Corpay trades at $353.00 per share and has stayed right on track with the overall market, gaining 15.3% over the last six months. At the same time, the S&P 500 has returned 10.9%.

Is now the time to buy CPAY? Find out in our full research report, it’s free.

Why Is Corpay a Good Business?

Formerly known as FLEETCOR until its 2024 rebrand, Corpay (NYSE: CPAY) provides specialized payment solutions for businesses to manage vehicle expenses, corporate payments, and lodging costs with enhanced control and reporting capabilities.

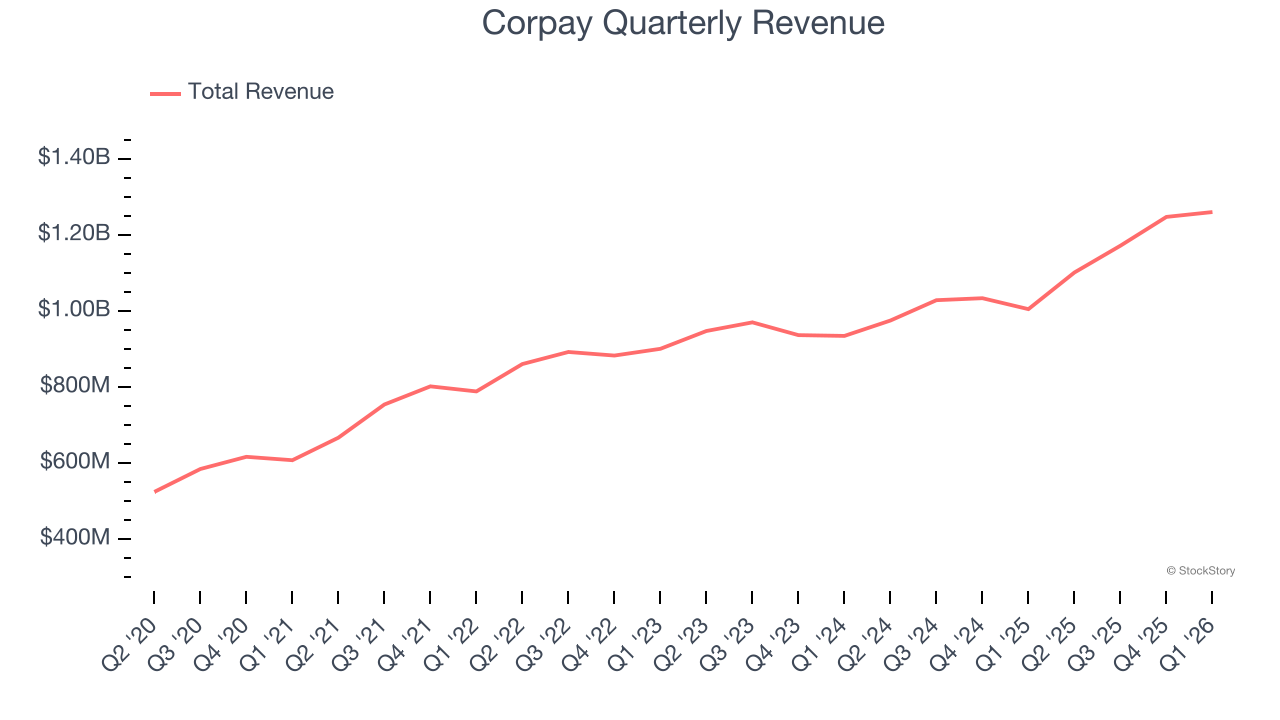

1. Skyrocketing Revenue Shows Strong Momentum

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

Over the last five years, Corpay grew its revenue at an impressive 15.4% compounded annual growth rate. Its growth beat the average financials company and shows its offerings resonate with customers.

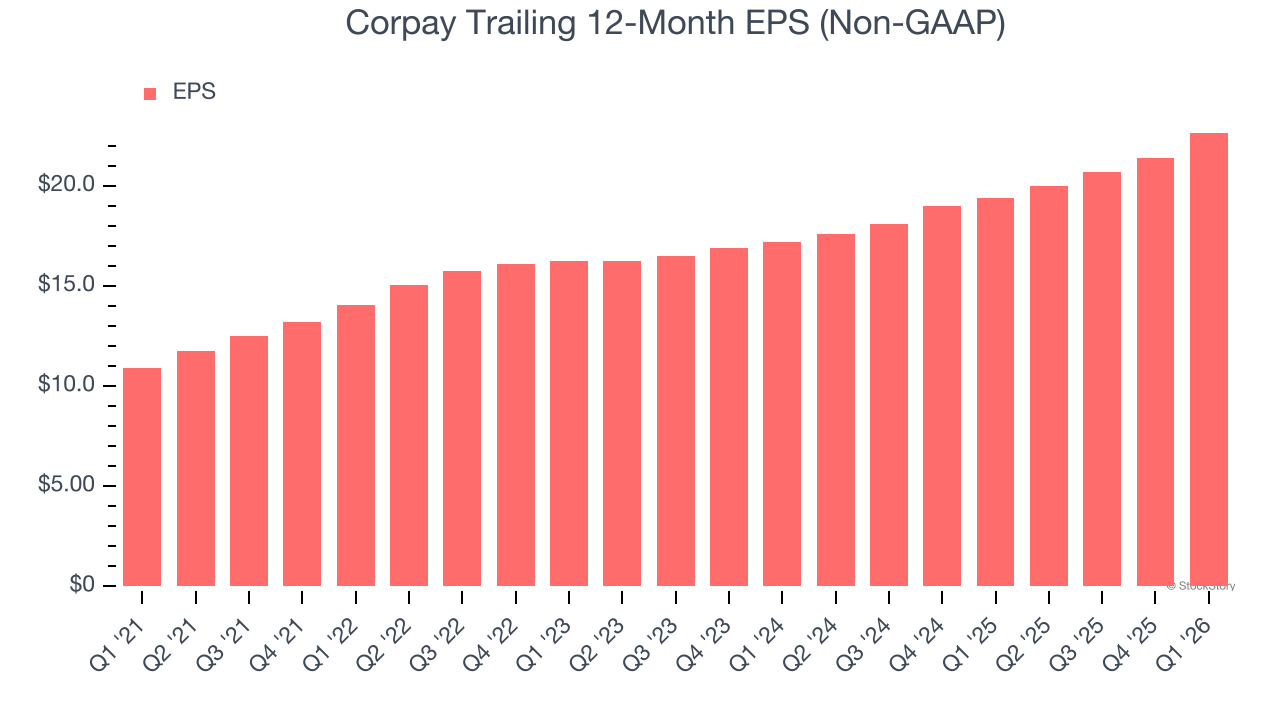

2. EPS Increasing Steadily

Analyzing the long-term change in earnings per share (EPS) shows whether a company’s incremental sales were profitable — for example, revenue could be inflated through excessive spending on advertising and promotions.

Corpay’s solid 15.8% annual EPS growth over the last five years aligns with its revenue performance. This tells us its incremental sales were profitable.

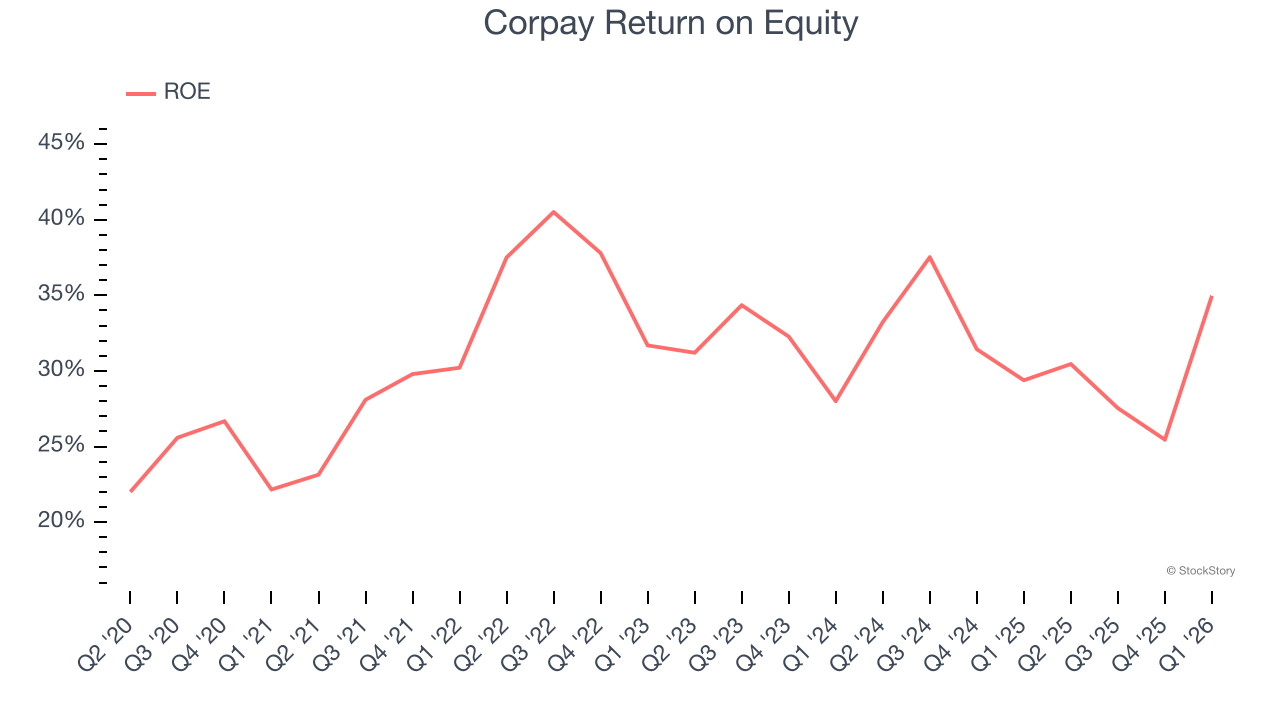

3. Stellar ROE Showcases Lucrative Growth Opportunities

Return on equity, or ROE, quantifies financial firm profitability relative to shareholder equity — an essential capital source for these institutions. Over extended periods, superior ROE performance drives faster shareholder wealth compounding through reinvestment, share repurchases, and dividend growth.

Over the last five years, Corpay has averaged an ROE of 31.7%, exceptional for a company operating in a sector where the average shakes out around 10% and those putting up 25%+ are greatly admired. This shows Corpay has a strong competitive moat.

Final Judgment

These are just a few reasons Corpay is a high-quality business worth owning, but at $353.00 per share (or 12.9× forward P/E), is now the time to initiate a position? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than Corpay

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren’t just high-quality businesses. Something is happening with them right now. Elite fundamentals meet near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week’s Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.