New York, NY – November 28, 2025 – The global commodity markets are currently exhibiting an unusual and striking divergence, with crude oil prices continuing their slump, down an estimated 13% this year, while a broad array of other commodities – from precious metals to industrial minerals crucial for the green energy transition – are experiencing robust rallies. This creates a fascinating and complex landscape for investors, businesses, and policymakers, signaling a potential reordering of global economic priorities and a profound shift in market dynamics.

This bifurcated market reflects a confluence of factors, including an oversupplied oil market, accelerating decarbonization efforts, persistent geopolitical tensions, and structural shifts in global demand. The immediate implications are far-reaching, impacting everything from corporate profitability and consumer spending to national budgets and long-term investment strategies, as the world grapples with the transition from a fuel-intensive to a material-intensive economy.

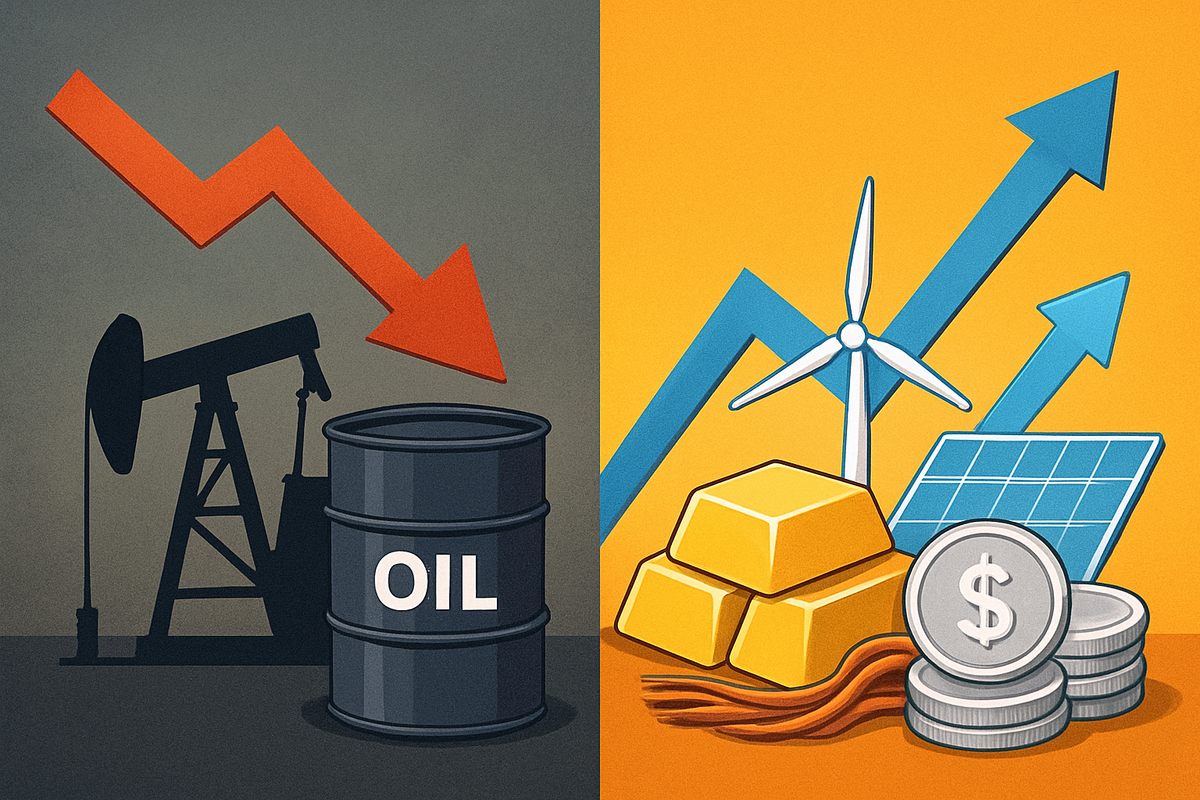

A Tale of Two Markets: Oil's Retreat and the Broad-Based Commodity Ascent

Throughout 2025, the narrative in commodity markets has been dominated by two contrasting storylines. On one side, crude oil, traditionally a bellwether for global economic health, has been steadily losing ground. Brent crude is trading around $62.85 per barrel, while West Texas Intermediate (WTI) hovers near $59.47 per barrel. Both benchmarks have seen consistent monthly declines, with the year-to-date slump of approximately 13% putting significant pressure on the energy sector. This downturn is primarily attributed to a substantial oversupply, with global oil production, particularly from non-OPEC+ nations like the United States and Brazil, surging to record highs, outpacing a more moderate growth in global demand. Easing geopolitical fears, particularly regarding the Russia-Ukraine conflict, and a strengthening U.S. dollar have further contributed to the bearish sentiment.

In stark contrast, the broader commodity market, as evidenced by the Bloomberg Commodity Total Return Index, has rallied by an impressive 15% in 2025, reaching levels not seen since mid-2022. Precious metals have been star performers, with gold (NYSE: NEM) surging by an astounding 49% year-to-date to trade near $3,919 per ounce in early October, while silver (NYSE: AG) has outpaced it with a remarkable 60% gain, reaching approximately $47.20 per ounce. This rally is underpinned by persistent safe-haven demand amidst global economic uncertainties and geopolitical instability, coupled with aggressive buying by central banks seeking to diversify reserves. Expectations of future interest rate cuts and a potentially weaker U.S. dollar have also made these non-yielding assets more attractive.

Industrial metals, critical for the burgeoning green energy transition, have also seen a constructive trend, with a year-to-date increase of around 13%. Copper (NYSE: FCX), in particular, is leading this resurgence, with forecasts suggesting prices could reach $11,000 per metric ton by year-end, driven by unprecedented demand from electrification, grid upgrades, and data center construction. Supply disruptions and years of underinvestment in mining have created a structural deficit, bolstering prices for copper, aluminum, and nickel. Even natural gas (Henry Hub futures) has experienced a significant month-over-month increase of approximately 33% by mid-November, fueled by expectations of a colder 2025-2026 winter and robust U.S. industrial demand. Agricultural commodities have shown a more mixed but generally positive performance, with broad strength in grains and soft commodities offsetting some livestock losses, though volatility remains high due to weather patterns and logistics.

Key players are reacting to this complex environment. OPEC+ nations face the delicate task of balancing market share with price stability, while major non-OPEC producers like the United States continue to ramp up output. Mining giants such as BHP Group (ASX: BHP), Rio Tinto (ASX: RIO), and Glencore (LSE: GLEN) are strategically positioned to capitalize on the surging demand for critical minerals. Initial market reactions have seen a clear rotation of capital, with investors shifting away from traditional energy plays towards sectors poised to benefit from lower energy costs or the rising tide of green technology. Analysts are rapidly revising their forecasts, with many debating whether the accelerated decline in oil demand signals an earlier "peak oil demand" than previously anticipated.

Winners and Losers in the Commodity Crossroads

The diverging commodity market creates a clear delineation of winners and losers across various industries, profoundly impacting their operational costs, revenue streams, and ultimately, their stock performance.

On the losing side, companies with direct exposure to slumping oil prices are feeling the pinch. Oil and Gas Exploration & Production (E&P) companies like ExxonMobil (NYSE: XOM), Chevron (NYSE: CVX), ConocoPhillips (NYSE: COP), and Devon Energy (NYSE: DVN) face reduced profitability from new projects, leading to potential cuts in capital expenditure and drilling activity. Smaller, highly leveraged producers are particularly vulnerable to financial strain. Similarly, oilfield services companies, which rely on E&P spending, are experiencing decreased demand and intense pricing pressure. While the impact on refining companies can be nuanced, a general oil slump driven by weaker demand could tighten "crack spreads" (refining margins), negatively affecting their profitability.

Conversely, companies that consume oil as a major input are reaping significant benefits. Airlines, for whom jet fuel is a substantial operating expense, are seeing a direct boost to their bottom lines. Carriers like Delta Air Lines (NYSE: DAL) and Southwest Airlines (NYSE: LUV) are likely to report improved profit margins and potentially higher stock valuations as investors anticipate enhanced financial performance. Shipping and freight companies, including maritime and trucking firms like FedEx (NYSE: FDX), also benefit from lower fuel costs, which reduce operational expenses and can enhance competitiveness. Chemical manufacturers, particularly those in petrochemicals, are experiencing reduced feedstock costs, leading to improved profit margins, especially for commodity chemicals.

However, the rally in other commodities presents its own set of winners and losers. Manufacturers heavily reliant on rising commodity inputs face increased costs. Battery and electric vehicle (EV) manufacturers such as Tesla (NASDAQ: TSLA), Panasonic (TYO: 6752), CATL (SHE: 300750), and General Motors (NYSE: GM) are grappling with surging lithium and nickel prices, which directly impact battery production costs. This could squeeze their profit margins or force them to pass costs onto consumers, potentially affecting sales. Similarly, cable and wire manufacturers, with significant copper input costs, face rising raw material expenses, necessitating price adjustments or the search for alternative materials.

On the other hand, mining companies focused on the rallying commodities are experiencing a boom. Copper miners like Freeport-McMoRan Inc. (NYSE: FCX) and Southern Copper Corporation (NYSE: SCCO) are seeing increased revenues and profitability, driven by the insatiable demand for electrification. Lithium miners such as Sociedad Química y Minera (NYSE: SQM) and Pilbara Minerals (ASX: PLS) are benefiting from the explosive growth in EV and battery storage markets. Gold miners like Newmont Corporation (NYSE: NEM) and Barrick Gold Corporation (NYSE: GOLD), along with silver miners such as Hecla Mining Company (NYSE: HL) and First Majestic Silver Corp. (NYSE: AG), are thriving amidst strong precious metal prices. These companies are witnessing enhanced profitability and strong stock performance, often leading to increased investment in exploration and production.

Wider Significance: A Reshaping of Global Economics

This commodity market divergence in late 2025 carries profound wider significance, signaling a fundamental reshaping of global economic structures and priorities. It underscores the accelerating pace of decarbonization and the energy transition, moving the world from a fuel-intensive to a material-intensive energy system. The decline in oil prices, even if partially due to oversupply, aligns with long-term trends of reduced fossil fuel demand as renewable energy and electric vehicles gain traction. Conversely, the rally in industrial metals like copper, lithium, and nickel is a direct consequence of the massive infrastructure build-out required for this green transition, from solar panels and wind turbines to EV batteries and smart grids.

Geopolitical shifts continue to play a dominant role. While easing tensions in some oil-producing regions contribute to lower crude prices, broader geopolitical fragmentation is driving nations to reassess resource security. This creates a premium for strategic resources, particularly critical minerals and certain agricultural commodities, as countries seek diversified and secure supply chains. Trade barriers, sanctions, and ongoing conflicts continue to disrupt traditional trade routes and sourcing models, leading to higher costs and increased volatility in non-oil commodities.

The ripple effects on the global economy are complex. For inflation, the picture is mixed: lower oil prices generally ease headline inflation by reducing energy and transportation costs, offering some relief to central banks. However, the sustained rally in industrial metals and certain agricultural products could exert upward pressure on core inflation, as these are essential inputs for manufacturing and food production. This makes the job of central banks particularly challenging in balancing price stability with economic growth. For consumer spending, cheaper oil acts like a "tax cut," potentially boosting discretionary income. Yet, if rising prices for food and manufactured goods (due to higher material costs) offset these savings, overall consumer purchasing power could remain constrained. In global trade, oil-importing nations stand to benefit from reduced energy bills, improving their terms of trade, while oil-exporting nations face fiscal strain, necessitating economic diversification. The ongoing re-evaluation of supply chain resilience is also redrawing global trade patterns, potentially leading to new, albeit sometimes costlier, trade corridors.

Regulatory and policy implications are significant. Governments of oil-exporting nations will likely face increased pressure to accelerate economic diversification away from hydrocarbon reliance. Oil-importing nations might seize the opportunity to rebuild fiscal reserves or channel investments into clean energy infrastructure. Central banks will need to carefully navigate monetary policy in an environment where disinflationary pressures from oil coexist with inflationary pressures from other commodities. Trade policies, particularly those related to critical minerals and strategic resources, are expected to intensify as nations prioritize resource security.

Historically, while exact parallels are rare, this divergence can be viewed through the lens of commodity supercycles. The current rally in industrial metals, driven by technological change and decarbonization, suggests the early stages of a "green energy supercycle," where demand for new materials supersedes that for traditional fossil fuels. This contrasts with the 2014-2016 oil price collapse, which saw a broader alignment of industrial commodity prices. The current scenario highlights a more nuanced inflationary environment compared to past broad commodity booms or busts.

What Comes Next: Navigating a Shifting Landscape

The outlook for the commodity market divergence suggests that this complex dynamic is likely to persist well into 2026 and beyond, presenting both formidable challenges and significant opportunities.

In the short-term (late 2025 to early 2026), oil prices are expected to remain under pressure, potentially averaging in the $50-60 per barrel range. The persistent global oversupply, coupled with slowing demand growth, will continue to cap any significant upward movement. Conversely, industrial metals like copper are forecast to maintain their bullish momentum, with prices potentially reaching $11,000 per metric ton, driven by strong demand and tightening supply. Precious metals, including gold and silver, are also anticipated to sustain their rally, buoyed by safe-haven demand and central bank purchasing. Natural gas is likely to remain volatile but generally strong, particularly in regions facing colder winters and geopolitical supply constraints.

Looking at the long-term (beyond 2026), the structural shifts become even more pronounced. Global oil demand is widely projected to peak before 2030 and then steadily decline as the energy transition accelerates. This implies a sustained bearish trend for crude oil over the coming decades. In stark contrast, the demand for critical industrial metals essential for the green transition is projected to surge dramatically, potentially tripling by 2030 and rising sevenfold by 2050. Lithium and nickel demand, specifically for EVs and battery storage, could grow by 40 times by 2040. This unprecedented demand, coupled with challenges in ramping up mining investment, points to a period of sustained high prices for these materials. Precious metals are expected to retain their role as crucial portfolio diversifiers and hedges against inflation and economic uncertainty.

Strategic pivots and adaptations will be critical for companies and governments. Oil and gas companies must accelerate diversification into renewable energy, carbon capture, and other sustainable ventures, while optimizing existing assets. Mining companies face the challenge and opportunity of meeting surging demand for critical minerals, requiring significant investment in sustainable extraction, processing, and recycling. Manufacturers consuming these metals will need to diversify supply chains, implement hedging strategies, and invest in material efficiency. Oil-exporting nations must intensify economic diversification to reduce reliance on volatile oil revenues, while oil-importing nations can leverage lower energy costs to invest in green infrastructure and strengthen fiscal positions.

Market opportunities will emerge in sectors tied to the green energy transition, critical mineral exploration and processing, and advanced materials. Emerging markets rich in these minerals, such as Chile for copper or Indonesia for nickel, could see substantial investment inflows. Conversely, challenges will persist for oil-dependent economies, which face fiscal stress and potential currency depreciation. Inflationary pressures from non-oil commodities could also pose a significant challenge for importing emerging markets, particularly if global interest rates remain elevated.

Several potential scenarios could unfold. A "Green Transition Acceleration" scenario sees oil prices slump even more aggressively as EV adoption and renewable energy deployment outpace forecasts, while industrial metals experience sustained, strong rallies. A "Global Economic Slowdown" could dampen demand across all commodities, muting rallies even for industrial metals. Geopolitical disruptions or a breakdown in OPEC+ cohesion could also introduce extreme volatility, temporarily overriding underlying trends.

Wrap-Up: A New Era for Commodity Markets

The commodity market divergence of late 2025 represents a pivotal moment, underscoring a fundamental reordering of global economic priorities. The era of cheap, abundant oil appears to be waning in significance, giving way to an unprecedented demand for the raw materials that will power the future.

Key takeaways include the persistent oversupply in oil markets driven by increased production and slowing demand, resulting in a notable 13% year-to-date slump. In stark contrast, precious metals like gold (up 49% YTD) and silver (up 60% YTD) have soared due to safe-haven demand and central bank activity. Industrial metals, particularly copper, are experiencing robust rallies, fueled by the accelerating global energy transition.

Moving forward, while aggregate commodity prices may see a modest contraction in 2026, this divergence is expected to persist. Oil prices are forecast to remain suppressed, potentially averaging around $60 per barrel in 2026. Precious metals and natural gas are likely to continue outperforming, while copper's structural bullishness, driven by long-term deficits and green energy demand, suggests sustained strength.

The lasting significance of this period lies in its confirmation of the global shift towards a material-intensive energy system. This transition, coupled with ongoing geopolitical complexities and supply chain vulnerabilities, will continue to drive increased volatility across commodity markets. It highlights the growing importance of commodities for portfolio diversification, acting as a hedge against both inflation and economic uncertainty. A critical lasting impact could also stem from the underinvestment in new mining and energy supply in recent years, potentially setting the stage for future tightness and higher prices beyond 2026.

Investors should vigilantly watch for several key factors in the coming months: central bank monetary policies, especially interest rate decisions by the U.S. Federal Reserve, which will impact the U.S. dollar and commodity pricing. Geopolitical developments, including trade policies and ongoing conflicts, remain crucial for potential supply disruptions. Global economic growth data, particularly from major commodity consumers like China, will influence industrial demand. OPEC+ production decisions will continue to shape the oil market. Finally, investors should monitor physical supply conditions for specific commodities, inflation trends, the indirect impact of AI demand on energy and materials, and unpredictable weather patterns affecting agricultural output.

This content is intended for informational purposes only and is not financial advice