Intel (INTC) just delivered one of its strongest quarters in years, and at least one prominent money manager is not even thinking about cashing out. According to reports, KKM Financial CEO Jeff Kilburg has held his Intel position through years of doubt and is now more convinced than ever.

Kilburg's reasoning goes well beyond quarterly earnings. To him, Intel is a foundational piece of the U.S. economy. Let’s take a closer look.

Intel's Q1 Earnings Beat Blew Past Wall Street

Intel's first-quarter results came in well above what analysts had expected, marking the sixth-straight quarter the company beat its financial targets. Revenue reached $13.6 billion, more than $1.4 billion above the midpoint of Intel's own guidance. The company's data center and AI (DCAI) segment posted revenue of $5.1 billion in Q1 2026, up 22% year-over-year (YOY). Server CPU demand is so high that Intel CEO Lip-Bu Tan said supply is still struggling to keep up with customer demand.

"Demand continues to outpace our growing supply," remarked CFO David Zinsner during the earnings call.

For Q2, Intel guided revenue between $13.8 billion and $14.8 billion, with DCAI expected to grow in the double digits sequentially. Shares of INTC stock surged almost 24% following the results, briefly touching $85.

Why KKM Is Bullish on INTC Stock

Kilburg noted that Intel has now gained significantly since the start of 2025. Over the past 52 weeks, shares of INTC stock are up more than 360%, as well as up more than 150% year-to-date (YTD). He describes the tech giant as an essential American asset, not just a chip stock.

This conviction has grown alongside Intel's foundry turnaround. The foundry division, which was once a drag on the business with no profit, is now expected to generate $3 billion next year. Kilburg pointed to the Terafab development as the deal that meaningfully shifted the company's trajectory.

On the earnings call, Tan confirmed Intel's recent partnership with SpaceX, xAI, and Tesla (TSLA) to support Terafab. He and Elon Musk share the view that global semiconductor supply is not keeping pace with demand, and the two are exploring ways to improve manufacturing efficiency at scale.

This kind of deal signals a different Intel from the one that traded below $20 not long ago, when the U.S. government stepped in as a stakeholder. Kilburg acknowledged the current media attention makes him slightly cautious, but maintained that the momentum is real.

The CPU Is Back at the Center of the AI Boom

One of the bigger shifts driving Intel's comeback is happening inside AI infrastructure itself. For years, graphics processing units (GPUs) dominated the conversation around artificial intelligence. But the workloads are changing as training models require massive numbers of GPUs. Running those models, and especially running AI agents that make decisions in real time, requires far more central processing units (CPUs).

Intel says the ratio of GPUs to CPUs in AI systems has shifted from roughly 8:1 in training environments to closer to 4:1 or 3:1 in inference settings. In agentic AI, that ratio could flip further toward parity or even favor CPUs. "The CPU now serves as the orchestration layer and critical control plane for the entire AI stack," Tan said on the call.

Intel signed multiple long-term agreements in Q1, including a deal with Alphabet's (GOOGL) Google to supply Xeon processors. Zinsner said these contracts typically run three to five years with committed volumes and pricing, giving the company real revenue visibility.

The company's ASIC business, which builds purpose-built chips tailored to specific customer workloads, is already running at over $1 billion annually and growing fast. Kilburg summed it up plainly: this is a workhorse company that has earned its place back at the table. "I want to own it," Kilburg said.

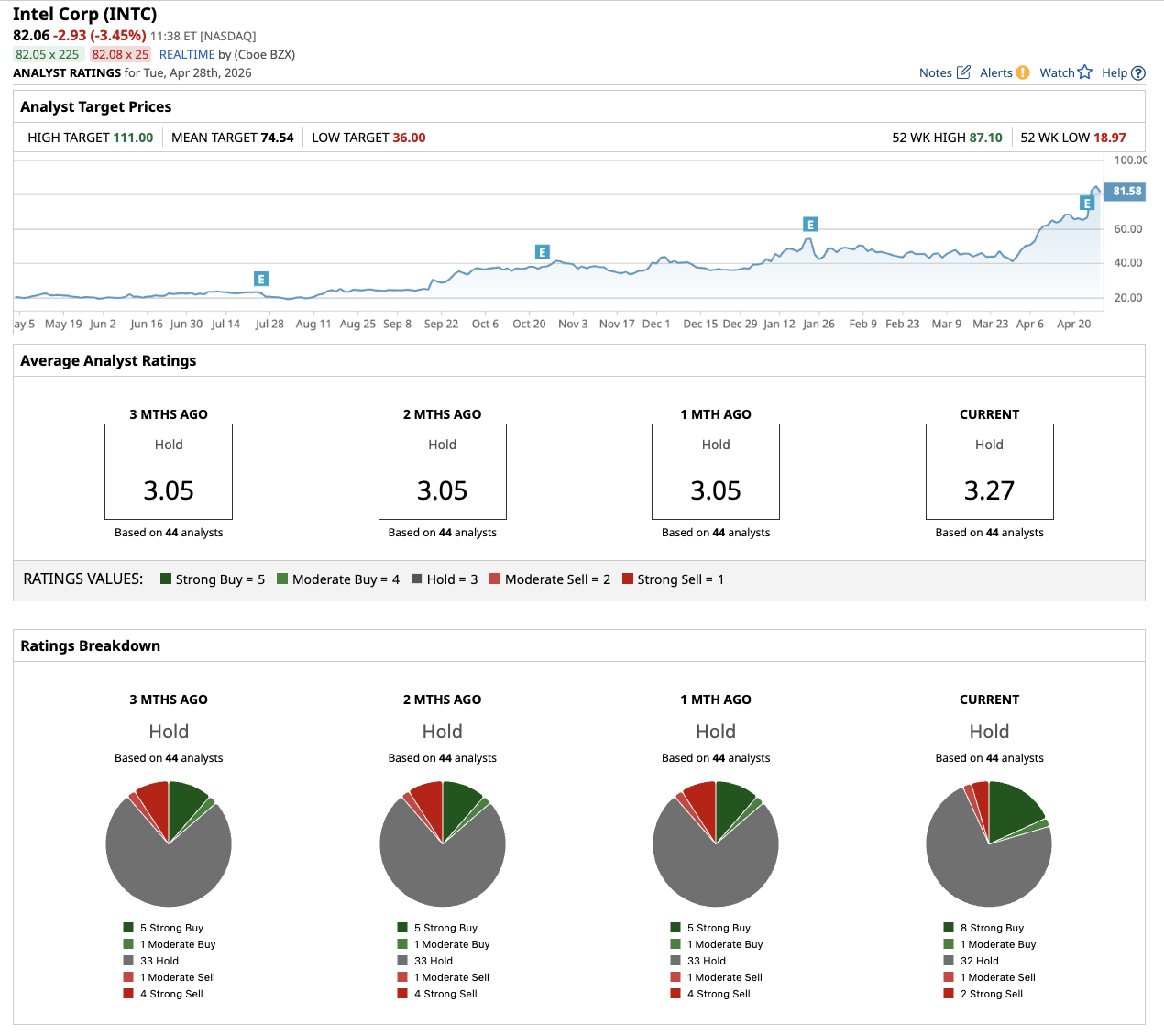

What Do Analysts Think of INTC Stock?

Analysts tracking INTC stock forecast adjusted earnings to expand from $0.42 per share in 2025 to $4.16 per share in 2030. Intel earns a consensus “Hold” rating currently. Out of the 44 analysts covering Intel stock, nine recommend a “Strong Buy”, one recommends a “Moderate Buy,” 31 recommend a “Hold” rating, one recommends a “Moderate Sell,” and two recommend a “Strong Sell” rating. The average price target for INTC stock is $76.19, implying 19% potential downside from current levels.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- A $20 Billion Reason to Buy Dividend-Paying Visa Stock Now

- SanDisk Stock Just Hit New Record Highs With Wall Street

- GLP-1 Sales Continue to Lift Eli Lilly. Does That Make LLY Stock a Buy?

- Western Digital Stock Has More Than Doubled YTD, but Bank of America Still Thinks You Should Buy Ahead of Earnings