Over the last six months, CSW’s shares have sunk to $270.70, producing a disappointing 11.4% loss - a stark contrast to the S&P 500’s 10.9% gain. This may have investors wondering how to approach the situation.

Following the pullback, is now an opportune time to buy CSW? Find out in our full research report, it’s free.

Why Are We Positive on CSW?

With over two centuries of combined operations manufacturing and supplying, CSW (NYSE: CSW) offers special chemicals, coatings, sealants, and lubricants for various industries.

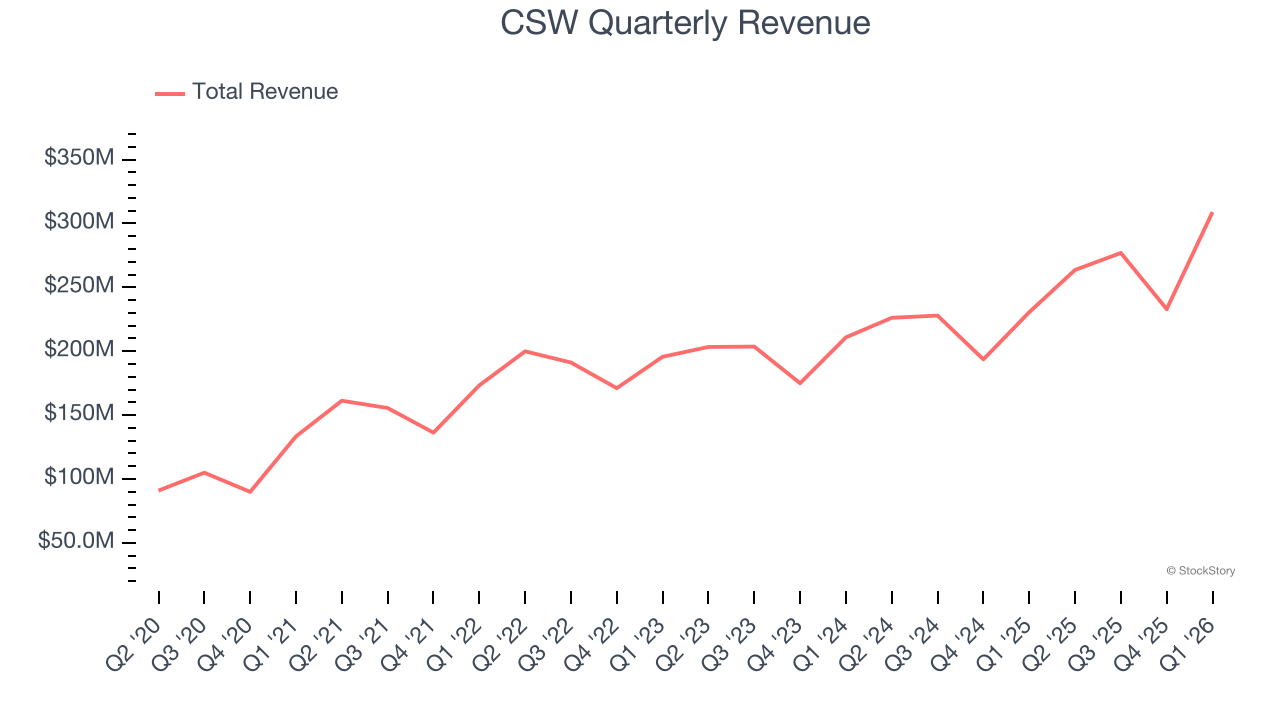

1. Skyrocketing Revenue Shows Strong Momentum

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Luckily, CSW’s sales grew at an incredible 20.9% compounded annual growth rate over the last five years. Its growth surpassed the average industrials company and shows its offerings resonate with customers.

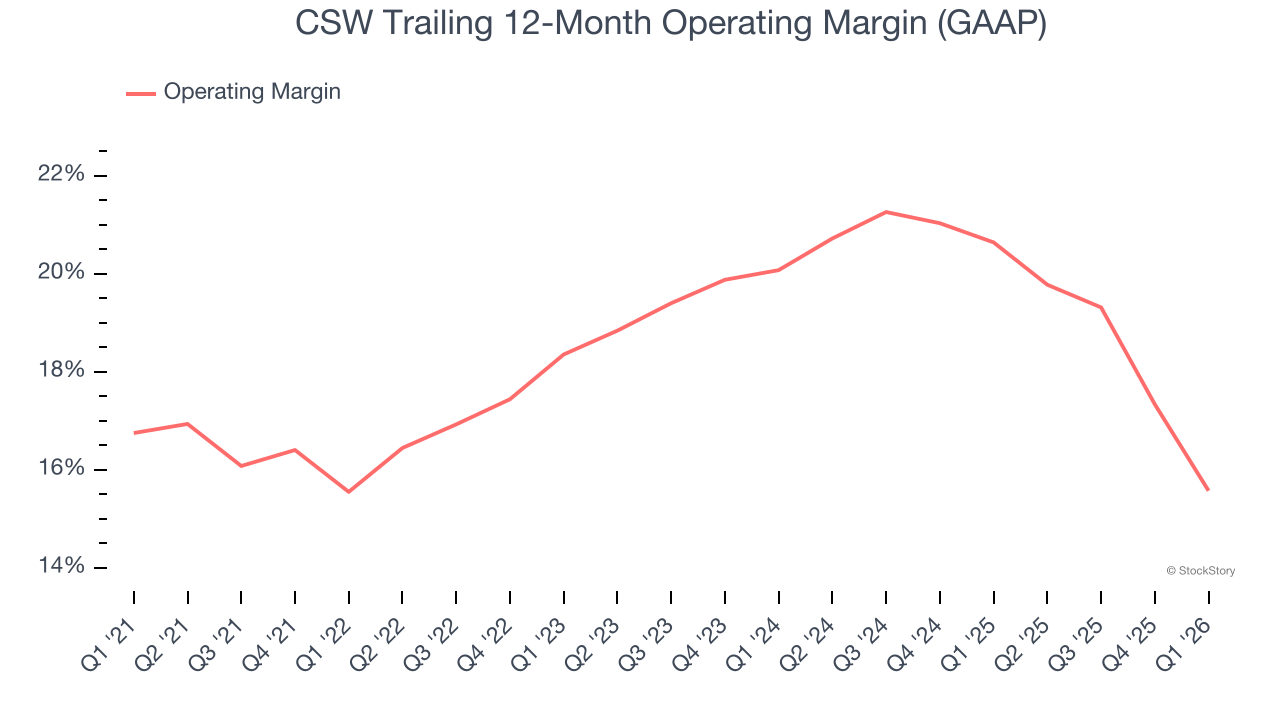

2. Operating Margin Reveals a Well-Run Organization

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses — everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

CSW’s operating margin has generally stayed the same over the last 12 months, averaging 18% over the last five years. This profitability was elite for an industrials business thanks to its efficient cost structure and economies of scale. This is seen in its fast historical revenue growth and healthy gross margin, which is why we look at all three data points together.

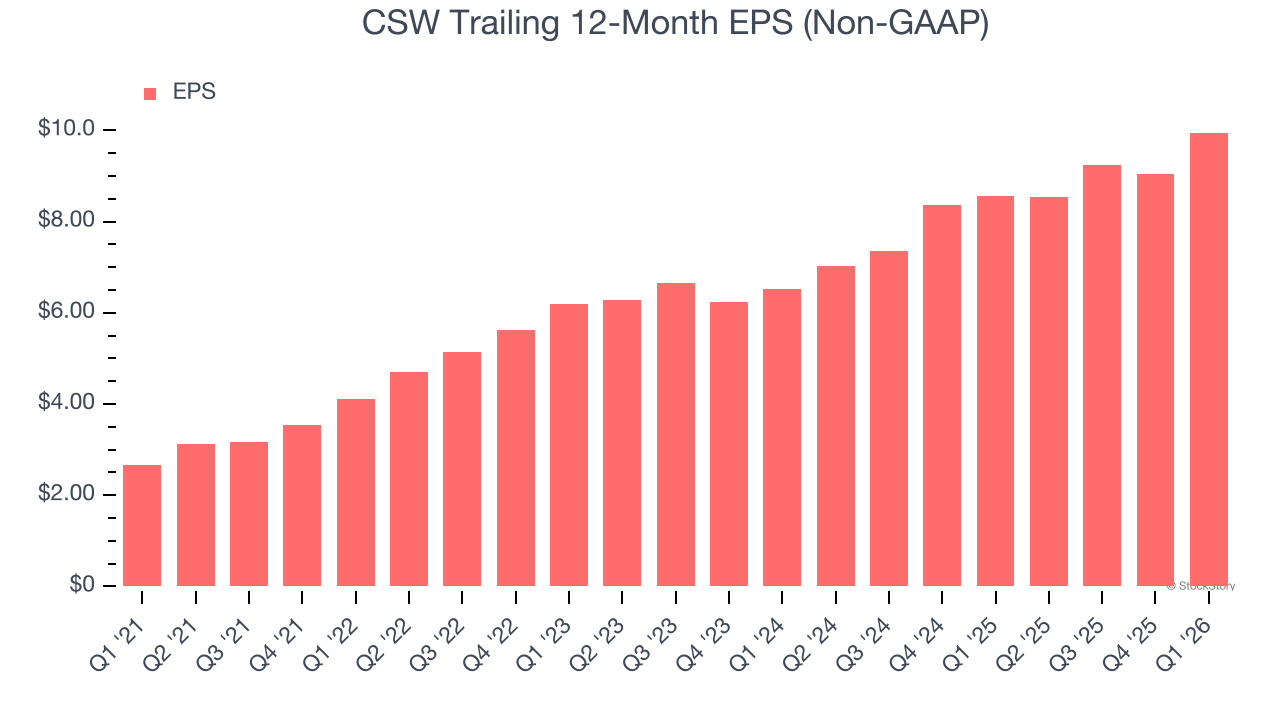

3. Outstanding Long-Term EPS Growth

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

CSW’s EPS grew at 30.1% compounded annual growth rate over the last five years, higher than its 20.9% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Final Judgment

These are just a few reasons why CSW is a cream-of-the-crop industrials company. After the recent drawdown, the stock trades at 22.9× forward P/E (or $270.70 per share). Is now the time to initiate a position? See for yourself in our comprehensive research report, it’s free.

Stocks We Like Even More Than CSW

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren’t just high-quality businesses. Something is happening with them right now. Elite fundamentals meet near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week’s Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.