Viper Energy has had an impressive run over the past six months as its shares have beaten the S&P 500 by 19%. The stock now trades at $47.08, marking a 23.8% gain. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Following the strength, is VNOM a buy right now? Or is the market overestimating its value? Find out in our full research report, it’s free.

Why Are We Positive On VNOM?

Operating a business model that requires no drilling rigs or production equipment of its own, Viper Energy (NASDAQ: VNOM) owns mineral and royalty interests in oil and gas properties, collecting revenue when operators extract resources from land.

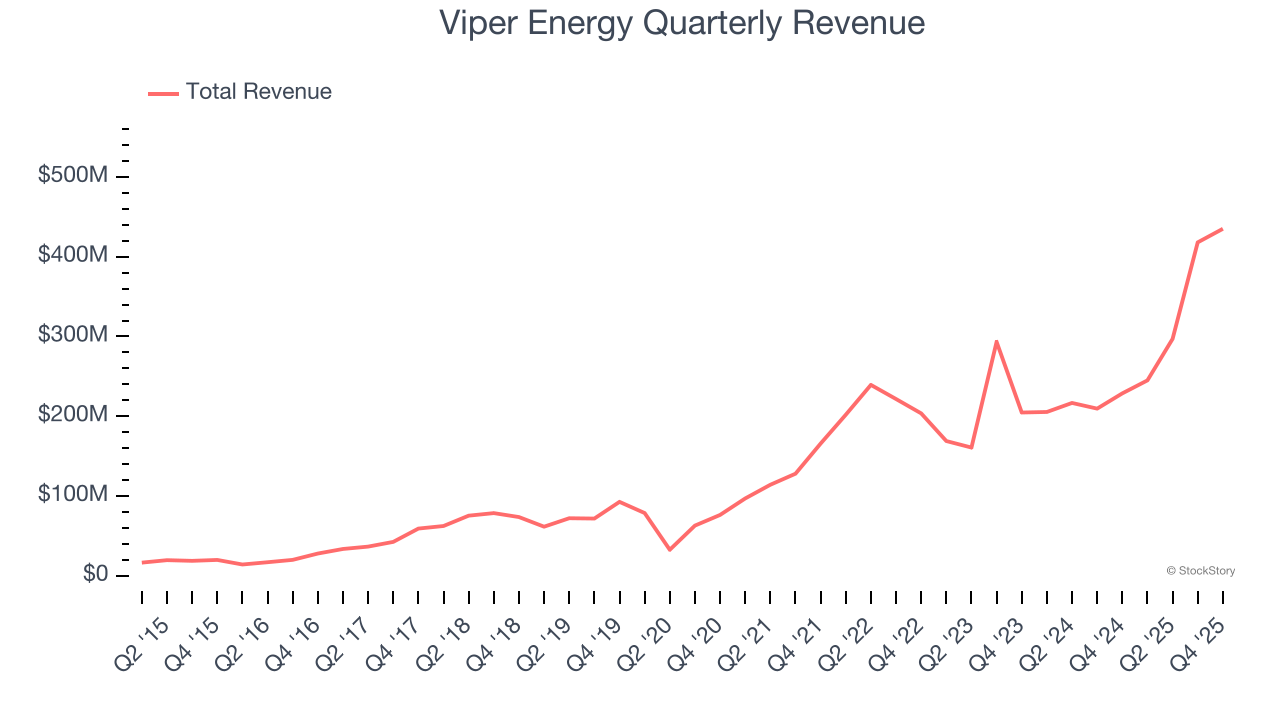

1. Skyrocketing Revenue Shows Strong Momentum

Cyclical industries such as Energy can make mediocre companies look great for a time, but a long-term view reveals which businesses can actually withstand and adapt to changing conditions. Luckily, Viper Energy’s sales grew at an incredible 41% compounded annual growth rate over the last five years. Its growth surpassed the average energy upstream and integrated energy company and shows its offerings resonate with customers.

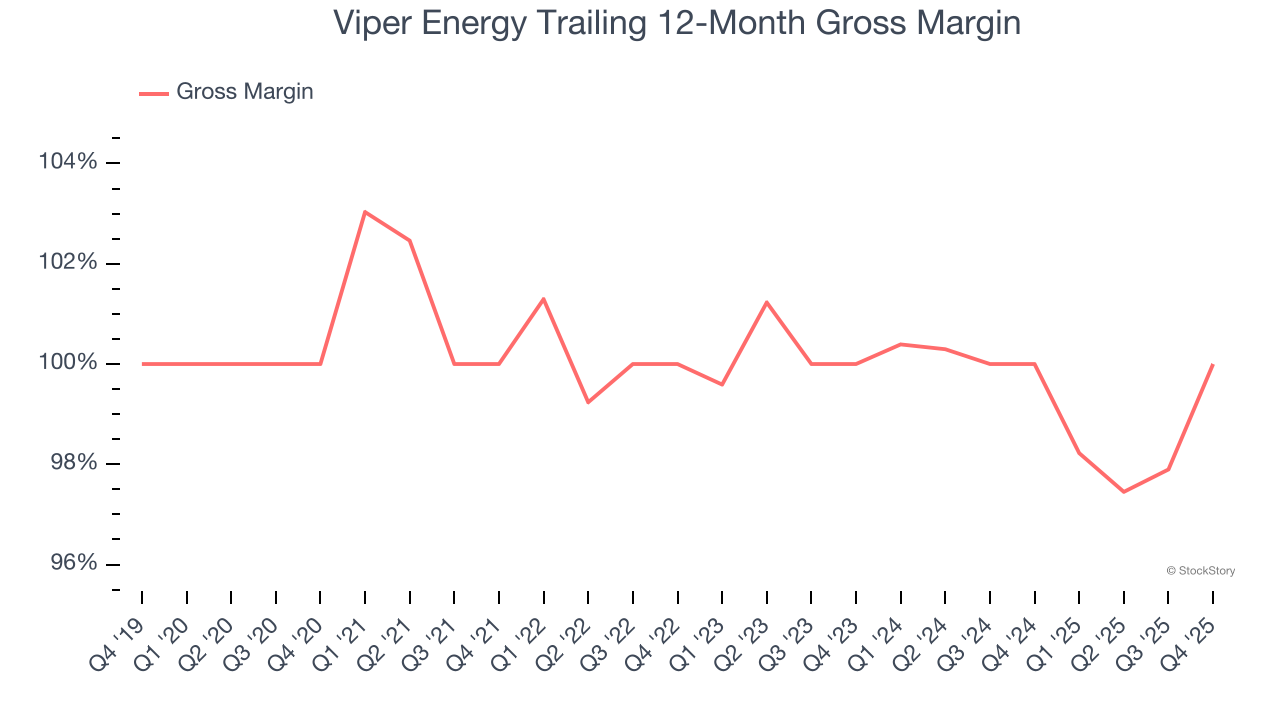

2. Elite Gross Margin Powers Best-In-Class Business Model

While energy gross margins can be distorted by commodity prices, hedging, and short-term cost swings, sustained margins across a full cycle reflect a producer’s underlying asset quality, infrastructure position, and cost structure.

Viper Energy, which averaged 100% gross margin over the last five years, exhibits enviable unit economics in the sector. It means the company will remain profitable at lower commodity prices than peers with inferior gross margins and serves as an advantaged starting point for ultimate operating profits and free cash flow generation.

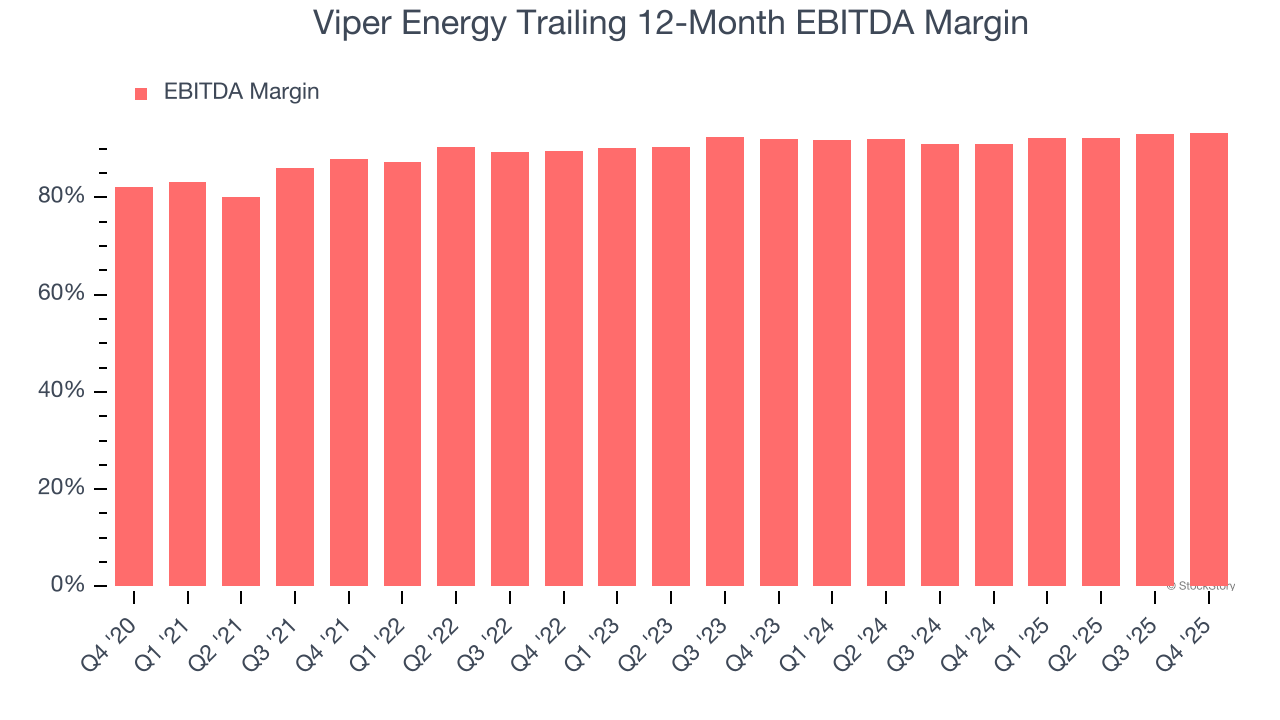

3. EBITDA Margin Rising, Profits Up

Adjusted EBITDA margin captures the true operating profitability of an energy producer by removing accounting noise around depletion and capitalized drilling costs. It reveals how much cash the asset base generates before capital structure and reinvestment requirements shape reported earnings.

Analyzing the trend in its profitability, Viper Energy’s EBITDA margin rose by 5.4 percentage points over the last year, as its sales growth gave it operating leverage. Its EBITDA margin for the trailing 12 months was 93.3%.

Final Judgment

These are just a few reasons Viper Energy is a high-quality business worth owning, and with its shares beating the market recently, the stock trades at 17.8× forward P/E (or $47.08 per share). Is now the time to initiate a position? See for yourself in our in-depth research report, it’s free.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.