Amazon.com (AMZN) has long been the everything store, powering online shopping, logistics, and, increasingly, the backbone of the internet through Amazon Web Services (AWS). But in today’s artificial intelligence (AI) era, the cloud edge depends heavily on chips. The ability to design powerful, cost-efficient AI hardware has become a defining advantage, and Amazon has been pushing hard with Amazon Trainium, its in-house accelerators built for training and running large AI models.

Trainium has been gaining serious traction, especially with heavy usage from Anthropic’s Claude models, putting Amazon firmly in the AI infrastructure game. Behind that momentum was Gadi Hutt, a key voice and leader helping steer the chip strategy forward. Now, with Hutt reportedly exiting, it marks the second senior departure from Annapurna Labs, the Israeli semiconductor startup that Amazon acquired in 2015. This follows Rami Sinno leaving for Arm Holdings (ARM). Add in broader AI leadership exits like that of Rohit Prasad, and it starts to feel like a wave of churn amidst a critical time.

With competition heating up and AMZN stock slipping, is this just leadership reshuffling, or something that could start weighing on the stock going forward?

About Amazon Stock

Amazon is one of those companies that’s everywhere, whether one notices it or not. It started off selling books online, and today it’s a tech giant sitting at the center of e-commerce in the U.S, boasting a market capitalization of $2.14 trillion. But that’s just one piece.

Through AWS, it powers a big chunk of the internet, while also expanding into streaming, smart devices, advertising, healthcare, and now AI. From getting packages to the door to running the tech behind businesses, Amazon is deeply woven into everyday life. It’s constantly building, experimenting, and scaling new ideas, shaping the ways people shop, watch, work, and connect in a rapidly evolving digital world.

For a company with the scale of Amazon, the long-term story still looks nothing short of remarkable. The stock has delivered a staggering 10,814% return over the past two decades and 572% over the last ten years. Even in the more recent stretch, AMZN is up 93% over the past three years, showing its ability to keep compounding despite shifts in the market.

But zoom in, and the stock’s journey has not been smooth lately. Over the past 52 weeks, the stock has moved through a volatile phase, peaking at $258.60 in November before sliding nearly 22.5%. While AMZN is only down about 4.3% over the past year, 2026 has started on a weaker note, with shares down 12.9% so far. That shift reflects growing investor caution, especially around Amazon’s aggressive spending and pressure on margins.

The reaction was clear after its Q4 results. The stock fell for six straight sessions as investors digested plans to pour roughly $200 billion into AI, cloud infrastructure, robotics, and data centers, raising concerns about near-term profitability and cash flow.

Technically, the setup is turning cautious for Amazon. The 14-day RSI, which had bounced from oversold levels in February, is slipping again and now sits around 39.82, pointing to weakening momentum. Volume trends are also flashing more red bars, suggesting rising selling pressure.

Meanwhile, the MACD oscillator is flashing a bearish signal, with the MACD line slipping below the blue signal line as both trend downward. The histogram staying in negative territory further reinforces the shift, pointing to fading momentum and suggesting that bullish strength in Amazon stock is weakening in the near term.

Even after the recent pullback, AMZN stock still trades at a premium – priced at around 26.68 times forward adjusted earnings and 2.65 times sales – above sector's averages. But compared to its own historical medians, that’s actually cheaper than usual. For a company dominating cloud, AI, and retail at this scale, the valuation feels less stretched, and maybe even attractive.

A Closer Look at Amazon’s Q4 Report

Amazon wrapped up 2025 with numbers that, at first glance, looked strong. Yet, the market was not fully convinced. In the fourth-quarter report, released on Feb. 5, the company’s net sales jumped 14% year-over-year (YOY) to $213.4 billion, showing that demand across its ecosystem is still holding up. The real engine, though, continues to be AWS, which pulled in $35.6 billion in revenue, up a solid 24% annually – its fastest growth in over a year – driven largely by AI workloads and enterprise demand rushing into the cloud.

Also, advertising did its part, climbing 22% YOY to $21.3 billion, reinforcing how Amazon is monetizing traffic beyond just retail. Meanwhile, the company posted $1.95 per-share earnings, slightly above last year’s $1.86 but just shy of what Wall Street was expecting. That small miss, paired with what came next, was enough to rattle sentiment. The stock slid about 5.6% the following day, as investors started focusing less on what Amazon delivered and more on what it plans to spend.

For fiscal 2025, Amazon’s net sales rose about 12% YOY to $716.9 billion, keeping its growth story intact. But under the surface, free cash flow took a noticeable hit, falling to around $11.2 billion. The reason was Amazon’s heavy spending, doubling down on AI infrastructure, data centers, custom chips, robotics, and even satellite networks.

Looking ahead, management made it clear that this is not slowing down. Capital expenditures for 2026 are expected to reach $200 billion, a massive step-up that signals Amazon is all-in on owning the next phase of AI and cloud computing. At the same time, that level of investment puts pressure on near-term margins and cash flow, something the market is clearly watching closely.

For the first quarter of fiscal 2026, management guided revenue between $173.5 billion and $178.5 billion, pointing to 11% to 15% annual growth.

Wall Street analysts tracking Amazon project its revenue for Q1 to be around $177.07 billion, with EPS expected to rise 6.3% YOY to $1.69. For fiscal 2026, EPS is anticipated to be $7.78, indicating a 8.5% YOY surge, before rising by another 19.7% annually to $9.31 in fiscal 2027.

What Do Analysts Expect for Amazon Stock?

Recently, Tigress Financial lifted its price target on AMZN to $315 from $305, keeping a “Buy” rating, pointing to growing AI strength across AWS and retail, along with strong high-margin businesses steadily boosting cash flow.

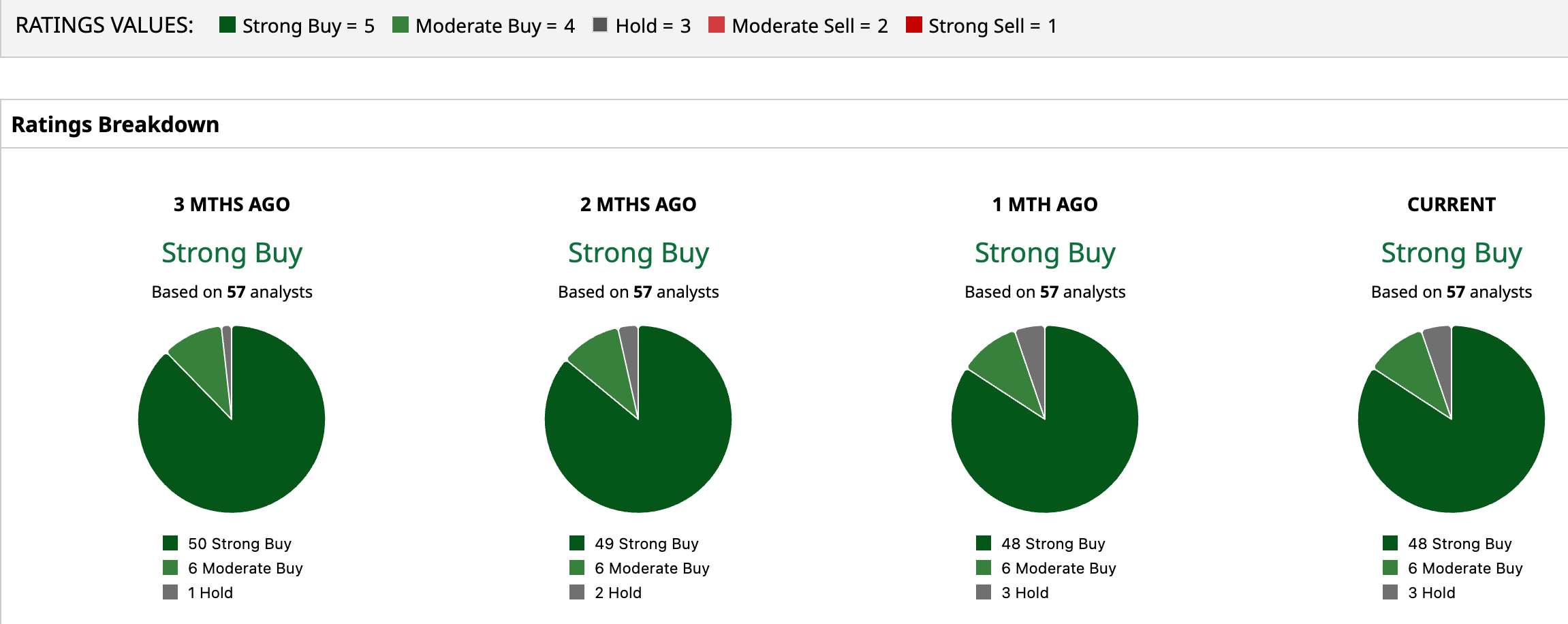

Analysts monitoring AMZN are bullish, with consensus leaning heavily toward a “Strong Buy.” Out of 57 analysts, 48 advise a “Strong Buy,” six recommend a “Moderate Buy,” and three are cautious with a “Hold” rating.

The average price target of $285.82 suggests a 43% upside potential from here. Meanwhile, Loop Capital’s Street-high target of $360 suggests AMZN stock could rise as much as 80%.

Final Thoughts on AMZN Stock

If we look at the bigger picture, Gadi Hutt’s exit carries weight. As director of product and customer engineering at Annapurna Labs, he was deeply involved in shaping Amazon’s competitive custom AI chip strategy. His departure, coming soon after Rami Sinno’s exit, does raise a red flag, especially since it is happening within the team closest to the technology. So, of course, when key builders start stepping away, questions naturally follow.

But on the other hand, it is not entirely one-sided. Amazon is still pushing hard on AI, Trainium adoption is growing, and analysts are upbeat on AMZN’s growth potential. Still, with the stock reacting to Hutt’s exit news and leadership churn picking up, this is one of those moments investors may want to watch a little more closely.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Meta Platforms Just Made Entergy a Top Stock to Buy... and It Pays a 2.49% Dividend

- Micron Stock Cools Off — Is MU Now Too Cheap to Ignore?

- The Strait of Hormuz Is Causing Issues for Scotts Miracle-Gro. How Should You Play the High-Yield Dividend Stock Here?

- Fannie Mae Is Now Accepting Crypto-Backed Mortgages. Does That Make FNMA Stock a Buy?