As the Q4 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the consumer discretionary - leisure products industry, including YETI (NYSE: YETI) and its peers.

The Consumer Discretionary sector, by definition, is made up of companies selling non-essential goods and services. When economic conditions deteriorate or tastes shift, consumers can easily cut back or eliminate these purchases. For long-term investors with five-year holding periods, this creates a structural challenge: the sector is inherently hit-driven, with low switching costs and fickle customers. As a result, only a handful of companies can reliably grow demand and compound earnings over long periods, which is why our bar is high and High Quality ratings are rare. Leisure products companies manufacture recreational goods such as bicycles, marine vessels, fitness equipment, camping gear, and musical instruments. Tailwinds include heightened outdoor-activity participation, health-and-wellness awareness, and periodic innovation cycles that drive trade-up purchases. Headwinds are pronounced: demand is highly discretionary and sensitive to economic cycles—consumers readily defer big-ticket leisure purchases during downturns. Post-pandemic normalization has created excess channel inventory after demand surged then retreated. Raw-material and shipping cost inflation squeezes margins, while competition from low-cost imports and a fragmented market make pricing power elusive for most players.

The 12 consumer discretionary - leisure products stocks we track reported a strong Q4. As a group, revenues beat analysts’ consensus estimates by 4.6% while next quarter’s revenue guidance was 1.8% below.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 11.8% since the latest earnings results.

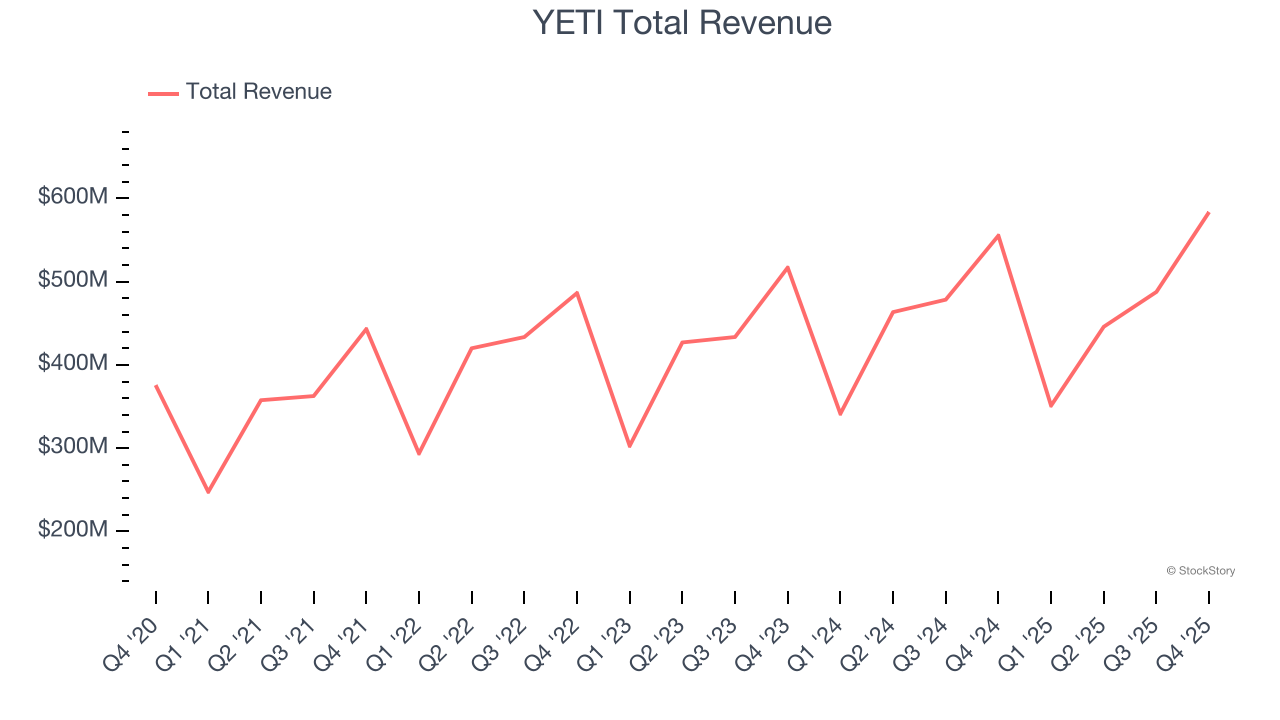

YETI (NYSE: YETI)

Founded by two brothers from Texas, YETI (NYSE: YETI) specializes in durable outdoor goods including coolers, drinkware, and other gear tailored to adventure enthusiasts.

YETI reported revenues of $583.7 million, up 5.1% year on year. This print was in line with analysts’ expectations, but overall, it was a mixed quarter for the company with a beat of analysts’ EPS estimates but full-year EPS guidance missing analysts’ expectations.

Matt Reintjes, President and Chief Executive Officer, commented, “Q4 was our strongest quarter of the year as the YETI brand continued to build momentum. We’re seeing solid demand, our teams are executing with discipline, and the strategy we’ve been building over the last few years is showing through in the numbers and outlook. Across categories and channels, the business is more balanced and resilient than it’s ever been. A big part of that strength comes from the work we’ve done on innovation, strengthening our brand globally, and expanding internationally. These long-term growth pillars are producing tangible results and give us tremendous confidence as we head into 2026. These are the reasons we expect to continue to drive strong top and bottom-line results while generating over $200 million in free cash flow. We are playing in a large global addressable market, which provides us with a significant runway for growth as we continue to bring new consumers to YETI.”

Unsurprisingly, the stock is down 26.2% since reporting and currently trades at $36.50.

Is now the time to buy YETI? Access our full analysis of the earnings results here, it’s free.

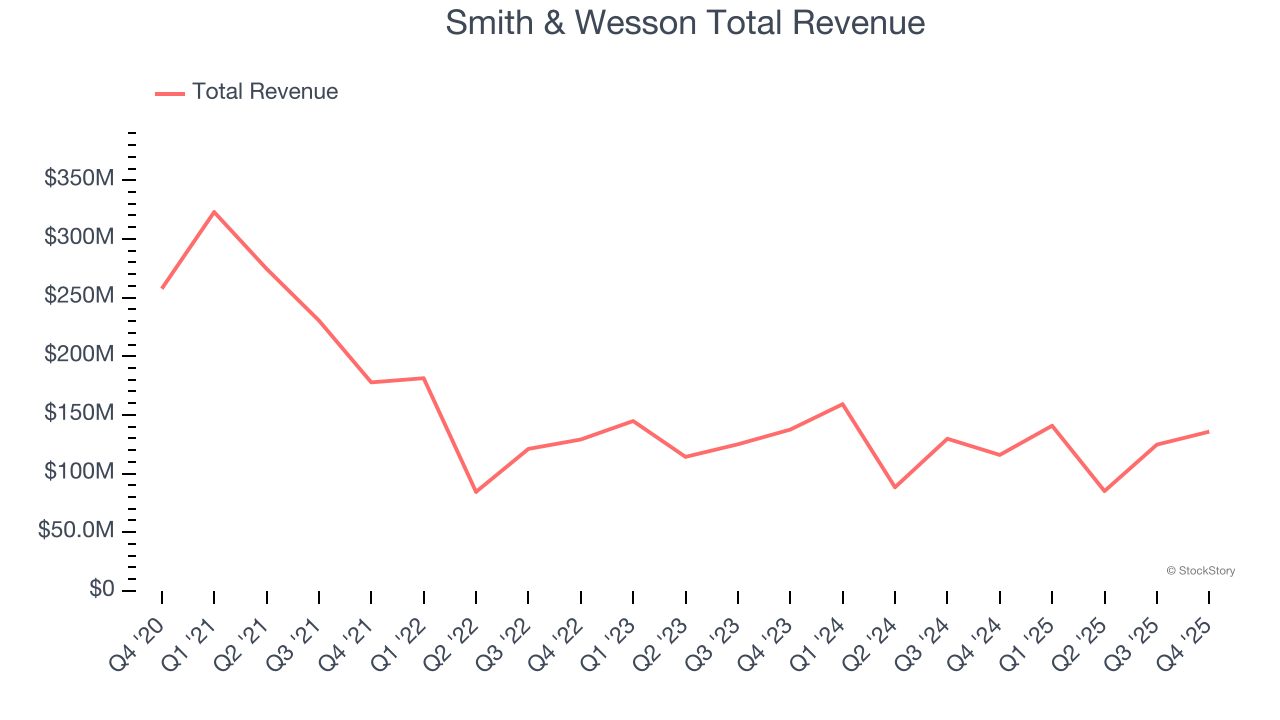

Best Q4: Smith & Wesson (NASDAQ: SWBI)

With a history dating back to 1852, Smith & Wesson (NASDAQ: SWBI) is a firearms manufacturer known for its handguns and rifles.

Smith & Wesson reported revenues of $135.7 million, up 17.1% year on year, outperforming analysts’ expectations by 8.1%. The business had an incredible quarter with a beat of analysts’ EPS estimates and a solid beat of analysts’ EBITDA estimates.

Smith & Wesson delivered the fastest revenue growth among its peers. The market seems happy with the results as the stock is up 16.8% since reporting. It currently trades at $13.77.

Is now the time to buy Smith & Wesson? Access our full analysis of the earnings results here, it’s free.

Slowest Q4: Harley-Davidson (NYSE: HOG)

Founded in 1903, Harley-Davidson (NYSE: HOG) is an American motorcycle manufacturer known for its heavyweight motorcycles designed for cruising on highways.

Harley-Davidson reported revenues of $496.2 million, down 27.8% year on year, exceeding analysts’ expectations by 3.4%. Still, it was a softer quarter as it posted a significant miss of analysts’ adjusted operating income estimates and a significant miss of analysts’ EBITDA estimates.

Harley-Davidson delivered the slowest revenue growth in the group. As expected, the stock is down 14.6% since the results and currently trades at $17.21.

Read our full analysis of Harley-Davidson’s results here.

MasterCraft (NASDAQ: MCFT)

Started by a waterskiing instructor, MasterCraft (NASDAQ: MCFT) specializes in designing, manufacturing, and selling sport boats.

MasterCraft reported revenues of $71.76 million, up 13.2% year on year. This print beat analysts’ expectations by 4.1%. It was a stunning quarter as it also logged a beat of analysts’ EPS estimates and an impressive beat of analysts’ EBITDA estimates.

The stock is down 15.7% since reporting and currently trades at $19.49.

Read our full, actionable report on MasterCraft here, it’s free.

Latham (NASDAQ: SWIM)

Started as a family business, Latham (NASDAQ: SWIM) is a global designer and manufacturer of in-ground residential swimming pools and related products.

Latham reported revenues of $99.95 million, up 14.5% year on year. This result surpassed analysts’ expectations by 4.4%. Overall, it was a stunning quarter as it also put up a beat of analysts’ EPS estimates and a solid beat of analysts’ EBITDA estimates.

The stock is down 10.6% since reporting and currently trades at $5.76.

Read our full, actionable report on Latham here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.