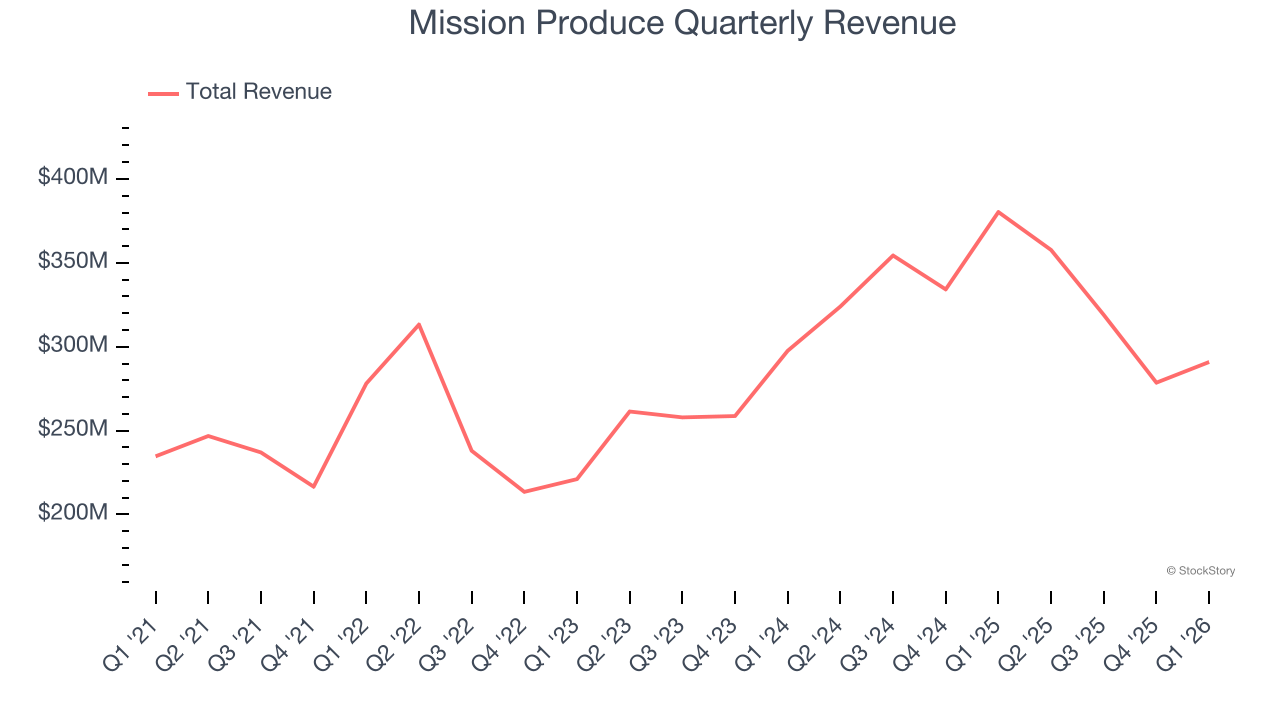

Avocado company Mission Produce (NASDAQ: AVO) reported Q1 CY2026 results beating Wall Street’s revenue expectations, but sales fell by 23.5% year on year to $290.9 million. Its non-GAAP profit of $0.01 per share was 81.2% below analysts’ consensus estimates.

Is now the time to buy Mission Produce? Find out by accessing our full research report, it’s free.

Mission Produce (AVO) Q1 CY2026 Highlights:

- Revenue: $290.9 million vs analyst estimates of $256.3 million (23.5% year-on-year decline, 13.5% beat)

- Adjusted EPS: $0.01 vs analyst expectations of $0.05 (81.2% miss)

- Adjusted EBITDA: $7.1 million vs analyst estimates of $14.73 million (2.4% margin, 51.8% miss)

- Operating Margin: -2.4%, down from 1.9% in the same quarter last year

- Free Cash Flow was -$29 million compared to -$25 million in the same quarter last year

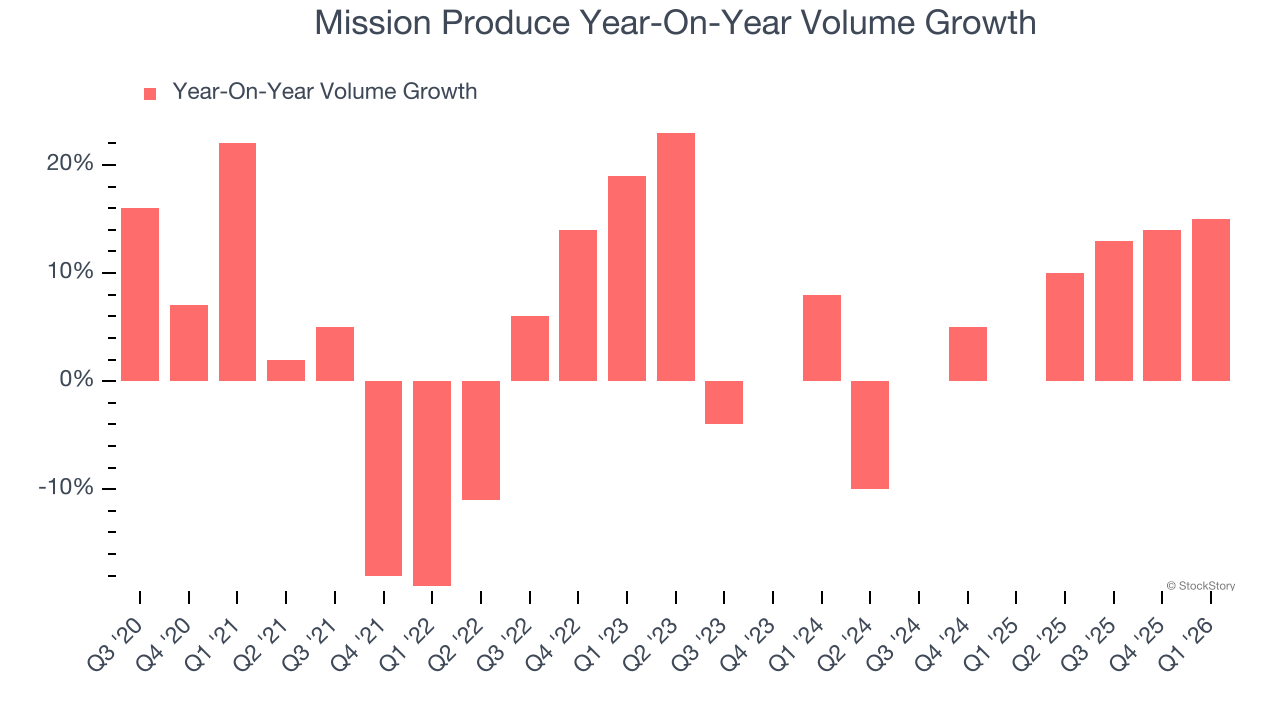

- Sales Volumes rose 15% year on year (0% in the same quarter last year)

- Market Capitalization: $724 million

John Pawlowski, President and CEO of Mission, stated, “This quarter was shaped by high volumes, low prices, strong execution by our sales and operations teams, and unfortunately, margin compression concentrated in April. Despite the low-price environment, we maintained manageable margins through most of the quarter until the Mexican supply of core fruit sizes fell out of line with customer demand in the final weeks. Delays in the California and Peru harvests increased sourcing costs to fill the gaps and pressured margins. Importantly, supply conditions have improved, pricing and margins are recovering, and we expect to deliver solid performance in the back half of the year.

Company Overview

Founded in 1983 in California, Mission Produce (NASDAQ: AVO) grows, packages, and distributes avocados.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $1.25 billion in revenue over the past 12 months, Mission Produce is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers. On the bright side, it can grow faster because it has a longer list of untapped store chains to sell into.

As you can see below, Mission Produce’s sales grew at a decent 8.1% compounded annual growth rate over the last three years as consumers bought more of its products.

This quarter, Mission Produce’s revenue fell by 23.5% year on year to $290.9 million but beat Wall Street’s estimates by 13.5%.

Looking ahead, sell-side analysts expect revenue to decline by 12.1% over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and suggests its products will face some demand challenges.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Volume Growth

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

Mission Produce’s average quarterly volume growth was a robust 5.9% over the last two years. This is good because meaningful volume growth is hard to come by in the stable consumer staples sector.

In Mission Produce’s Q1 2026, sales volumes jumped 15% year on year. This result was an acceleration from its historical levels, certainly a positive signal.

Key Takeaways from Mission Produce’s Q1 Results

We were impressed by how significantly Mission Produce blew past analysts’ revenue expectations this quarter. On the other hand, its adjusted operating income missed and its EBITDA fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 7.7% to $9.32 immediately following the results.

Mission Produce didn’t show it’s best hand this quarter, but does that create an opportunity to buy the stock right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).