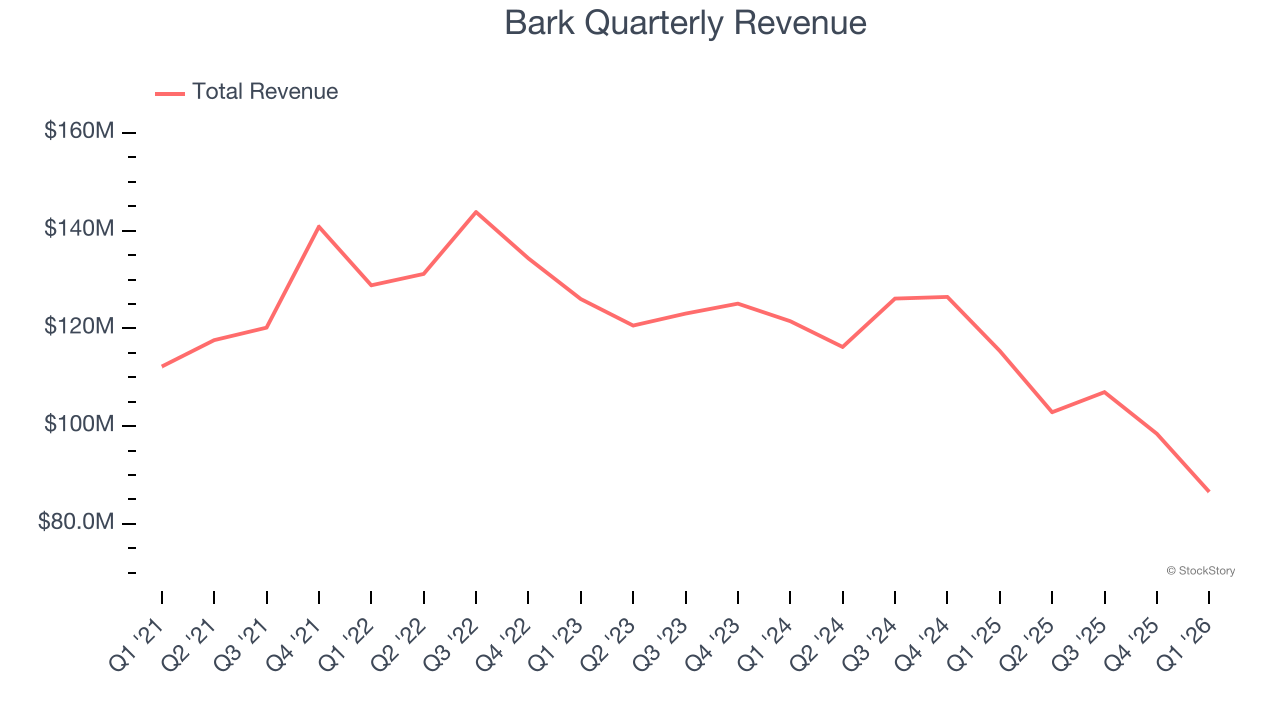

Pet products provider Bark (NYSE: BARK) missed Wall Street’s revenue expectations in Q1 CY2026, with sales falling 25% year on year to $86.57 million. Next quarter’s revenue guidance of $78 million underwhelmed, coming in 25.7% below analysts’ estimates. Its non-GAAP profit of $0.07 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Bark? Find out by accessing our full research report, it’s free.

Bark (BARK) Q1 CY2026 Highlights:

- Revenue: $86.57 million vs analyst estimates of $95.2 million (25% year-on-year decline, 9.1% miss)

- Adjusted EPS: $0.07 vs analyst estimates of -$0.40 (significant beat)

- Adjusted EBITDA: $3.17 million vs analyst estimates of $814,000 (3.7% margin, significant beat)

- Revenue Guidance for Q2 CY2026 is $78 million at the midpoint, below analyst estimates of $105 million

- EBITDA guidance for the upcoming financial year 2027 is $8.5 million at the midpoint, above analyst estimates of $4.06 million

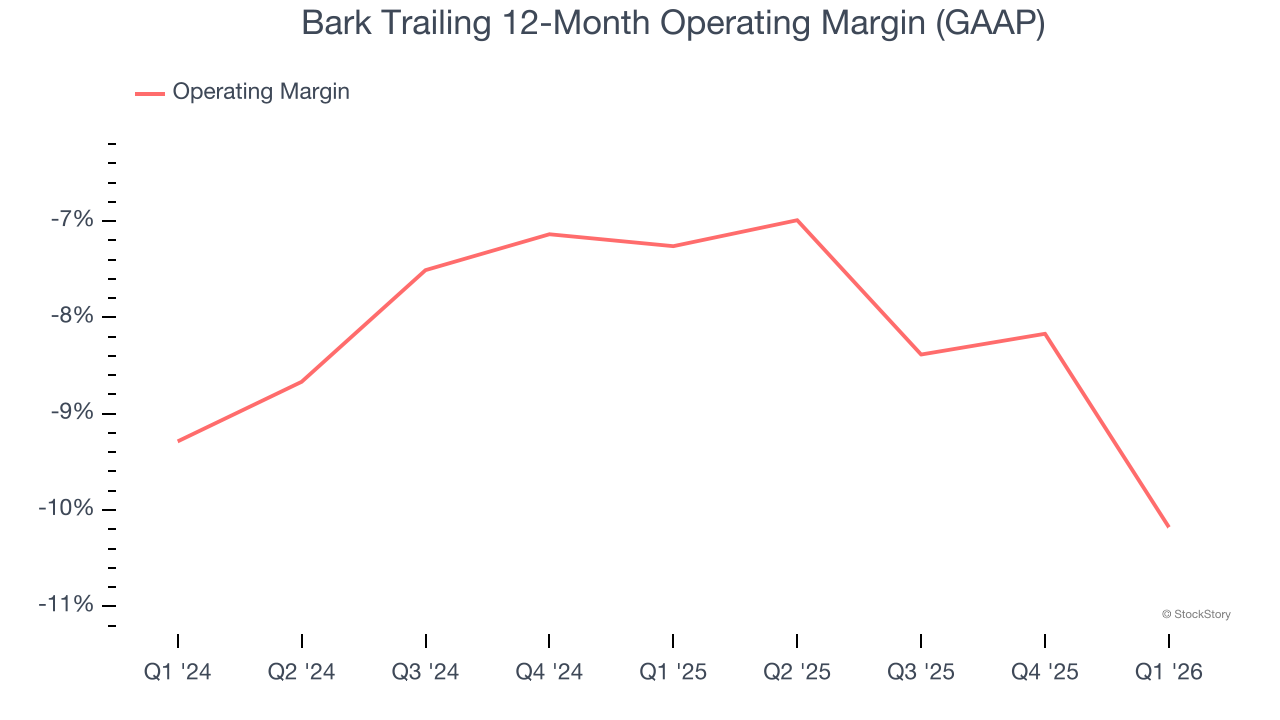

- Operating Margin: -14.1%, down from -5.7% in the same quarter last year

- Free Cash Flow was -$2.06 million compared to -$11.99 million in the same quarter last year

- Market Capitalization: $82.61 million

Company Overview

Making a name for itself with the BarkBox, Bark (NYSE: BARK) specializes in subscription-based, personalized pet products.

Revenue Growth

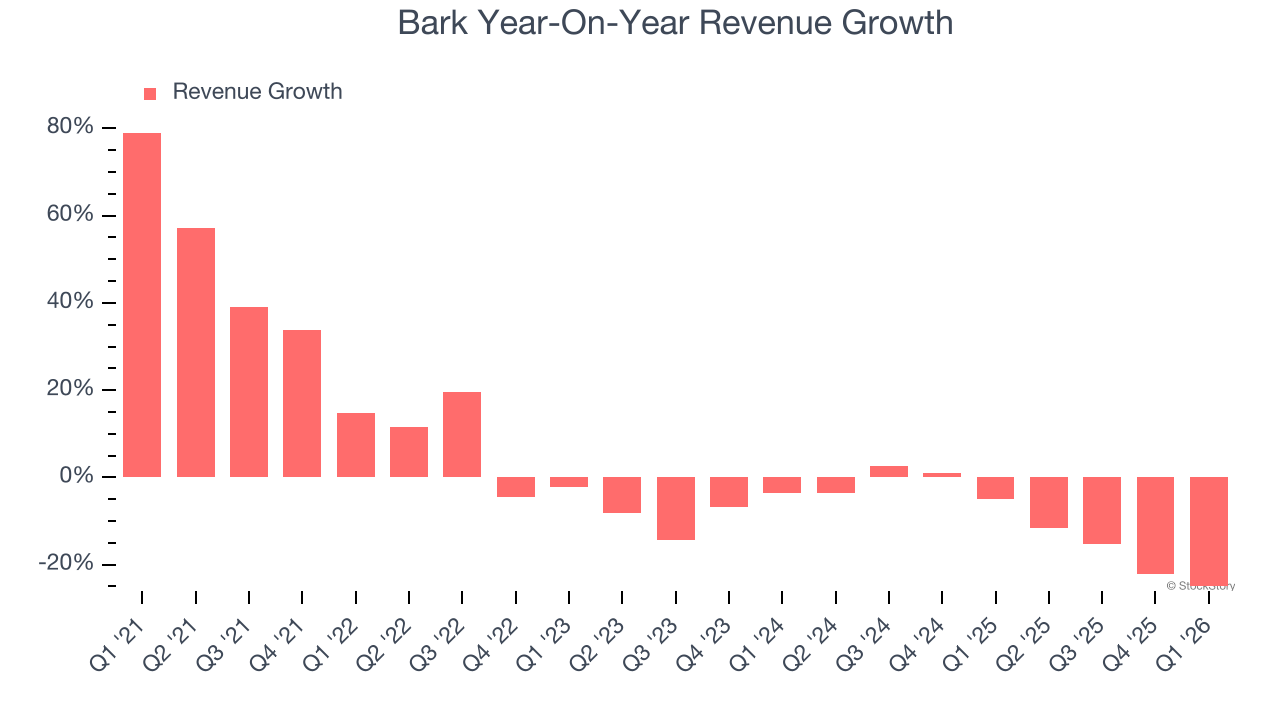

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, Bark struggled to consistently increase demand as its $394.8 million of sales for the trailing 12 months was close to its revenue five years ago. This wasn’t a great result and is a sign of poor business quality.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Bark’s recent performance shows its demand remained suppressed as its revenue has declined by 10.3% annually over the last two years.

This quarter, Bark missed Wall Street’s estimates and reported a rather uninspiring 25% year-on-year revenue decline, generating $86.57 million of revenue. Company management is currently guiding for a 24.2% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 5.7% over the next 12 months. While this projection suggests its newer products and services will catalyze better top-line performance, it is still below average for the sector.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Bark’s operating margin has been trending down over the last 12 months and averaged negative 8.6% over the last two years. Unprofitable consumer discretionary companies with falling margins deserve extra scrutiny because they’re spending loads of money to stay relevant, an unsustainable practice.

Bark’s operating margin was negative 14.1% this quarter. The company’s consistent lack of profits raises a flag.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth — for example, a company could inflate its sales through excessive spending on advertising and promotions.

Although Bark’s full-year earnings are still negative, it reduced its losses and improved its EPS by 36.2% annually over the last four years. The next few quarters will be critical for assessing its long-term profitability.

In Q1, Bark reported adjusted EPS of $0.07, down from $0.20 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Bark to improve its earnings losses. Analysts forecast its full-year EPS will improve from negative $1.53 to negative $1.

Key Takeaways from Bark’s Q1 Results

It was good to see Bark beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. On the other hand, its full-year revenue guidance missed and its revenue guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock remained flat at $10.08 immediately following the results.

Big picture, is Bark a buy here and now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).