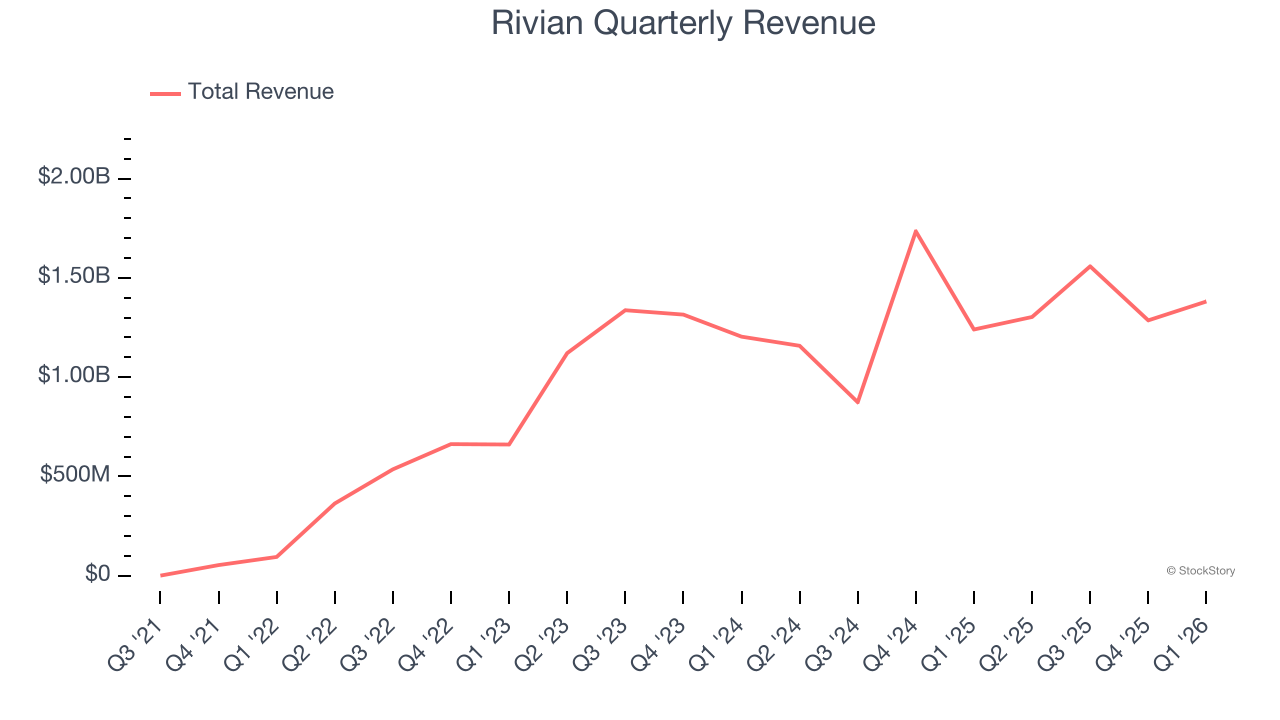

Electric vehicle manufacturer Rivian (NASDAQ: RIVN) fell short of the market’s revenue expectations in Q1 CY2026, but sales rose 11.4% year on year to $1.38 billion. Its GAAP loss of $0.33 per share was 53.9% above analysts’ consensus estimates.

Is now the time to buy Rivian? Find out by accessing our full research report, it’s free.

Rivian (RIVN) Q1 CY2026 Highlights:

- Revenue: $1.38 billion vs analyst estimates of $1.40 billion (11.4% year-on-year growth, 1% miss)

- EPS (GAAP): -$0.33 vs analyst estimates of -$0.72 (53.9% beat)

- Adjusted EBITDA: -$472 million (-34.2% margin, 43.5% year-on-year decline)

- EBITDA guidance for the full year is -$1.95 billion at the midpoint, above analyst estimates of -$2.01 billion

- Adjusted EBITDA Margin: -34.2%, down from -26.5% in the same quarter last year

- Free Cash Flow was -$1.08 billion compared to -$526 million in the same quarter last year

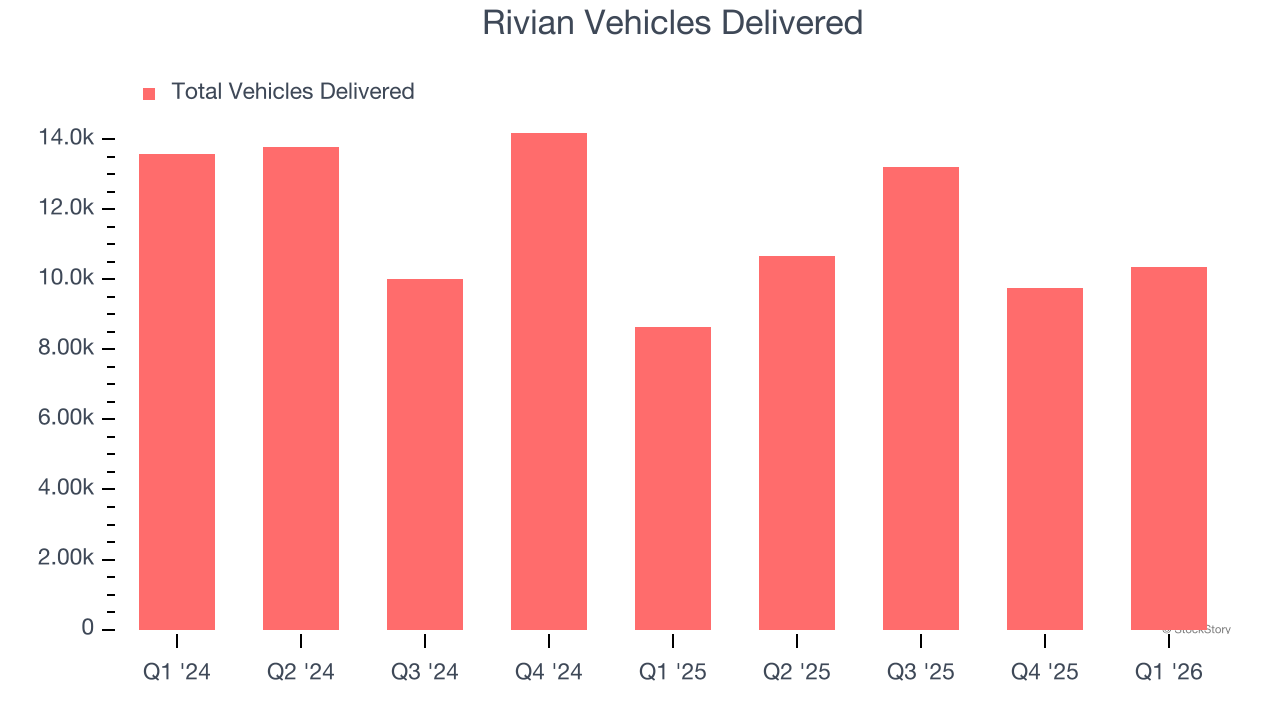

- Sales Volumes rose 20% year on year (-36.4% in the same quarter last year)

- Market Capitalization: $19.93 billion

RJ Scaringe, Rivian Founder and CEO, said: “With the launch of R2, we are excited to dramatically expand our market opportunity and have more people driving Rivians. The support of the Department of Energy for the $4.5 billion loan to build our Georgia facility enables Rivian to grow American jobs and establish stronger U.S. technology and manufacturing leadership while further scaling our customer base.”

Company Overview

The manufacturer of Amazon’s delivery trucks, Rivian (NASDAQ: RIVN) designs, manufactures, and sells electric vehicles and commercial delivery vans.

Revenue Growth

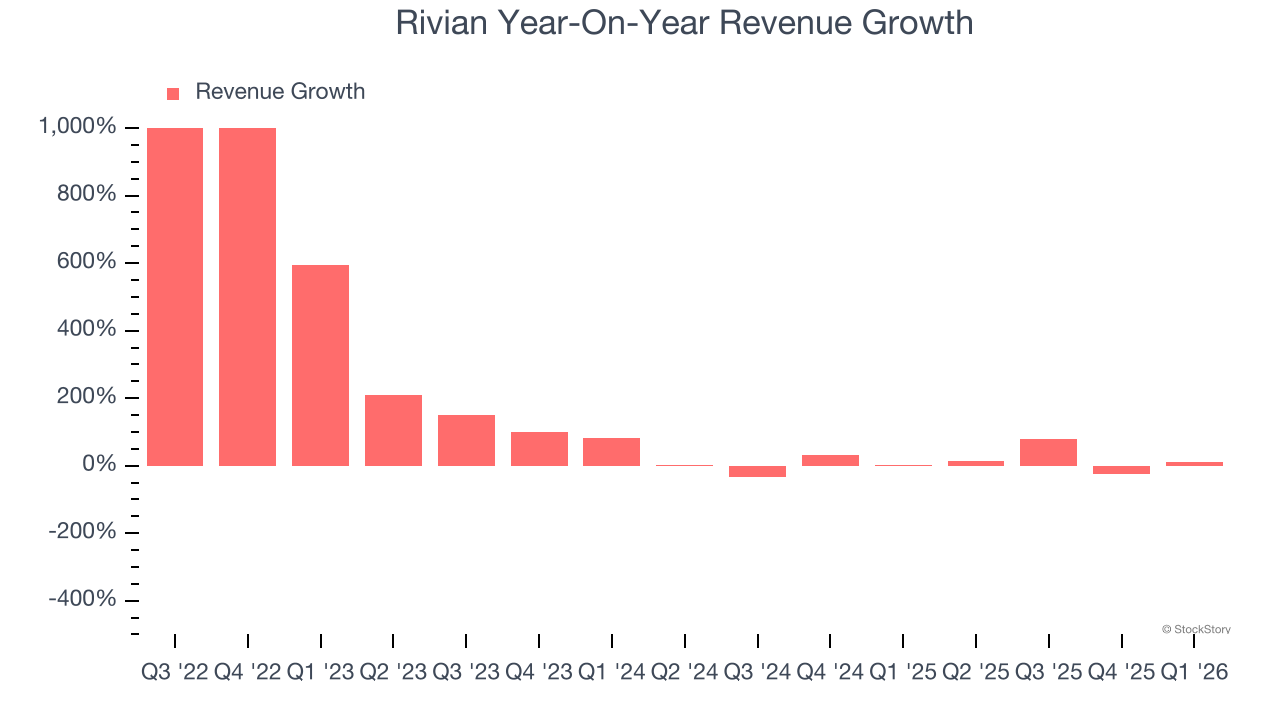

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Luckily, Rivian’s sales grew at an incredible 130% compounded annual growth rate over the last four years. Its growth beat the average industrials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within industrials, a stretched historical view may miss new industry trends or demand cycles. Rivian’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 5.4% over the last two years was well below its four-year trend.

Rivian also reports its number of vehicles delivered, which reached 10,365 in the latest quarter. Over the last two years, Rivian’s vehicles delivered were flat. Because this number is lower than its revenue growth, we can see the company benefited from price increases.

This quarter, Rivian’s revenue grew by 11.4% year on year to $1.38 billion but fell short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 48.2% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and indicates its newer products and services will fuel better top-line performance.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

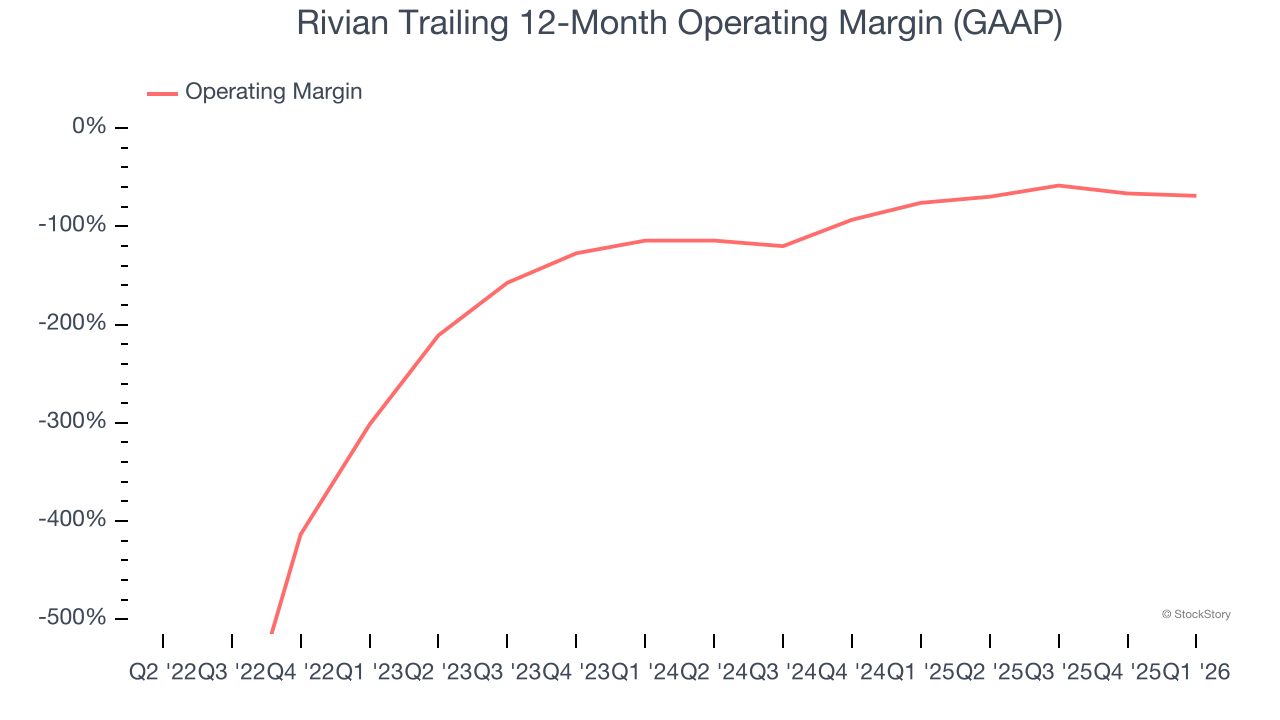

Rivian’s high expenses have contributed to an average operating margin of negative 135% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, Rivian’s operating margin rose over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to reach long-term profitability.

This quarter, Rivian generated a negative 63.8% operating margin.

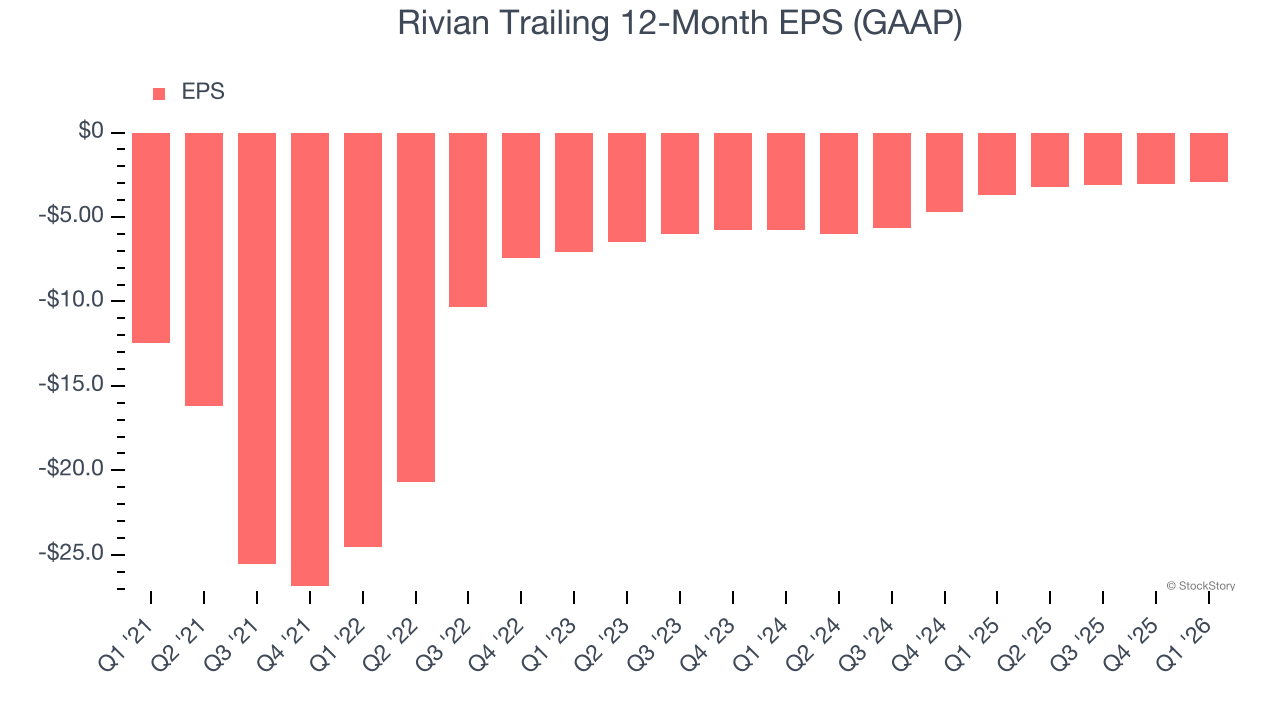

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Although Rivian’s full-year earnings are still negative, it reduced its losses and improved its EPS by 25.2% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability. We hope to see an inflection point soon, especially since it recently diluted shareholders by forming a $5.8 billion joint venture with Volkswagen in November 2024.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Rivian, its two-year annual EPS growth of 29% was higher than its five-year trend. We love it when earnings improve, but a caveat is that its EPS is still in the red.

In Q1, Rivian reported EPS of negative $0.33, up from negative $0.48 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Rivian to improve its earnings losses. Analysts forecast its full-year EPS of negative $2.92 will advance to negative $2.74.

Key Takeaways from Rivian’s Q1 Results

It was good to see Rivian beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. On the other hand, its revenue slightly missed. Zooming out, we think this was a good print with some key areas of upside. The stock remained flat at $16.60 immediately after reporting.

Rivian had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).