The Campbell's Company (CPB), headquartered in Camden, New Jersey, manufactures and markets branded convenience food and beverage products. Valued at $8.6 billion by market cap, the company's core divisions include soups and sauces, biscuits and confectionery, and foodservice. It sells its products through retail food chains, mass discounters and merchandisers, club stores, convenience stores, drug stores, and dollar stores.

Shares of this leading packaged food manufacturer have underperformed the broader market considerably over the past year. CPB has declined 23% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 12.2%. However, in 2026, CPB’s stock rose 3%, surpassing the SPX’s marginal dip on a YTD basis.

Narrowing the focus, CPB’s underperformance is also apparent compared to the First Trust Nasdaq Food & Beverage ETF (FTXG). The exchange-traded fund has gained about 5.6% over the past year. Moreover, the ETF’s 10.2% gains on a YTD basis outshine the stock’s single-digit returns over the same time frame.

CPB faced challenges, with sales decline driven by shifting consumer habits and cost pressures. Despite stable market share for core brands, tariffs, inflation, and higher input costs impacted margins.

On Dec. 9, 2025, CPB shares closed down more than 5% after reporting its Q1 results. Its adjusted EPS of $0.77 exceeded Wall Street expectations of $0.73. The company’s revenue was $2.68 billion, exceeding Wall Street forecasts of $2.66 billion. CPB expects full-year adjusted EPS in the range of $2.40 to $2.55.

For the current fiscal year, ending in July, analysts expect CPB’s EPS to decline 18.2% to $2.43 on a diluted basis. The company’s earnings surprise history is impressive. It beat the consensus estimate in each of the last four quarters.

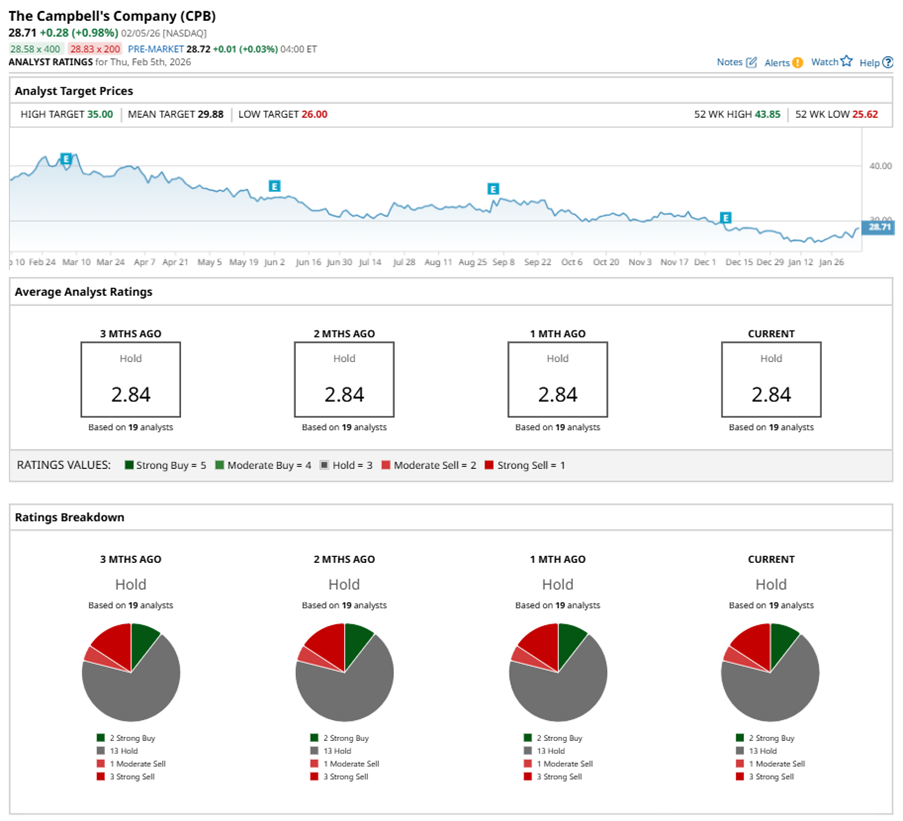

Among the 19 analysts covering CPB stock, the consensus is a “Hold.” That’s based on two “Strong Buy” ratings, 13 “Holds,” one “Moderate Sell,” and three “Strong Sells.”

The configuration has been consistent over the past three months.

On Jan. 21, Bernstein analyst Alexia Burland Howard maintained a “Buy” rating on CPB and set a price target of $33, implying a potential upside of 14.9% from current levels.

The mean price target of $29.88 represents a 4.1% premium to CPB’s current price levels. The Street-high price target of $35 suggests an upside potential of 21.9%.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart