Over the last six months, Lowe’s shares have sunk to $218.65, producing a disappointing 11.7% loss - a stark contrast to the S&P 500’s 10.9% gain. This may have investors wondering how to approach the situation.

Is there a buying opportunity in Lowe's, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is Lowe's Not Exciting?

Despite the more favorable entry price, we’re sitting this one out for now. Here are three reasons why there are better opportunities than LOW, plus one stock we’d rather own.

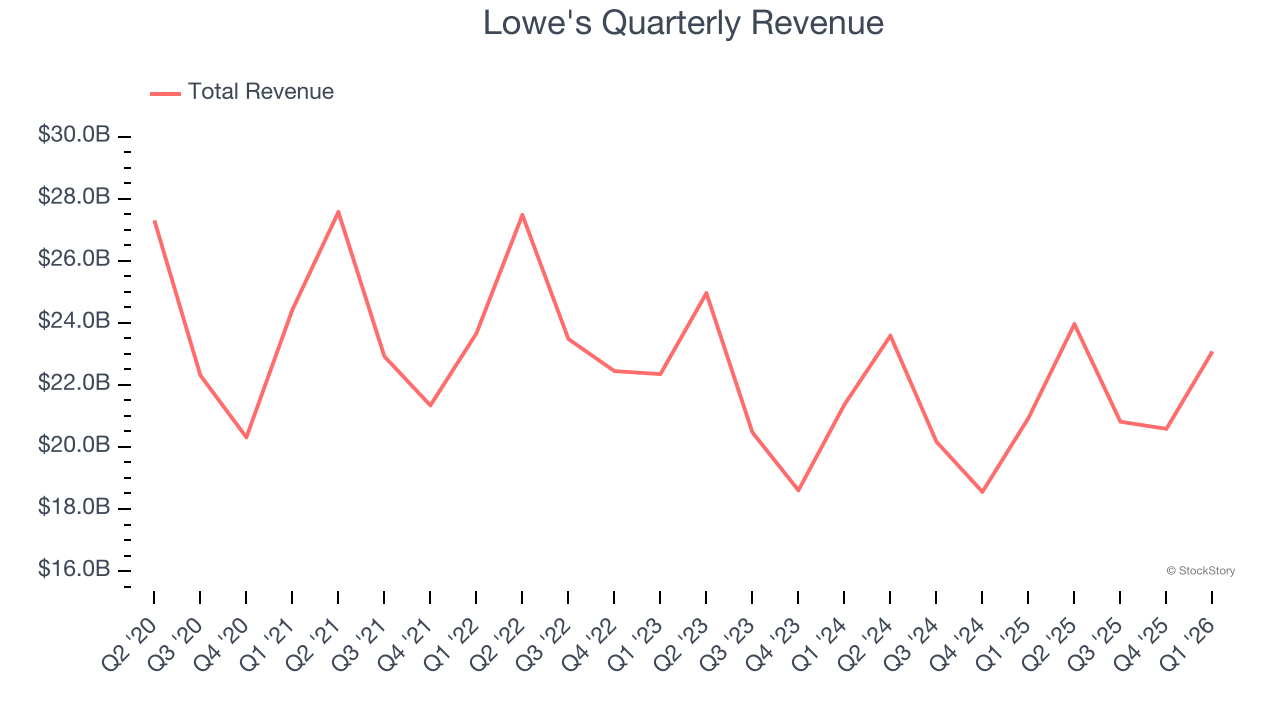

1. Revenue Spiraling Downwards

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Lowe’s demand was weak over the last three years as its sales fell at a 2.6% annual rate. This was below our standards and signals it’s a lower quality business.

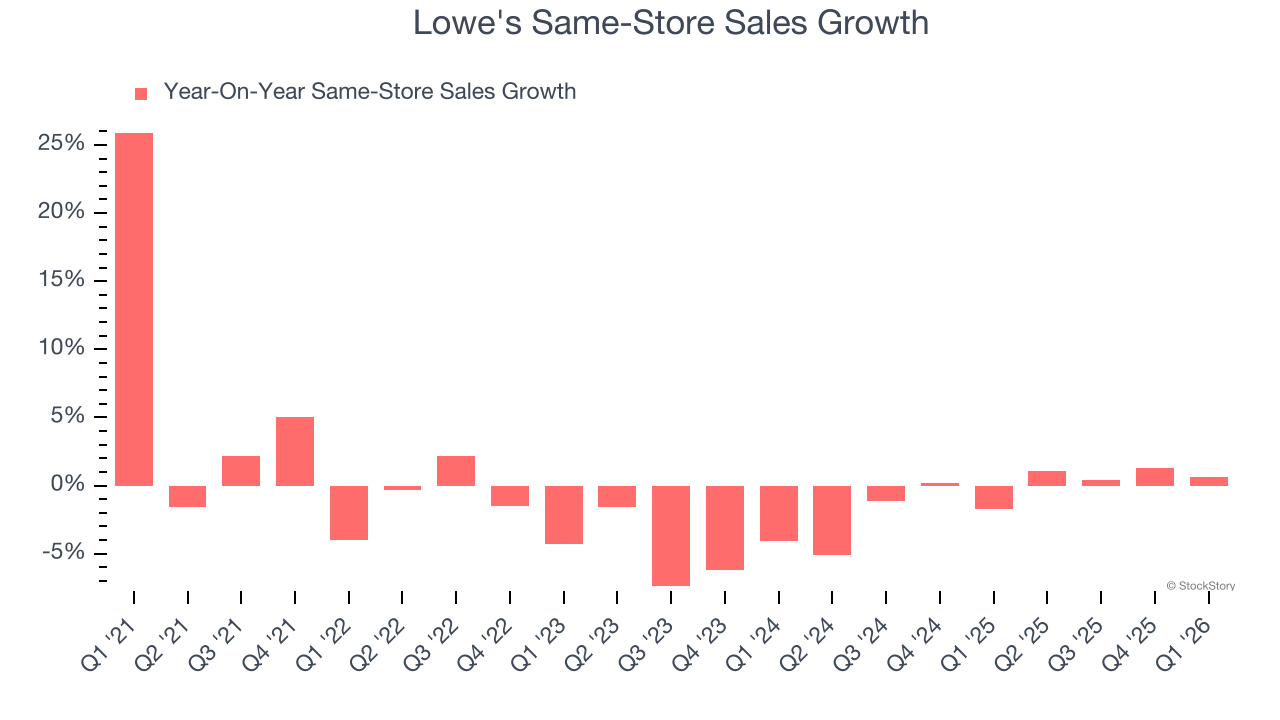

2. Flat Same-Store Sales Indicate Weak Demand

Same-store sales is a key performance indicator used to measure organic growth at brick-and-mortar shops for at least a year.

Lowe’s demand within its existing locations has barely increased over the last two years as its same-store sales were flat.

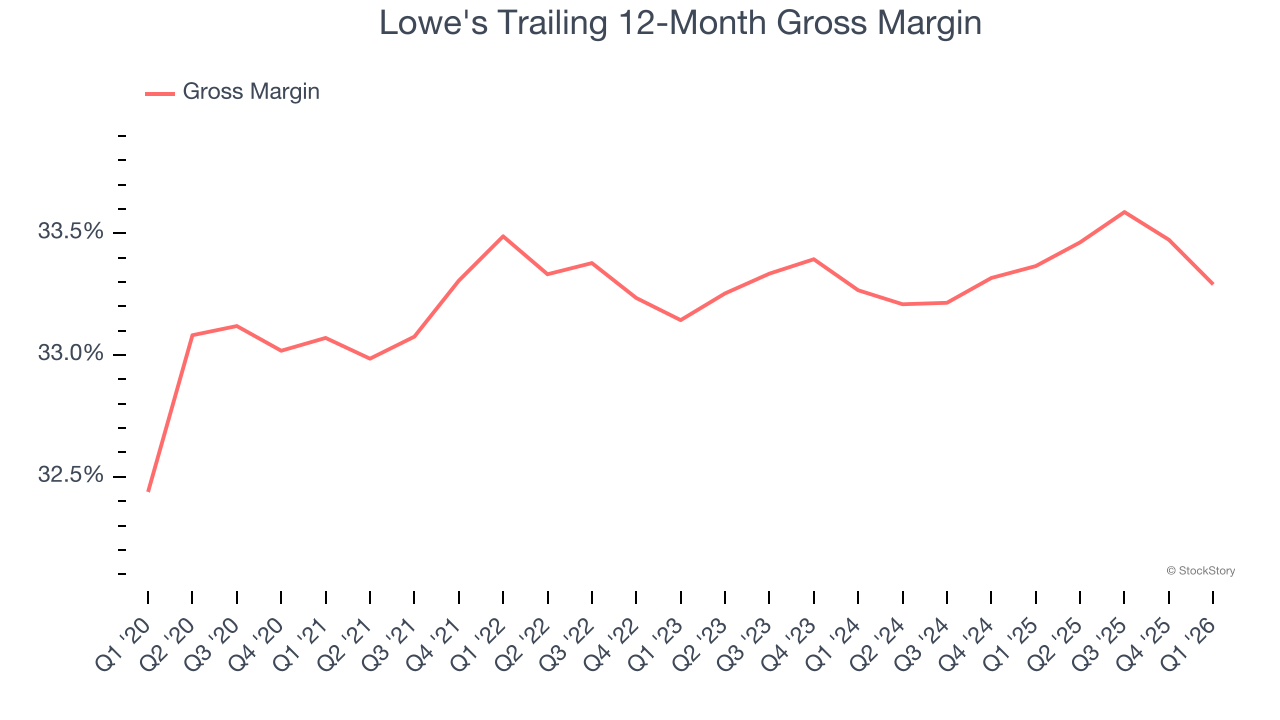

3. Low Gross Margin Reveals Weak Structural Profitability

We prefer higher gross margins because they not only make it easier to generate more operating profits but also indicate product differentiation, negotiating leverage, and pricing power.

Lowe's has bad unit economics for a retailer, signaling it operates in a competitive market and lacks pricing power because its inventory is sold in many places. As you can see below, it averaged a 33.3% gross margin over the last two years. That means Lowe's paid its suppliers a lot of money ($66.67 for every $100 in revenue) to run its business.

Final Judgment

Lowe's isn’t a terrible business, but it isn’t one of our picks. Following the recent decline, the stock trades at 17.6× forward P/E (or $218.65 per share). Investors with a higher risk tolerance might like the company, but we think the potential downside is too great. We’re fairly confident there are better investments elsewhere. We’d suggest looking at one of Charlie Munger’s all-time favorite businesses.

Stocks We Like More Than Lowe's

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.