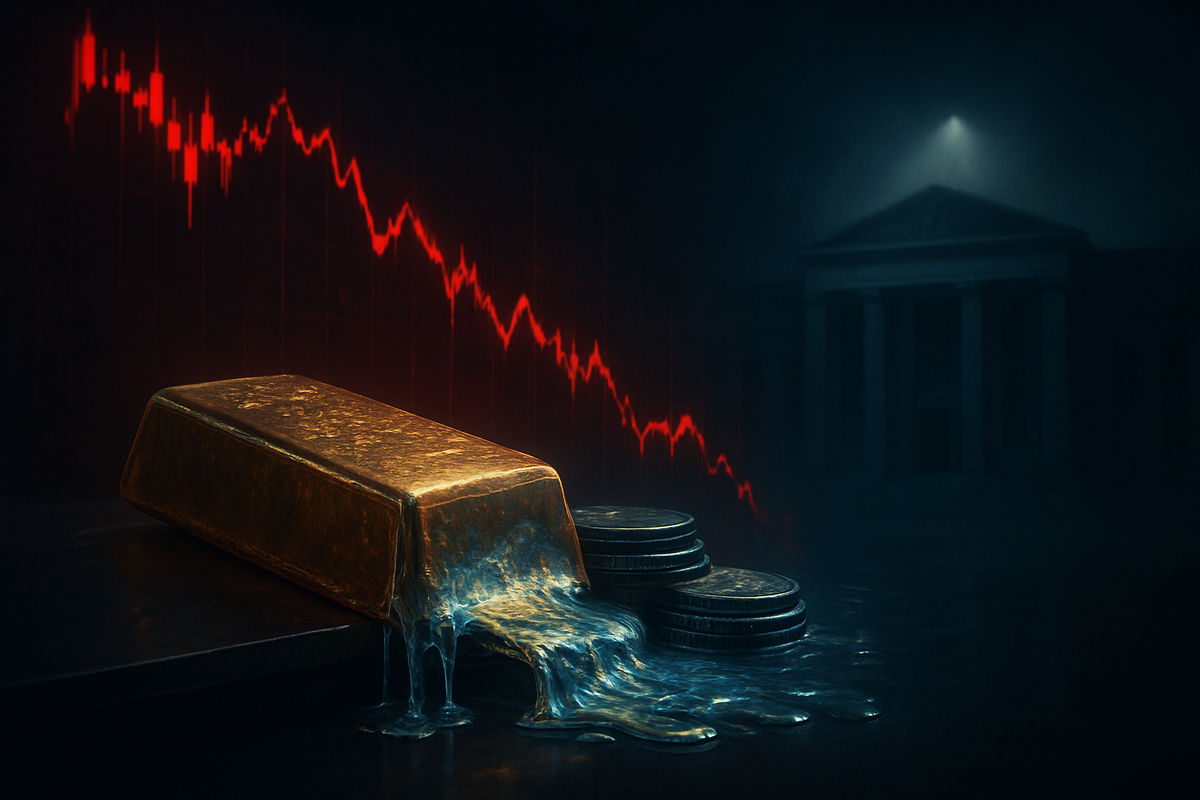

The global financial landscape was rocked this week by a phenomenon market participants are calling the "Warsh Shock." As the Federal Reserve prepares for a transition in leadership, a potent cocktail of hotter-than-expected inflation data and a pivot toward an ultra-hawkish, "disciplined" monetary regime has triggered a violent "dash for cash." This liquidity rupture has seen institutional investors liquidate their most liquid winning positions—primarily precious metals—to bolster balance sheets, leading to a massive sell-off across major exchange-traded funds and mining equities.

The immediate implications are stark: the traditional "safe-haven" narrative for gold and silver has been temporarily suspended as the assets serve a different, more painful role as the market's primary source of liquidity. On April 2, 2026, the selling reached a crescendo, forcing gold and silver prices to disconnect from their usual inflationary hedging roles and instead plummet alongside risk assets. This "mechanical selling" has left investors scrambling to assess the duration of this new, more restrictive era of American monetary policy.

A Volcker-Esque Pivot and the April Liquidity Flush

The seeds of the current turmoil were sown on January 30, 2026, with the nomination of Kevin Warsh to succeed Jerome Powell as Federal Reserve Chair. Warsh, long regarded as a monetary hawk, immediately signaled a "regime change" in policy through his "Warsh Doctrine." This approach prioritizes the "scarcity value" of the U.S. dollar and a principled commitment to sound money, moving away from the more discretionary, data-dependent stance of the past decade. The market's anxiety intensified as early 2026 inflation data proved unexpectedly "sticky," with March PPI figures exceeding estimates and April CPI nowcasts climbing to a startling 3.71%.

The breaking point arrived in the first week of April 2026. As the U.S. Dollar Index (DXY) surged past the 100.00 psychological threshold, institutional investors faced a mounting liquidity crisis. With equity markets beginning to wobble under the weight of rising real yields, hedge funds and large asset managers were forced into a "dash for cash" to meet margin calls and shore up solvency. This led to the massive liquidation of precious metal holdings, which had performed exceptionally well in the prior two years. The selling was not necessarily a reflection of a lack of confidence in gold, but rather a reflection of its high liquidity and substantial paper gains, making it the first "ATM" for distressed desks.

The market reaction was swift and brutal. On April 2, the VanEck Junior Gold Miners ETF (NYSE Arca: GDXJ) experienced a staggering 5.6% plunge in a single trading session. The high-beta nature of junior miners meant they bore the brunt of the "liquidity flush," as investors fled the operational leverage inherent in the sector. Simultaneously, the SPDR Gold Shares (NYSE Arca: GLD) dropped 3.2%, while the iShares Silver Trust (NYSE Arca: SLV) fell 3.1%, following a pattern of forced selling that saw silver settle near $71.44 per ounce—a sharp retreat from its early-year highs.

Winners and Losers in the New Monetary Order

The primary "losers" in this current environment are the non-yielding assets that thrived during the era of low real rates and expansionary balance sheets. Holders of the VanEck Gold Miners ETF (NYSE Arca: GDX) have seen their positions slide by 4.1% as the market rotates out of mining equities and into higher-carry instruments. Major mining giants like Newmont Corporation (NYSE: NEM) and Barrick Gold Corporation (NYSE: GOLD) are facing a dual headwind: falling spot prices for their primary outputs and a rising cost of capital as the "Warsh Fed" prepares to aggressively shrink its balance sheet.

Conversely, the "winners" in this shock are those holding liquid, dollar-denominated cash and short-term debt. Large commercial banks with significant liquidity buffers, such as JPMorgan Chase & Co. (NYSE: JPM) and Bank of America (NYSE: BAC), are positioned to benefit from higher net interest margins and the increased demand for dollar liquidity. Furthermore, the "disciplined monetary regime" has breathed new life into the "Carry Trade," where investors borrow in lower-rate currencies to invest in the now higher-yielding, sound-money backed U.S. dollar.

For institutional gold bulls, the current rupture is a painful lesson in market mechanics. While gold’s long-term value proposition remains tied to debt sustainability and geopolitical risk, its short-term price action is at the mercy of the dollar’s scarcity. The "Warsh Shock" has essentially turned the "inflation hedge" into a "collateral source," leaving investors who used excessive leverage in gold and silver exposed to rapid liquidations.

Wider Significance and Historical Precedents

This event marks a significant departure from the post-2008 monetary consensus. By shifting toward a "disciplined monetary regime," the Federal Reserve is signaling that it will no longer provide a "floor" for asset prices at the cost of the dollar's purchasing power. This "Warsh Shock" is being compared by many to the 1979 pivot by Paul Volcker, which similarly caused a liquidity rupture in commodities before eventually stabilizing the currency. The transition to "QT-for-Cuts"—a framework of shrinking the balance sheet while maintaining high real rates—is a paradigm shift that affects every corner of the global market.

The ripple effects extend far beyond precious metals. If the dollar remains the "only game in town" for liquidity, we can expect continued pressure on emerging market currencies and commodities across the board. Historically, such "liquidity ruptures"—like those seen in 2008 and March 2020—have seen gold and silver sell off first because they are the easiest things to sell for a profit when everything else is crashing. The current event fits this trend of "selling what you can, not what you want."

The regulatory and policy implications are also profound. A Fed that prioritizes "scarcity value" effectively curtails the "Fed Put" that has fueled risk-taking for nearly two decades. This forces a return to fundamentals and credit quality, potentially weeding out "zombie" companies that have survived solely on cheap credit. However, the risk remains that an overly aggressive "disciplined" regime could lead to a systemic credit event if the liquidity rupture in precious metals spreads to more sensitive debt markets.

The Path Forward: Strategic Pivots and Scenarios

In the short term, the market remains in a state of high volatility as it "prices out" the possibility of rate cuts in 2026. Investors should expect a "sawtooth" pattern in gold and silver as they oscillate between their roles as liquidity providers and long-term stores of value. The immediate focus for many funds will be a strategic pivot toward "quality and carry," prioritizing assets that generate yield in a high-rate environment rather than those that purely rely on price appreciation.

A potential scenario for the coming months involves a "normalization" of the gold-to-silver ratio. If the liquidity rupture stabilizes, precious metals may find a base at these lower levels, but any recovery will be capped by the "Warsh Doctrine’s" commitment to a strong dollar. Conversely, if the Fed overplays its hand and triggers a broader recession, we could see a renewed flight to quality that eventually decouples gold from the dollar, though this remains a long-term possibility rather than an immediate certainty.

The challenge for the "Warsh Fed" will be managing this transition without breaking the plumbing of the global financial system. The 5.6% plunge in GDXJ is a warning shot; it indicates that the outer rim of the risk curve is already under extreme duress. Market participants will be watching the Fed’s balance sheet closely to see if the "QT-for-Cuts" strategy is as sustainable as the incoming Chair suggests, or if the liquidity rupture forces a tactical retreat.

Wrap-Up: Navigating the Liquidity Rupture

The "Warsh Shock" has fundamentally reordered the priorities of the modern investor. The era of "reflation trades" has given way to an era of "solvency and scarcity." The liquidity rupture in gold and silver, highlighted by the sharp sell-offs in GLD, SLV, and the junior miners, serves as a stark reminder that even the most reliable safe havens are not immune to the gravitational pull of a strengthening dollar and a hawkish Federal Reserve.

Moving forward, the market will remain hyper-sensitive to any communication from the incoming Chair regarding the pace of balance sheet reduction. The key takeaway for investors is that in a "disciplined monetary regime," cash is no longer "trash"—it is a strategic asset and a necessary buffer against the mechanical liquidations of a dash for cash.

In the coming months, watch for the stabilization of the precious metals ETFs as a signal that the initial liquidity panic has subsided. However, until the inflation data cools significantly or the Fed softens its hawkish stance, the road back to the 2026 highs for gold and silver will be uphill, contested by the formidable strength of the "Warsh Dollar."

This content is intended for informational purposes only and is not financial advice