October 10, 2025 - The technology sector experienced a significant downturn today as renewed threats of tariffs between the United States and China sent jitters across global financial markets. The tech-heavy Nasdaq Composite led the declines, with investors reacting swiftly to the prospect of escalating trade tensions that promise to disrupt intricate supply chains and restrict market access for some of the world's largest tech giants.

The immediate fallout saw major U.S. indexes slide, highlighting deep-seated concerns over the economic implications of a protracted trade conflict. Companies heavily reliant on cross-border trade and manufacturing, particularly those with significant exposure to both the U.S. and Chinese markets, faced intense selling pressure, signaling a challenging period ahead for innovation and profitability in the tech industry.

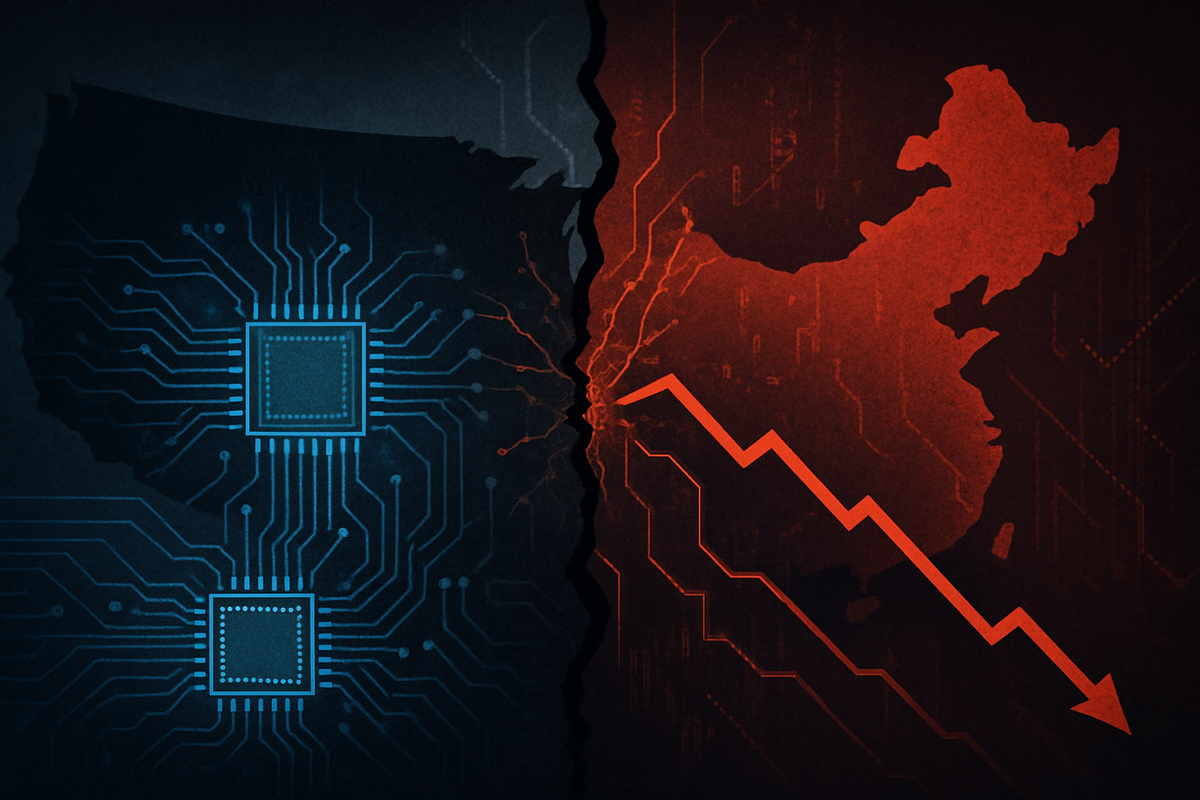

Escalating Trade War: A Day of Reckoning for Technology

Today's market upheaval on October 10, 2025, was directly triggered by the re-emergence of aggressive tariff rhetoric, primarily fueled by propositions from former President Donald Trump regarding "massive" new tariffs on Chinese products. This rhetoric comes in direct response to China's expanded export controls on critical materials and technologies, including rare earth elements essential for advanced semiconductors and electric vehicle batteries. These tit-for-tat measures have intensified what analysts are calling an escalating "tech war."

The timeline leading to this moment has been characterized by a series of strategic moves and counter-moves. Over recent years, the U.S. has increasingly imposed export controls, limiting China's access to advanced semiconductor technologies, including AI chips and chipmaking tools, citing national security concerns. In parallel, China has retaliated with its own restrictions, notably on rare earth elements, creating a complex and volatile environment. The proposition of new tariffs on this date represents a significant escalation, pushing the trade dispute into a more aggressive phase.

Key players in this unfolding drama include the U.S. government, particularly figures advocating for protectionist policies, and the Chinese government, which is strategically leveraging its control over critical resources. Within the industry, major stakeholders range from chipmakers like Nvidia (NASDAQ: NVDA) and Advanced Micro Devices (NASDAQ: AMD) to consumer electronics giants such as Apple (NASDAQ: AAPL), all of whom face direct impacts on their supply chains, manufacturing costs, and market strategies. Initial market reactions were overwhelmingly negative, with the PHLX Semiconductor Index plummeting by 4.1%, underscoring the severe hit to chipmakers.

Corporate Fortunes: Who Wins and Who Loses in the Tariff Crossfire

The renewed US-China tariff threats are poised to create distinct winners and losers within the technology sector, fundamentally reshaping corporate strategies and market valuations. Companies with diversified supply chains and less reliance on single-country manufacturing or consumer markets are likely to weather the storm more effectively, while those deeply integrated into the US-China economic nexus face significant headwinds.

Among the most vulnerable are companies like Apple (NASDAQ: AAPL), which has a substantial manufacturing footprint in China and a critical dependence on the Chinese consumer market. Any tariffs on finished goods or components would directly increase production costs, potentially impacting profitability and consumer pricing. Similarly, semiconductor companies such as Advanced Micro Devices (NASDAQ: AMD), Nvidia (NASDAQ: NVDA), and Qualcomm (NASDAQ: QCOM) are highly susceptible due to their reliance on global supply chains for manufacturing and their significant sales presence in China. China's new restrictions on rare earth elements, vital for their products, directly threaten their ability to source essential materials, leading to potential production delays and increased input costs. Qualcomm, already facing an antitrust probe in China, exemplifies the multi-faceted challenges these companies confront.

Conversely, companies that have already begun to diversify their manufacturing away from China, or those with a stronger domestic focus or alternative market access, might find themselves in a relatively stronger position. Furthermore, some software and services companies, less dependent on physical goods supply chains, may be more insulated from direct tariff impacts, though they could still suffer from broader economic slowdowns or retaliatory measures affecting market access. The ongoing tensions are also spurring a trend towards reshoring or nearshoring, which could benefit domestic manufacturing and logistics providers in the long run, albeit at a higher initial cost.

Broader Implications: A Fragmenting Global Tech Landscape

The re-escalation of US-China tariff threats on October 10, 2025, is not an isolated incident but rather a significant acceleration of broader industry trends towards technological fragmentation and increased protectionism. This event underscores the growing emphasis on national economic security, compelling tech companies to adapt to an increasingly bifurcated global market. The long-term implications suggest a fundamental shift away from deeply integrated global supply chains towards more regionalized and resilient models.

The potential ripple effects extend far beyond the direct participants. Competitors and partners across the tech ecosystem will be forced to re-evaluate their own strategic alliances and supply chain vulnerabilities. For instance, companies that supply components to major tech players impacted by tariffs might see reduced orders or pressure to relocate production. This could trigger a domino effect, leading to a broader restructuring of the global tech manufacturing and distribution network. Regulatory bodies in both the U.S. and China are likely to continue enacting policies that reinforce domestic industries and restrict foreign competition, further cementing the divide. Historically, similar trade disputes, though perhaps not as technologically focused, have demonstrated how protectionist measures can stifle innovation, increase consumer costs, and slow economic growth, drawing parallels to the current situation.

This event also highlights the increasing politicization of technology. Governments are now actively using economic levers, such as tariffs and export controls, to gain strategic advantages in critical areas like AI, quantum computing, and advanced materials. This shift is forcing companies to navigate a complex geopolitical landscape where business decisions are inextricably linked to national interests, potentially leading to the creation of distinct technological ecosystems—one centered around the U.S. and its allies, and another around China.

The Road Ahead: Navigating a New Era of Tech Geopolitics

Looking ahead, the renewed US-China tariff threats signal a turbulent short-term outlook for the technology sector, with potential for continued market volatility and downward pressure on stock valuations. In the long term, companies will be forced into strategic pivots, accelerating the diversification of supply chains away from China and exploring new markets to mitigate risks. This could involve significant capital expenditure in new manufacturing facilities in Southeast Asia, India, or even back in their home countries.

Market opportunities may emerge for companies that can offer resilient supply chain solutions, advanced automation to reduce labor reliance, or those capable of localizing production and product offerings for specific regional markets. Furthermore, companies focused on developing technologies that reduce dependence on critical materials controlled by a single nation could see increased investment and demand. Challenges will include higher operating costs, potential delays in product development due to supply chain reconfigurations, and the complex task of managing two distinct business operations for U.S. and non-U.S. markets.

Potential scenarios range from a continued, gradual escalation of trade tensions, leading to a "decoupling" of the tech economies, to periods of de-escalation driven by economic necessity or political shifts. A worst-case scenario could involve a full-blown trade war with widespread tariffs and export bans, severely impacting global economic growth and technological innovation. Conversely, a more optimistic scenario might see a negotiated settlement, though the underlying geopolitical competition for technological supremacy is likely to persist, ensuring a sustained focus on national resilience and strategic autonomy in tech.

MarketMinute Wrap-Up: Resilience Amidst Uncertainty

Today's market performance on October 10, 2025, serves as a stark reminder of the profound impact that geopolitical tensions, particularly the US-China trade dispute, can have on the highly interconnected technology sector. The immediate takeaway is clear: renewed tariff threats equate to heightened uncertainty, increased operational costs, and significant risks to profitability for tech companies deeply embedded in global supply chains. Investors witnessed a sharp sell-off, with chipmakers and consumer electronics giants bearing the brunt of the market's anxiety.

Moving forward, the market will likely remain highly sensitive to any developments in US-China relations. The underlying trend towards supply chain diversification and technological localization is expected to accelerate, fundamentally altering how tech products are designed, manufactured, and distributed. Companies that demonstrate agility in adapting to these shifts, investing in resilient supply chains, and strategically navigating bifurcated markets will be best positioned for long-term success.

Investors should closely monitor policy announcements from both the U.S. and Chinese governments, particularly regarding tariffs, export controls, and industrial policies. Furthermore, attention should be paid to corporate earnings reports for indications of how companies are managing increased costs and supply chain disruptions. The lasting impact of this period will likely be a more fragmented yet potentially more resilient global tech landscape, where geopolitical considerations are as critical as technological innovation.

This content is intended for informational purposes only and is not financial advice