Popular semiconductor and infrastructure software solutions provider Broadcom (AVGO) reported its first-quarter results for fiscal 2026 recently, and investors are rewarding a lesser-known stock based on a revelation in the earnings call. Specifically, Broadcom weighed in on the benefits of copper-based interconnects over co-packaged optics.

Broadcom CEO Hock Tan stated that if companies are building large language models (LLMs) and designing their own AI data centers, they need increasingly larger domains or clusters to connect XPUs directly whenever possible. Tan added that direct attach copper is the best way to achieve this.

Shares of active electrical cable (AEC) maker Credo Technology (CRDO) jumped on the news, gaining nearly 12% intraday on March 5. CRDO stock shrugged off fears that businesses would switch to optical connectivity, as Broadcom showed confidence in copper.

With that said, let's look into Credo a bit more deeply.

About Credo Technology Stock

Credo Technology focuses on designing high-speed connectivity solutions that are essential to modern data infrastructure. It develops AECs using copper, digital signal processors, serializer/deserializer intellectual property, retimers, and gearboxes. These products enable efficient data transmission in AI networks, cloud computing, hyperscale environments, and enterprise systems.

The company serves hyperscalers, original equipment manufacturers (OEMs), and optical module makers globally through its semiconductor operations and IP licensing. Credo is based in Grand Cayman, the Cayman Islands, and has a market capitalization of $20.2 billion.

Explosive demand for high-speed copper cables and optical connectivity solutions has fueled revenue growth and strong earnings momentum, leading to CRDO stock’s rapid surge. Over the past 52 weeks, CRDO stock has gained 150%. However, the stock has dropped 24% year-to-date (YTD). Shares had reached an all-time high of $213.80 in December 2025, but they are now down 49% from that level. Hence, the stock's gains have essentially tapered this year.

On a forward-adjusted basis, Credo’s price-to-earnings (P/E) ratio of 52.1 times is higher than the industry average of 21.8 times.

Credo Technology Delivers Record Q3 Revenue Amid AI Surge

Credo reported its Q3 fiscal 2026 results (the quarter ended Jan. 31, 2026) on March 2. Revenue grew by a staggering 201.5% year-over-year (YOY) to $407 million, as the demand for AECs and ICs continued to grow.

Credo also saw its margins expand as the topline skyrocketed. The company’s non-GAAP gross margin grew from 63.8% to 68.6%, while the non-GAAP operating income margin grew from 31.4% to 49.6%. Non-GAAP net income increased from $0.25 per diluted share to $1.07 per diluted share.

The company’s total addressable market has expanded by billions of dollars as Credo has added new offerings, such as ZeroFlap optics and OmniConnect. Credo has also acquired CoMira Solutions, an IP innovator in high-speed connectivity. CoMira’s link-layer, error-correction (ECC), and security IPs align with Credo’s existing scale-out products, helping the business improve them.

For Q4 fiscal 2026, revenue is expected to be in the $425 million to $435 million range. Credo's non-GAAP gross margin is expected to be in the 64% to 66% range, indicating a bit of sequential contraction. This, along with some profit-taking by investors, lead to a roughly 15% intraday decline on March 3.

Wall Street analysts are robustly optimistic about Credo’s future earnings. They expect EPS to climb by 255% YOY to $0.71 for Q4 fiscal 2026. For full-year fiscal 2026, EPS is projected to surge 659% annually to $2.20, followed by 41% growth to $3.10 in fiscal 2027.

What Do Analysts Think About Credo Technology Stock?

Following the company’s Q3 earnings release, CRDO stock has received a handful of positive reaffirmations from Wall Street analysts. Susquehanna maintained a bullish “Positive” rating on Credo but lowered the price target from $230 to $170. Mizuho analyst Vijay Rakesh echoed this sentiment, maintaining an “Outperform” rating on the stock but lowering the price target from $225 to $200.

Rosenblatt analysts are taking a more middle-of-the-road approach, maintaining a “Neutral” rating after the Q3 results and a $125 price target. Despite CRDO stock contracting after earnings, analysts at Needham reiterated their “Buy” rating and maintained a $220 price target, signaling that the underlying trajectory could remain intact. Needham analysts also raised their fiscal 2027 revenue estimate to $2 billion from $1.92 billion, suggesting optimism that the ongoing momentum in AEC deployments will persist if current adoption trends continue.

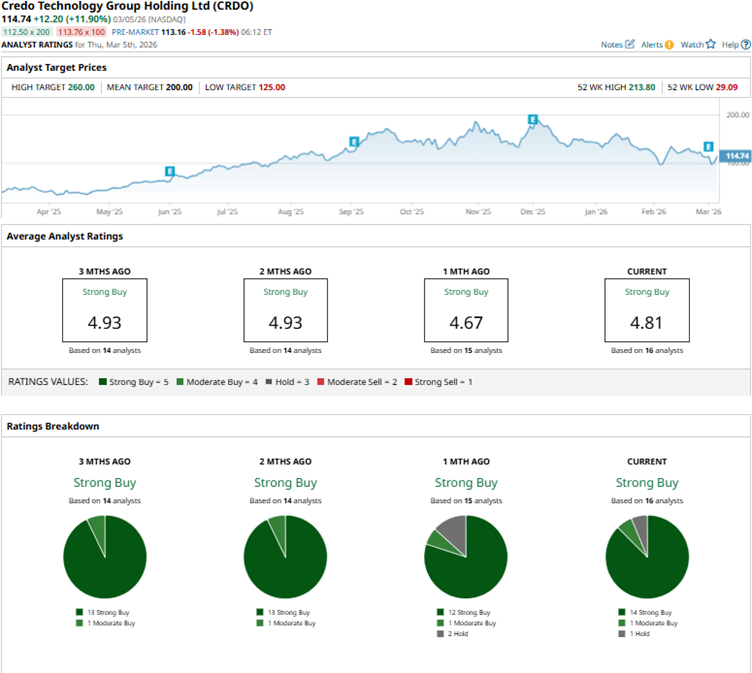

Wall Street analysts have a robustly favorable view of Credo Technology stock, awarding it with a “Strong Buy” rating overall. Of the 16 analysts rating the stock, a majority of 14 analysts rate it a “Strong Buy,” one analyst has a “Moderate Buy,” and one has a “Hold” rating. The consensus price target of $200 represents 82% potential upside from current levels, while the Street-high price target of $260 indicates 136% potential upside.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Defense Stocks Like RTX Corp Look Attractive to Value Investors and OTM Option Plays

- RTX Stock Just Hit New All-Time Highs Amid Iran War. How Much Higher Can It Go?

- Costco Slips Under $1,000 Again. Should You Buy This Dividend Powerhouse?

- ServiceNow Stock May Be Setting Up a Hidden Options Opportunity