Snap (SNAP) was already navigating a tough road back to profitability. Now it has a new problem sitting in Brussels, Belgium. The European Commission has opened formal proceedings to investigate whether Snapchat is meeting its obligations under the Digital Services Act (DSA), a sweeping European Union law designed to hold large platforms accountable for the safety of their users, especially children.

The investigation covers five areas: age verification, protection of minors from grooming and criminal recruitment, default account settings, the spread of information about illegal products, and the platform's handling of illegal content reports. The European Commission suspects Snapchat may be falling short on all five counts, according to a statement from authorities.

For investors, the timing is tricky. Snap just reported its strongest quarterly results in years. But a formal EU probe adds legal and financial risk to the story.

What the EU Investigation Means for Snap Stock

The core of the EU's concern is that Snapchat isn't doing enough to protect young users from harm. Regulators suspect that the platform's reliance on self-declaration — simply asking users their age when they sign up — is not a reliable way to keep underage children off the service or to ensure age-appropriate experiences for teenagers. The European Commission also flagged that a tool to report accounts of users under 13 may not even be accessible within the app.

Beyond age verification, authorities suspect Snapchat exposes minors to adults pretending to be teenagers, fails to prevent the spread of content pointing users toward illegal drugs and age-restricted products like vapes, and uses interface designs that make it hard for users to report harmful content.

The European Commission will now gather evidence through information requests, interviews, and potential on-site inspections. It has the power to issue interim measures, require Snap to make changes, or hand down a non-compliance decision. Fines under the DSA can reach up to 6% of a company's global annual revenue.

On the fourth-quarter 2025 earnings call, Snap CEO Evan Spiegel acknowledged that regulatory risk is real. Management noted that the platform already removed roughly 400,000 accounts after Australia introduced a law requiring users to be at least 16. Spiegel also made a point of distinguishing Snapchat from broader social media criticism, arguing that research shows the platform has a positive impact on well-being, but added that making the case to regulators has been difficult.

Snap Focuses on Fundamentals

Snap is valued at a market capitalization of $6.6 billion, with SNAP stock down 62% from the 52-week high, burning significant investor wealth. However, could the company be on the cusp of a turnaround?

In Q4 2025, Snap reported revenue of $1.72 billion, up 10% year-over-year (YOY). “Other Revenue” subscription sales, a high-margin revenue stream, grew 62% to $232 million while paying subscribers rose 71% to 24 million. Adjusted EBITDA of $358 million represented a margin of 21%, while net income was $45 million. Active advertisers grew 28% YOY. Small-and medium-sized businesses have now driven the majority of advertising revenue growth for six straight quarters. Finally, free cash flow (FCF) for the full year was $437 million. The company also authorized a new $500 million share repurchase program.

The message from management is that Snap is pivoting away from chasing user growth at any cost and toward building a more profitable, diversified business. Gross margins reached 59% in Q4, and the company sees a “clear path” to exceeding 60% in 2026.

Should You Buy, Sell, or Hold SNAP Stock?

The honest answer when it comes to investing in SNAP is that it depends heavily on how the investigation unfolds, and that timeline is uncertain. If regulators move toward a noncompliance decision, the financial hit could be significant. Snap's EU revenue isn't broken out separately, but Europe represents a key monetization market.

Analysts tracking SNAP stock forecast revenue to increase from $5.93 billion in 2025 to $9.12 billion in 2030. In this period, FCF is forecast to grow from $447 million to $1.63 billion. If SNAP stock is priced at 10 times forward FCF, it should surge within the next four years.

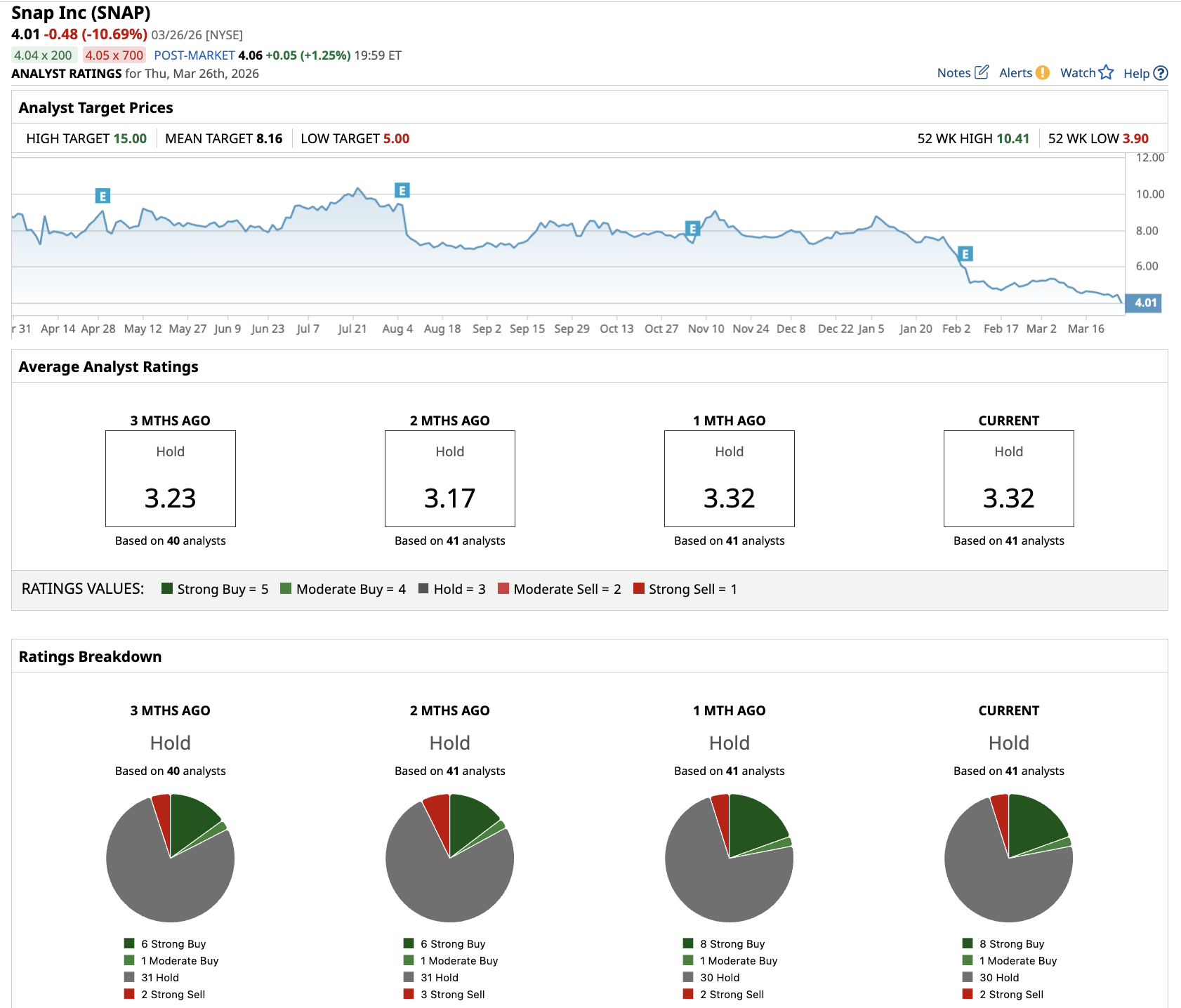

Out of the 41 analysts covering SNAP stock, eight recommend a “Strong Buy,” one recommends a “Moderate Buy” rating, 30 recommend a “Hold” rating, and two recommend a “Strong Sell." The average price target is $8.16, representing 107% potential upside from current levels.

What is clear is that the business itself is in better shape than it has been in years. The company is generating real cash, cutting costs intelligently, and growing its subscriber base quickly. Those are not the characteristics of a company falling apart.

For risk-tolerant investors, the current regulatory cloud may present an entry point. For those who prefer cleaner stories, waiting for more clarity from Brussels may be the smarter move.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.