, thin margins, and frequent legal challenges from branded pharmaceutical companies over patent disputes. Looking ahead, the industry is supported by tailwinds such as the role of AI in streamlining drug development (reverse engineering complex formulations) and manufacturing efficiency (optimize processes and remove inefficiencies). Governments and insurers' focus on reducing drug costs can also boost generics' adoption. However, headwinds include escalating pricing pressure from large buyers like pharmacy chains and healthcare distributors as well as evolving regulatory hurdles.

The 4 generic pharmaceuticals stocks we track reported a very strong Q3. As a group, revenues beat analysts’ consensus estimates by 4.2%.

Thankfully, share prices of the companies have been resilient as they are up 6.7% on average since the latest earnings results.

Weakest Q3: Viatris (NASDAQ: VTRS)

Created through the 2020 merger of Mylan and Pfizer's Upjohn division, Viatris (NASDAQ: VTRS) is a healthcare company that develops, manufactures, and distributes branded and generic medicines across more than 165 countries worldwide.

Viatris reported revenues of $3.76 billion, flat year on year. This print exceeded analysts’ expectations by 4.3%. Overall, it was a strong quarter for the company with an impressive beat of analysts’ revenue estimates and full-year revenue guidance slightly topping analysts’ expectations.

Interestingly, the stock is up 1.7% since reporting and currently trades at $10.98.

Is now the time to buy Viatris? Access our full analysis of the earnings results here, it’s free for active Edge members.

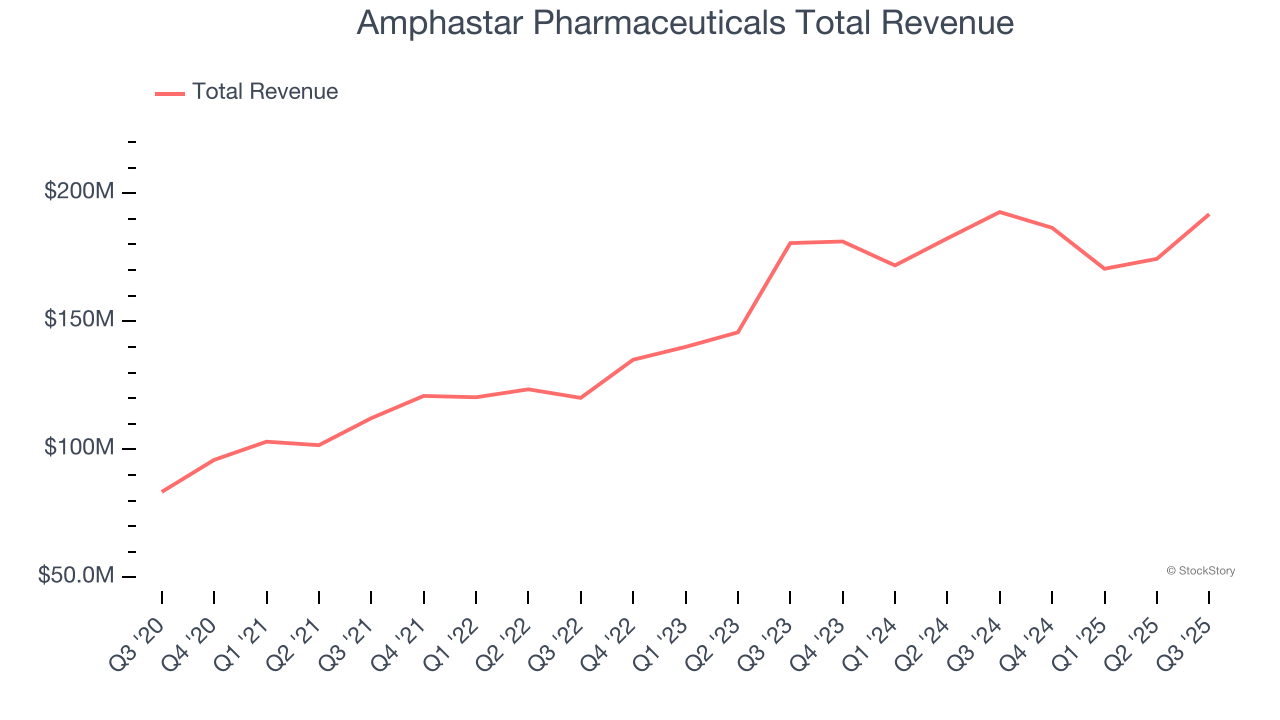

Best Q3: Amphastar Pharmaceuticals (NASDAQ: AMPH)

Founded in 1996 and known for its expertise in complex drug formulations, Amphastar Pharmaceuticals (NASDAQ: AMPH) develops and manufactures technically challenging injectable and inhalation medications, including both generic and proprietary pharmaceutical products.

Amphastar Pharmaceuticals reported revenues of $191.8 million, flat year on year, outperforming analysts’ expectations by 4%. The business had an exceptional quarter with a solid beat of analysts’ revenue estimates and a beat of analysts’ EPS estimates.

The market seems happy with the results as the stock is up 14.1% since reporting. It currently trades at $27.63.

Is now the time to buy Amphastar Pharmaceuticals? Access our full analysis of the earnings results here, it’s free for active Edge members.

Amneal (NASDAQ: AMRX)

Founded in 2002 and growing into one of America's largest generic drug producers, Amneal Pharmaceuticals (NASDAQ: AMRX) develops, manufactures, and distributes generic medicines, specialty branded drugs, biosimilars, and injectable products for the U.S. healthcare market.

Amneal reported revenues of $784.5 million, up 11.7% year on year, exceeding analysts’ expectations by 2.1%. It may have had the worst quarter among its peers, but its results were still good as it also locked in a beat of analysts’ EPS estimates and full-year revenue guidance slightly topping analysts’ expectations.

Amneal delivered the highest full-year guidance raise but had the weakest performance against analyst estimates in the group. Interestingly, the stock is up 14.1% since the results and currently trades at $11.91.

Read our full analysis of Amneal’s results here.

ANI Pharmaceuticals (NASDAQ: ANIP)

With a diverse portfolio of 116 pharmaceutical products and a growing rare disease platform, ANI Pharmaceuticals (NASDAQ: ANIP) develops, manufactures, and markets branded and generic prescription pharmaceuticals, with a focus on rare disease treatments.

ANI Pharmaceuticals reported revenues of $227.8 million, up 53.6% year on year. This number surpassed analysts’ expectations by 6.4%. Overall, it was a very strong quarter as it also put up a solid beat of analysts’ revenue estimates and a beat of analysts’ EPS estimates.

ANI Pharmaceuticals delivered the biggest analyst estimates beat and fastest revenue growth, but had the weakest full-year guidance update among its peers. The stock is down 2.9% since reporting and currently trades at $87.68.

Read our full, actionable report on ANI Pharmaceuticals here, it’s free for active Edge members.

Market Update

As a result of the Fed’s rate hikes in 2022 and 2023, inflation has come down from frothy levels post-pandemic. The general rise in the price of goods and services is trending towards the Fed’s 2% goal as of late, which is good news. The higher rates that fought inflation also didn't slow economic activity enough to catalyze a recession. So far, soft landing. This, combined with recent rate cuts (half a percent in September 2024 and a quarter percent in November 2024) have led to strong stock market performance in 2024. The icing on the cake for 2024 returns was Donald Trump’s victory in the U.S. Presidential Election in early November, sending major indices to all-time highs in the week following the election. Still, debates around the health of the economy and the impact of potential tariffs and corporate tax cuts remain, leaving much uncertainty around 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.