Enabling continuous vehicle performance through over-the-air updates, cybersecurity frameworks, and software-defined automotive architectures.

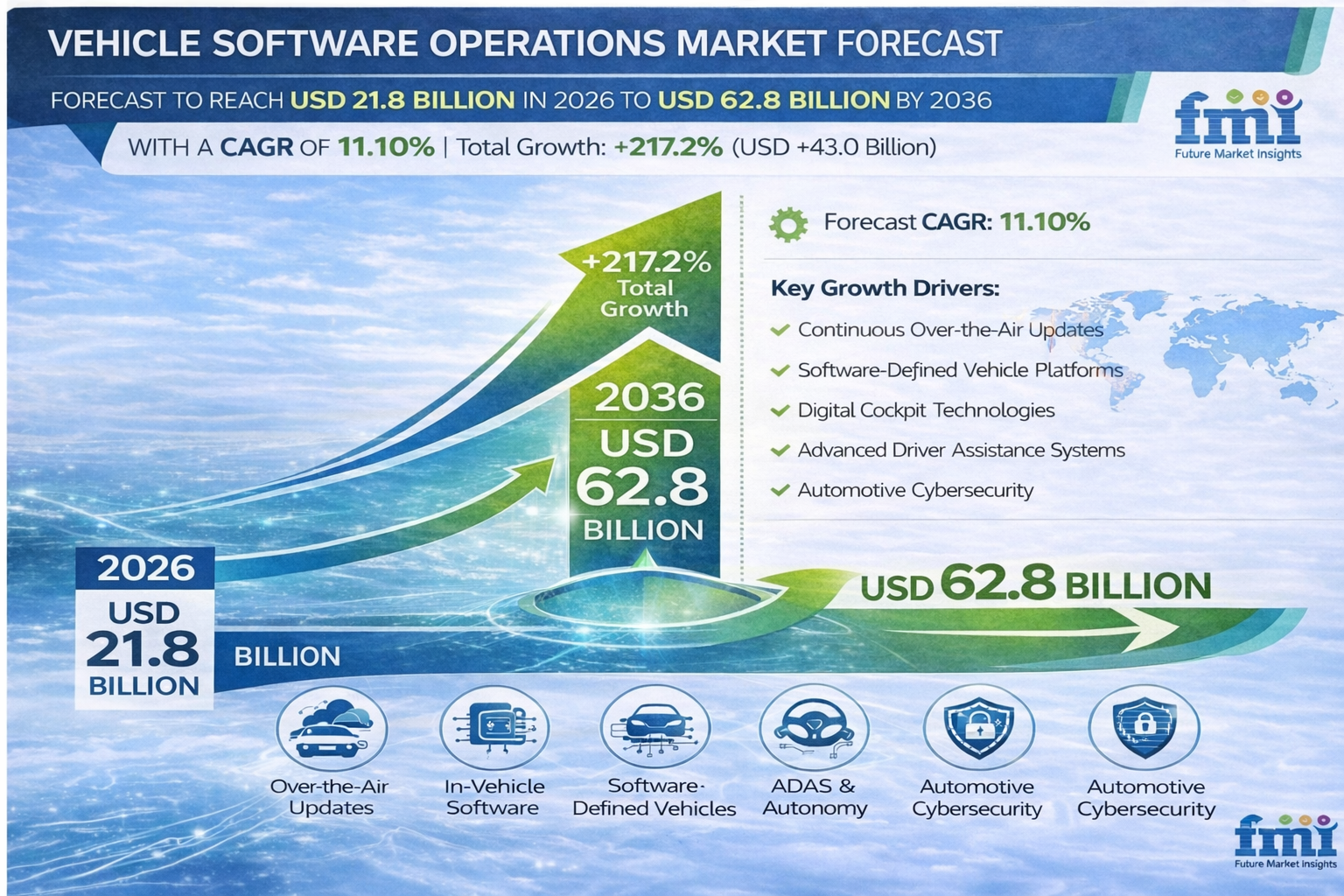

NEWARK, DELAWARE / ACCESS Newswire / March 9, 2026 / The global vehicle software operations market is entering a transformative growth phase as the automotive industry rapidly transitions toward software-defined vehicle architectures. Valued at USD 19.8 billion in 2025, the market is projected to grow to USD 62.8 billion by 2036, expanding at a CAGR of 11.10% over the forecast period.

This expansion reflects a fundamental shift in how vehicles are developed, deployed, and maintained. Automakers are moving away from static software installations during vehicle assembly and instead adopting continuous lifecycle management platforms capable of delivering updates, security patches, and feature upgrades throughout a vehicle's operational life.

As centralized compute architectures replace distributed control systems, vehicle manufacturers increasingly rely on enterprise-grade development pipelines, cybersecurity frameworks, and over-the-air deployment platforms to manage increasingly complex digital ecosystems.

Get Access of Report Sample:

https://www.futuremarketinsights.com/reports/sample/rep-gb-32193

Market Value Analysis: Software-Defined Vehicles Driving Long-Term Growth

Between 2025 and 2030, the vehicle software operations market is expected to grow from USD 19.8 billion to approximately USD 35.6 billion, representing a significant portion of the decade's total growth. This phase will be driven by accelerating adoption of connected vehicle platforms, advanced driver-assistance systems (ADAS), and digital cockpit technologies.

The second phase of expansion, from 2030 to 2036, will push the market from USD 35.6 billion to USD 62.8 billion, supported by widespread deployment of software-defined vehicle platforms, autonomous driving capabilities, and subscription-based vehicle features.

During this period, automakers will increasingly treat vehicles as updatable digital platforms, similar to smartphones, enabling continuous feature deployment without requiring physical recalls or dealer visits.

Technology Evolution: From Static Firmware to Continuous Vehicle Software Operations

The automotive industry is rapidly transitioning from traditional firmware-based vehicle architectures toward dynamic software operations ecosystems.

Modern vehicle software operations frameworks incorporate:

• Continuous integration and delivery pipelines for automotive code development

• Over-the-air (OTA) update platforms enabling remote deployment of software patches

• Automotive-grade operating systems and hypervisors supporting mixed-criticality workloads

• Cloud-to-vehicle telemetry platforms enabling fleet-wide diagnostics

• Containerized application environments isolating infotainment and safety-critical functions

These platforms allow automakers to deploy new functionality long after the vehicle leaves the production line, unlocking recurring revenue streams through digital services and feature subscriptions.

An industry analyst notes:

"The automotive industry is shifting toward software-defined vehicles where digital capability becomes the primary differentiator. Continuous software operations now determine how quickly manufacturers can deploy new features, resolve security vulnerabilities, and monetize connected services."

Over-the-Air Updates Reshaping Vehicle Development Cycles

Continuous software deployment is becoming central to vehicle development strategies. Automakers increasingly rely on OTA update infrastructure to maintain vehicle performance, security, and functionality throughout the product lifecycle.

OTA deployment capabilities allow manufacturers to:

• Deploy security patches across millions of vehicles simultaneously

• Introduce new infotainment and navigation features

• Upgrade ADAS algorithms and autonomy capabilities

• Deliver subscription-based digital services

These capabilities reduce the need for physical service visits while significantly lowering recall costs associated with software defects.

Manufacturers now treat update capability as a core product feature, integrating OTA verification directly into factory assembly lines to ensure vehicles can securely receive updates before leaving production facilities.

Segment Spotlight

Application Software Leads Software Type Segment (47%)

Application software accounts for approximately 47% of the market share, driven by the rapid expansion of digital cockpit interfaces and in-vehicle entertainment systems. Automakers are investing heavily in customizable user interfaces, voice assistants, and app ecosystems integrated directly into vehicle dashboards.

Embedded and Onboard Systems Dominate Deployment (70%)

Embedded and onboard deployments hold around 70% of the market share, reflecting the critical need for localized processing in safety-sensitive applications such as braking systems, steering controls, and ADAS functionality.

These onboard platforms process massive volumes of sensor data in real time, ensuring vehicles can operate safely even without continuous internet connectivity.

Regional Insights: Key Growth Markets

Country |

CAGR (2026-2036) |

Key Growth Drivers |

|---|---|---|

India |

14.0% |

Expansion of global automotive software development hubs and electric vehicle platforms |

China |

13.0% |

Massive EV production and rapid adoption of connected vehicle ecosystems |

United States |

11.0% |

Over-the-air feature monetization and advanced autonomy development |

South Korea |

10.0% |

Digital cockpit innovation and rapid infotainment technology cycles |

Germany |

10.0% |

Premium automotive manufacturing and stringent safety validation standards |

Asia-Pacific is expected to emerge as the fastest-growing region, driven by rising electric vehicle production, strong domestic automaker ecosystems, and aggressive integration of connected vehicle features.

Cybersecurity and Compliance Become Core Industry Priorities

As vehicle software complexity grows, cybersecurity and regulatory compliance have become critical priorities for automotive manufacturers.

Governments and safety regulators are introducing stringent cybersecurity mandates requiring manufacturers to maintain the ability to patch vulnerabilities throughout the vehicle lifecycle.

Key compliance trends include:

• Mandatory cybersecurity management systems for connected vehicles

• Continuous vulnerability monitoring across fleet deployments

• Strict validation of software supply chains and update mechanisms

• Integration of secure boot environments and encrypted OTA platforms

These regulatory requirements are accelerating investment in automotive DevOps platforms and software lifecycle management tools.

Competitive Landscape: Software Ecosystems Define Market Leadership

The vehicle software operations ecosystem is becoming increasingly competitive as technology providers, semiconductor companies, and automotive suppliers race to build end-to-end software platforms.

Leading market participants include:

• Bosch

• Continental

• Aptiv

• HARMAN (Samsung)

• NVIDIA

• Qualcomm

• Google (Android Automotive)

These companies are investing heavily in centralized vehicle compute platforms, AI-driven autonomy software, digital cockpit systems, and secure OTA update infrastructures.

Strategic collaborations between automakers, chip manufacturers, and software firms are rapidly reshaping the competitive landscape.

Future Outlook: Software-Defined Vehicles Redefine Automotive Innovation

Looking toward 2036, the vehicle software operations market will play a central role in enabling the next generation of mobility technologies.

Key trends expected to shape the market include:

• Full transition toward software-defined vehicle architectures

• Expansion of subscription-based digital vehicle features

• Integration of AI-powered autonomous driving algorithms

• Growth in cloud-connected fleet management systems

• Development of real-time vehicle cybersecurity monitoring platforms

As vehicles evolve into continuously updatable digital systems, software operations platforms will become the backbone of automotive innovation, enabling manufacturers to deliver safer, smarter, and more personalized mobility experiences.

With connected vehicles, autonomous technologies, and digital cockpit ecosystems gaining momentum worldwide, the vehicle software operations market is poised for sustained expansion over the next decade, fundamentally transforming how vehicles are designed, maintained, and experienced.

For an in-depth analysis of evolving formulation trends and to access the complete strategic outlook for the Vehicle Software Operations Market through 2036, visit the official report page at: https://www.futuremarketinsights.com/reports/vehicle-software-operations-market

Brows More Automotive Industry Reports:

Self balancing Scooter Market - https://www.futuremarketinsights.com/reports/self-balancing-scooter-market

In-Vehicle Intrusion Detection & Forensics Platforms for Connected Fleets Market - https://www.futuremarketinsights.com/reports/in-vehicle-intrusion-detection-forensics-platforms-for-connected-fleets-market

Off-Highway Vehicle Telematics Market - https://www.futuremarketinsights.com/reports/global-off-highway-vehicle-telematics-market

Automotive Tappet Market - https://www.futuremarketinsights.com/reports/automotive-tappet-market

Sailplane Market - https://www.futuremarketinsights.com/reports/sailplane-market

About Future Market Insights (FMI)

Future Market Insights (FMI) is a leading provider of market intelligence and consulting services, serving clients in over 150 countries. Headquartered in Delaware, USA, with a global delivery center in India and offices in the UK and UAE, FMI delivers actionable insights to businesses across industries including automotive, technology, consumer products, manufacturing, energy, and chemicals.

An ESOMAR-certified research organization, FMI provides custom and syndicated market reports and consulting services, supporting both Fortune 1,000 companies and SMEs. Its team of 300+ experienced analysts ensures credible, data-driven insights to help clients navigate global markets and identify growth opportunities.

For Press & Corporate Inquiries

Rahul Singh

AVP - Marketing and Growth Strategy

Future Market Insights, Inc.

+91 8600020075

For Sales - sales@futuremarketinsights.com

For Media - Rahul.singh@futuremarketinsights.com

For web - https://www.futuremarketinsights.com/

SOURCE: Future Market Insights, Inc.

View the original press release on ACCESS Newswire