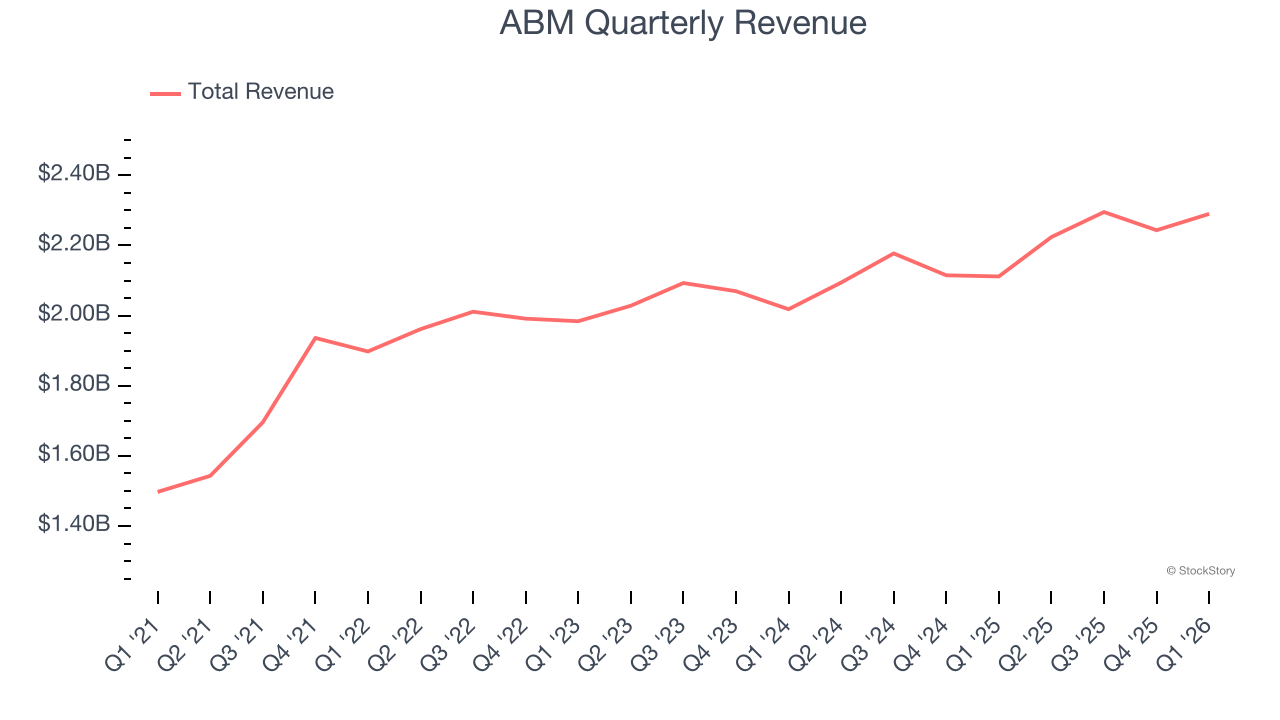

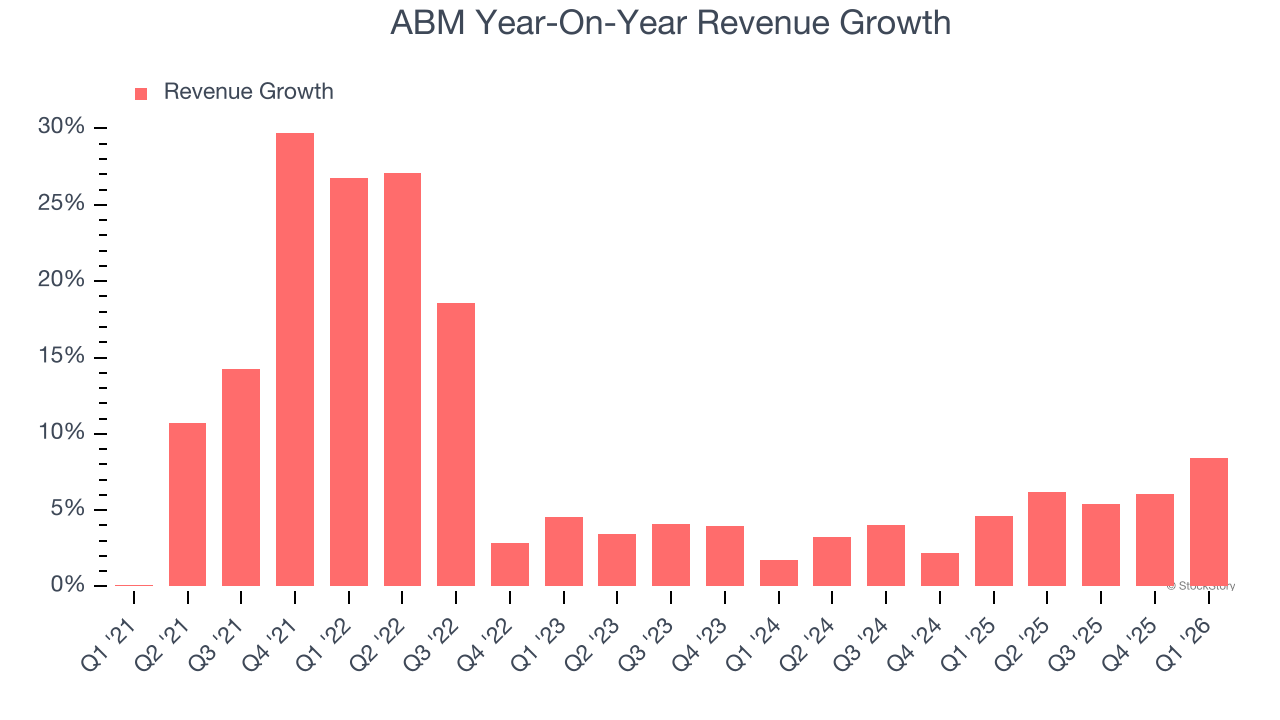

Facility services provider ABM Industries (NYSE: ABM) announced better-than-expected revenue in Q1 CY2026, with sales up 8.4% year on year to $2.29 billion. Its non-GAAP profit of $0.90 per share was 2.4% above analysts’ consensus estimates.

Is now the time to buy ABM? Find out by accessing our full research report, it’s free.

ABM (ABM) Q1 CY2026 Highlights:

- Revenue: $2.29 billion vs analyst estimates of $2.22 billion (8.4% year-on-year growth, 3.1% beat)

- Adjusted EPS: $0.90 vs analyst estimates of $0.88 (2.4% beat)

- Adjusted EBITDA: $131.7 million vs analyst estimates of $130.9 million (5.8% margin, 0.6% beat)

- Management reiterated its full-year Adjusted EPS guidance of $4 at the midpoint

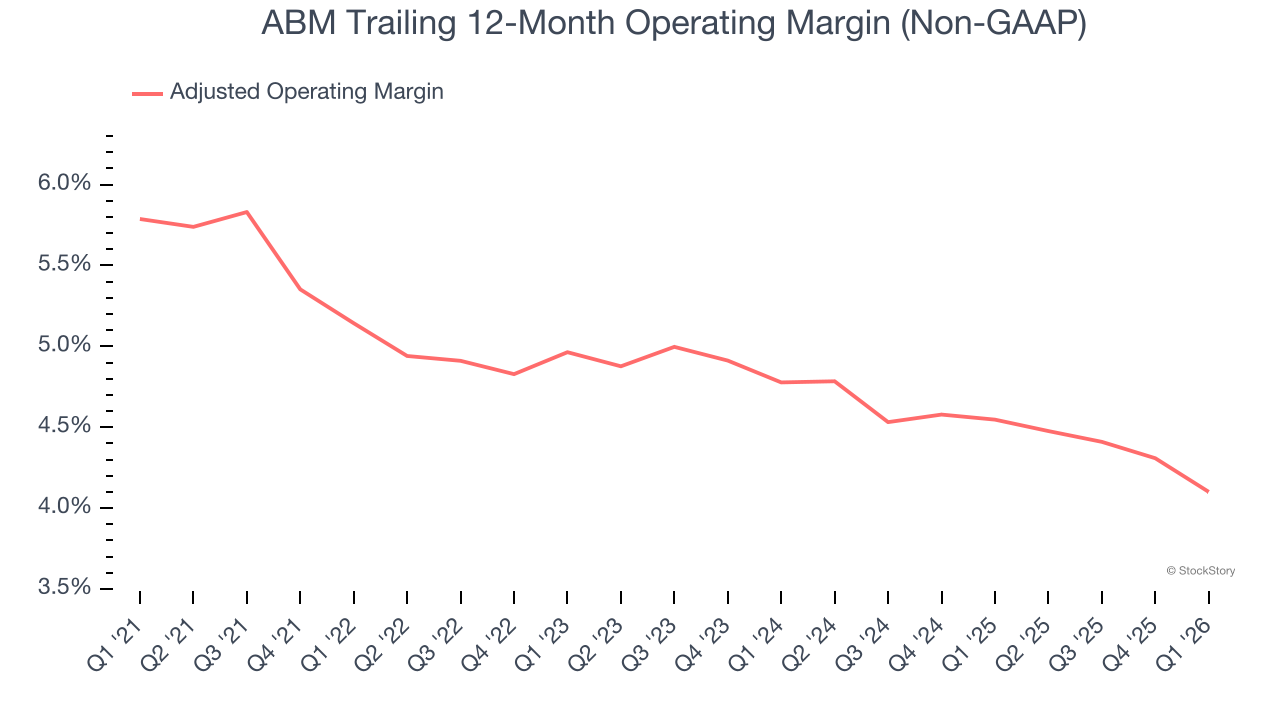

- Operating Margin: 3.8%, in line with the same quarter last year

- Free Cash Flow Margin: 1%, similar to the same quarter last year

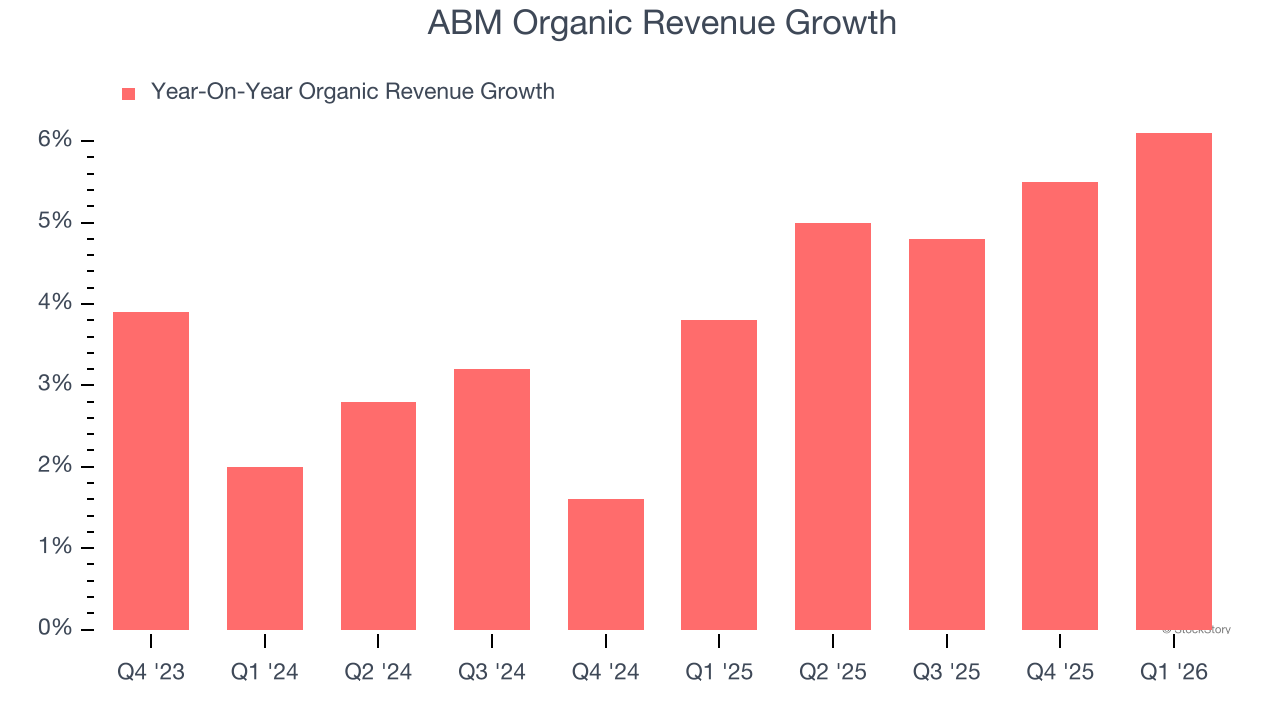

- Organic Revenue rose 6.1% year on year (beat)

- Market Capitalization: $2.33 billion

"Our second quarter performance was highlighted by organic revenue growth of 6.1% and record first half new sales bookings of $1.2 billion," said Scott Salmirs, President and Chief Executive Officer.

Company Overview

With roots dating back to 1909 as a window washing company, ABM Industries (NYSE: ABM) provides integrated facility management, infrastructure, and mobility solutions across various sectors including commercial, manufacturing, education, and aviation.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $9.05 billion in revenue over the past 12 months, ABM is one of the larger companies in the business services industry and benefits from a well-known brand that influences purchasing decisions.

As you can see below, ABM’s sales grew at an impressive 9.1% compounded annual growth rate over the last five years. This shows it had high demand, a useful starting point for our analysis.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. ABM’s annualized revenue growth of 5% over the last two years is below its five-year trend, but we still think the results were respectable.

We can better understand the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, ABM’s organic revenue averaged 4.1% year-on-year growth. Because this number aligns with its two-year revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, ABM reported year-on-year revenue growth of 8.4%, and its $2.29 billion of revenue exceeded Wall Street’s estimates by 3.1%.

Looking ahead, sell-side analysts expect revenue to grow 3.2% over the next 12 months, a slight deceleration versus the last two years. This projection doesn’t excite us and implies its products and services will face some demand challenges.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Adjusted Operating Margin

ABM was profitable over the last five years but held back by its large cost base. Its average adjusted operating margin of 4.7% was weak for a business services business.

Analyzing the trend in its profitability, ABM’s adjusted operating margin decreased by 1 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. ABM’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, ABM generated an adjusted operating margin profit margin of 3.8%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

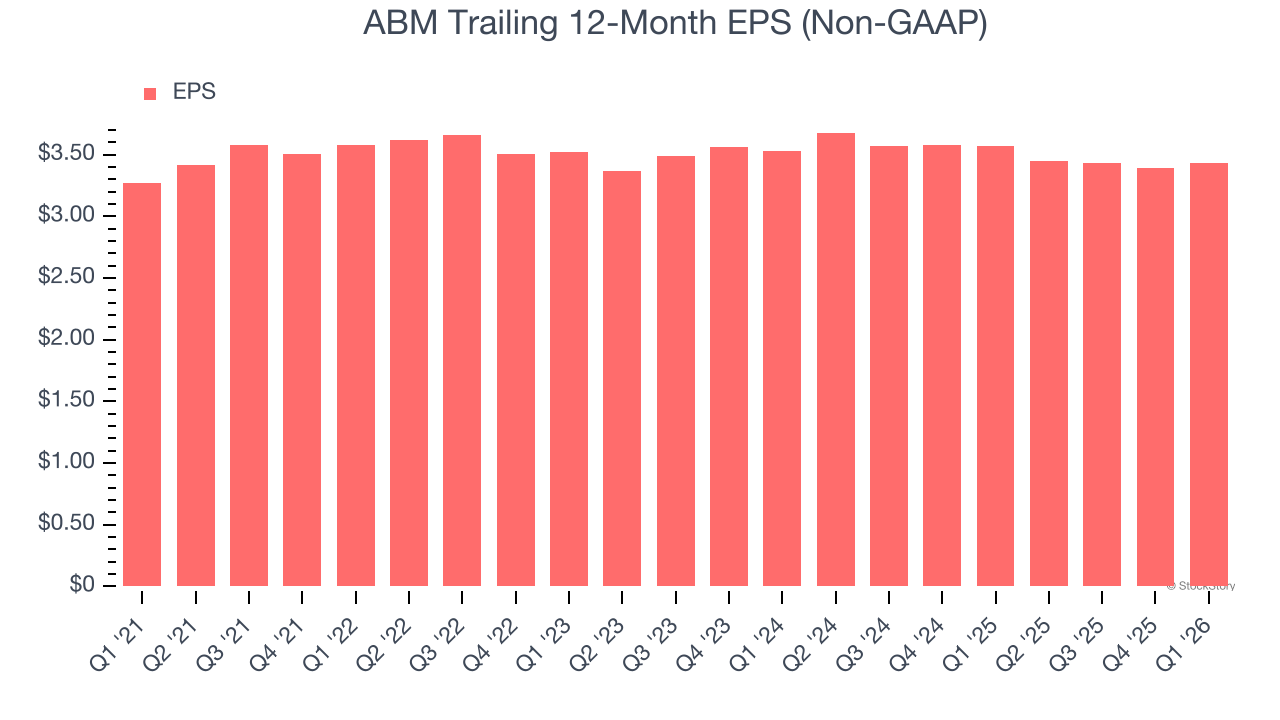

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

ABM’s flat EPS over the last five years was below its 9.1% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

We can take a deeper look into ABM’s earnings to better understand the drivers of its performance. As we mentioned earlier, ABM’s adjusted operating margin was flat this quarter but declined by 1 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For ABM, its two-year annual EPS declines of 1.4% show its recent history was to blame for its underperformance over the last five years. These results were bad no matter how you slice the data.

In Q1, ABM reported adjusted EPS of $0.90, up from $0.86 in the same quarter last year. This print beat analysts’ estimates by 2.4%. Over the next 12 months, Wall Street expects ABM’s full-year EPS to grow 21.9% from $3.43 to $4.18.

Key Takeaways from ABM’s Q1 Results

We enjoyed seeing ABM beat analysts’ organic revenue expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. Overall, we think this was a solid quarter with some key areas of upside. The stock traded up 5.9% to $42.24 immediately after reporting.

Sure, ABM had a solid quarter, but if we look at the bigger picture, is this stock a buy? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).