Heartland Express has followed the market’s trajectory closely, rising in tandem with the S&P 500 over the past six months. The stock has climbed by 10.3% to $12.56 per share while the index has gained 13%.

Is now the time to buy Heartland Express, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.We're sitting this one out for now. Here are three reasons why you should be careful with HTLD and a stock we'd rather own.

Why Is Heartland Express Not Exciting?

Founded by the son of a trucker, Heartland Express (NASDAQ: HTLD) offers full-truckload deliveries across the United States and Mexico.

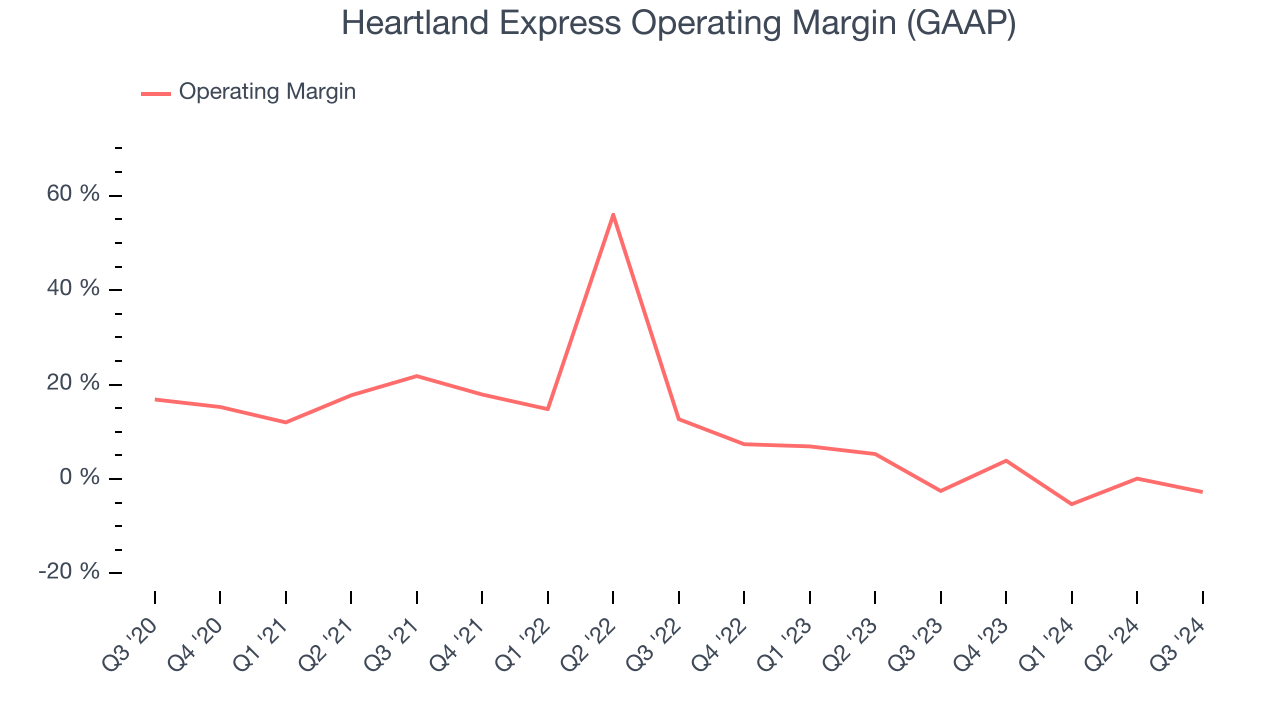

1. Operating Margin Falling

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Looking at the trend in its profitability, Heartland Express’s operating margin decreased by 14.3 percentage points over the last five years. Even though its historical margin is high, shareholders will want to see Heartland Express become more profitable in the future. Its operating margin for the trailing 12 months was breakeven.

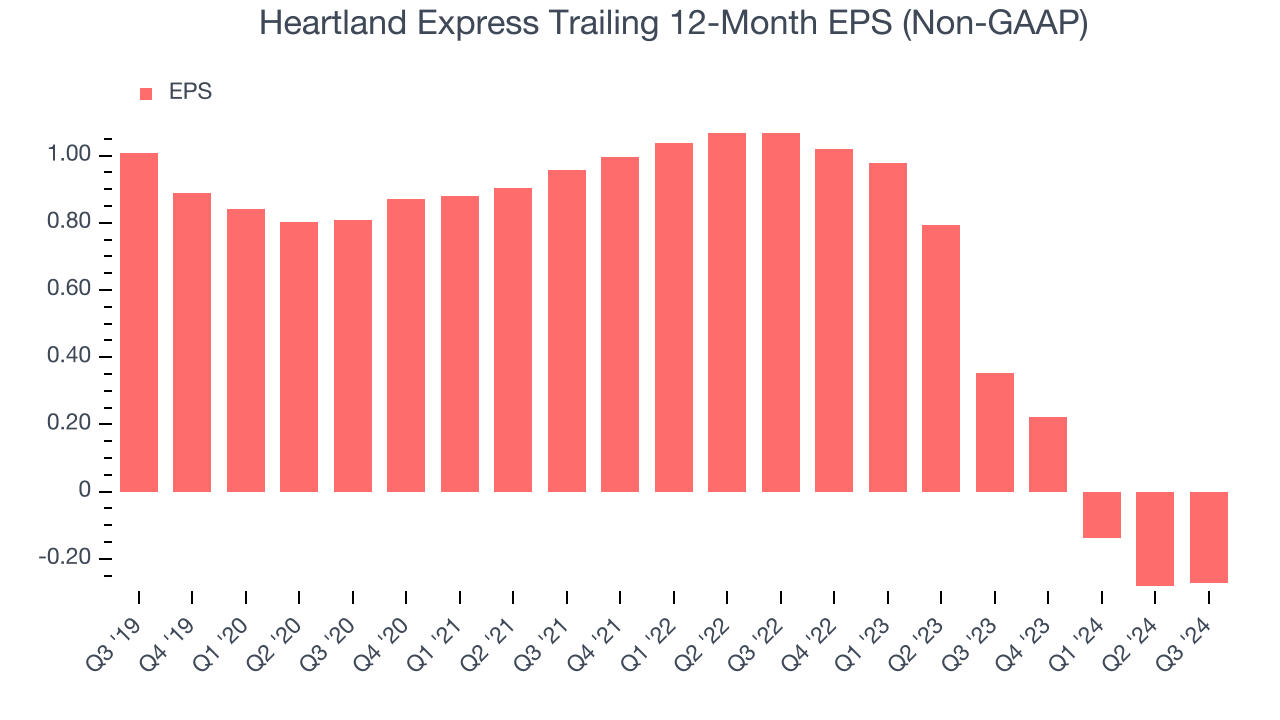

2. EPS Trending Down

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Heartland Express, its EPS declined by 17.8% annually over the last five years while its revenue grew by 13.4%. This tells us the company became less profitable on a per-share basis as it expanded.

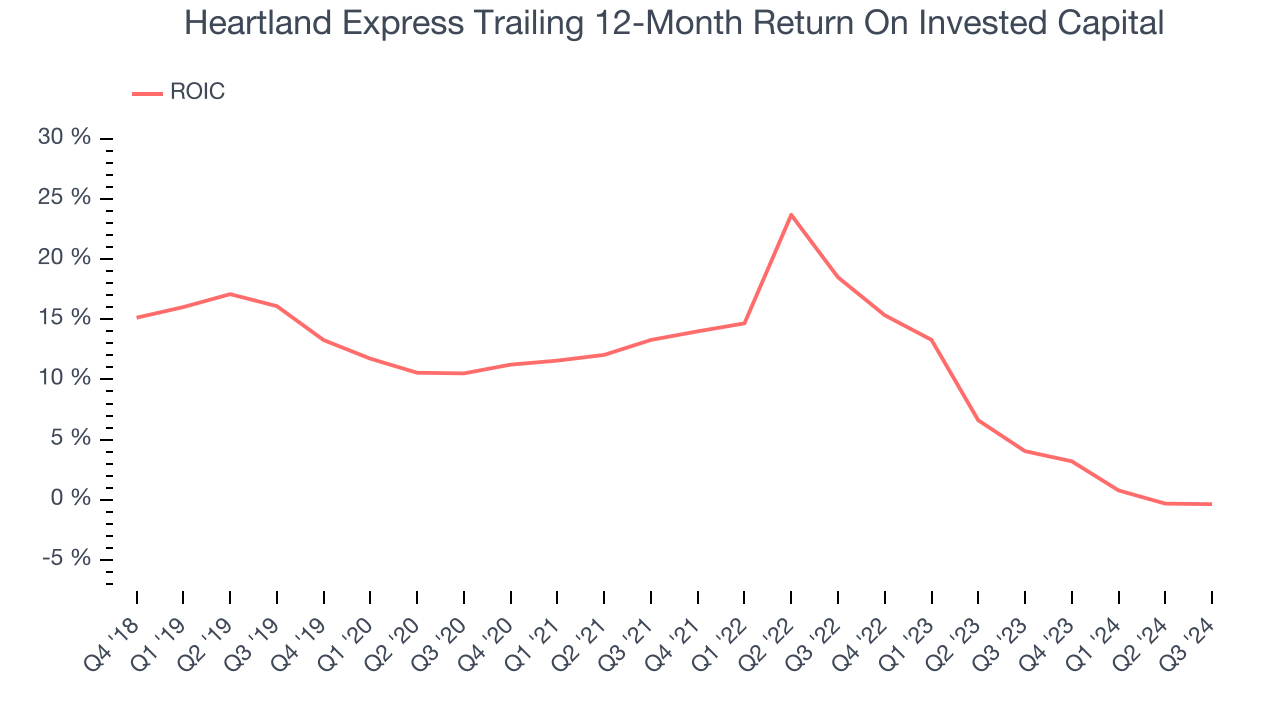

3. New Investments Fail to Bear Fruit as ROIC Declines

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

We typically prefer to invest in companies with high returns because it means they have viable business models, but the trend in a company’s ROIC is often what surprises the market and moves the stock price. Heartland Express’s ROIC has decreased significantly over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

Final Judgment

Heartland Express isn’t a terrible business, but it doesn’t pass our bar. That said, the stock currently trades at 20x forward EV-to-EBITDA (or $12.56 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - you can find better investment opportunities elsewhere. We’d recommend looking at Chipotle, which surprisingly still has a long runway for growth.

Stocks We Would Buy Instead of Heartland Express

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like Comfort Systems (+783% five-year return). Find your next big winner with StockStory today for free.