Over the last six months, Thermo Fisher’s shares have sunk to $464.50, producing a disappointing 17.4% loss - a stark contrast to the S&P 500’s 10.9% gain. This might have investors contemplating their next move.

Is there a buying opportunity in Thermo Fisher, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is Thermo Fisher Not Exciting?

Even with the cheaper entry price, we don’t have much confidence in Thermo Fisher. Here are three reasons why there are better opportunities than TMO, plus one stock we’d rather own.

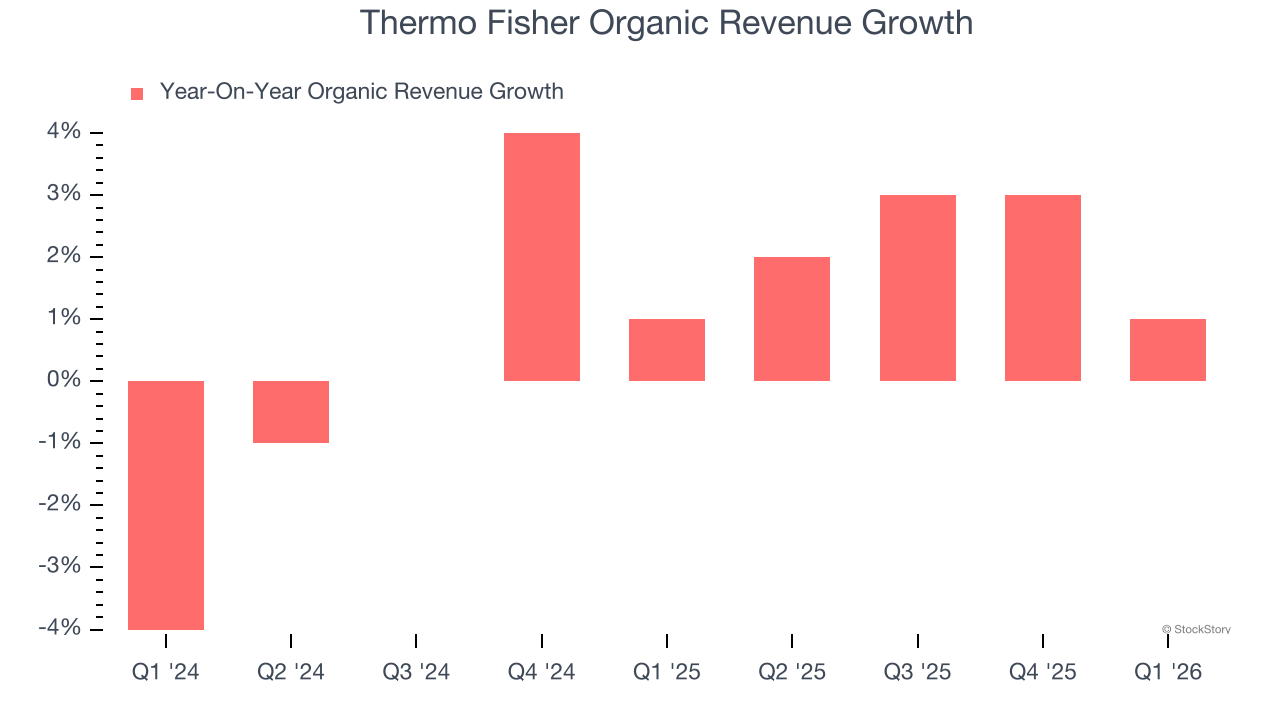

1. Slow Organic Growth Suggests Waning Demand In Core Business

Investors interested in Research Tools & Consumables companies should track organic revenue in addition to reported revenue. This metric gives visibility into Thermo Fisher’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Thermo Fisher’s organic revenue averaged 1.6% year-on-year growth. This performance was underwhelming and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

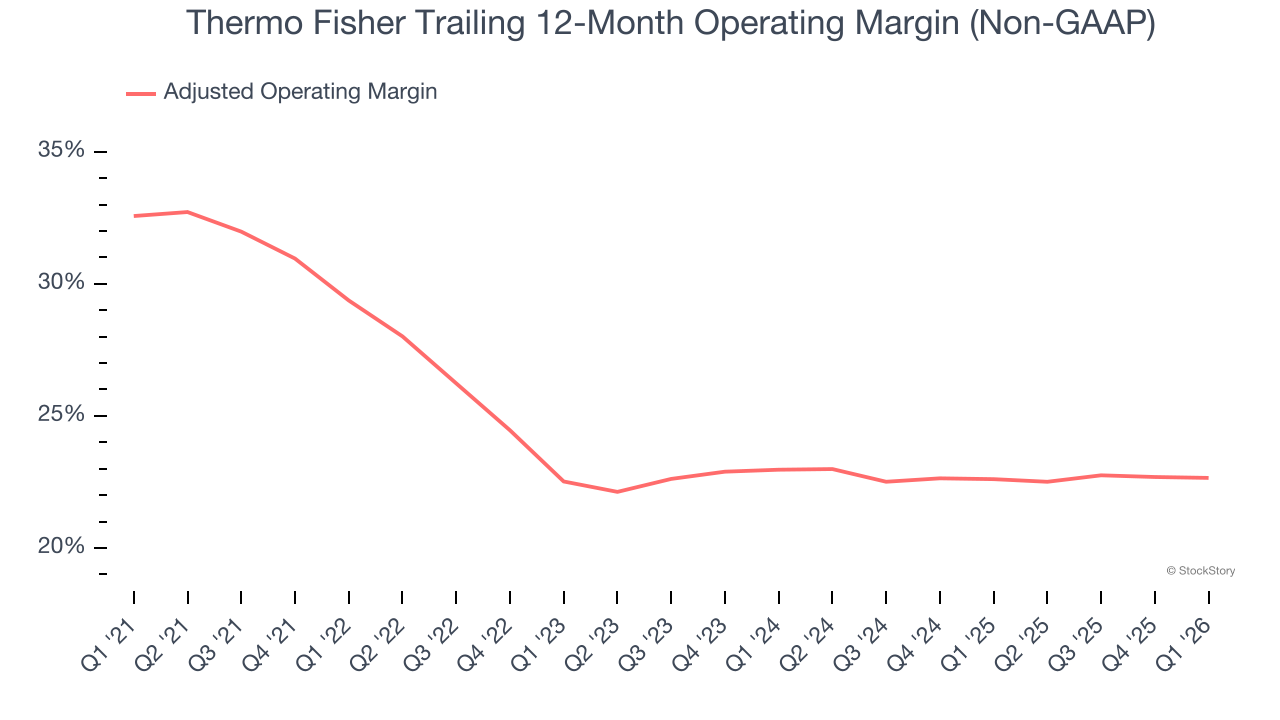

2. Shrinking Adjusted Operating Margin

Adjusted operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D. It also removes various one-time costs to paint a better picture of normalized profits.

Analyzing the trend in its profitability, Thermo Fisher’s adjusted operating margin decreased by 6.7 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its adjusted operating margin for the trailing 12 months was 22.7%.

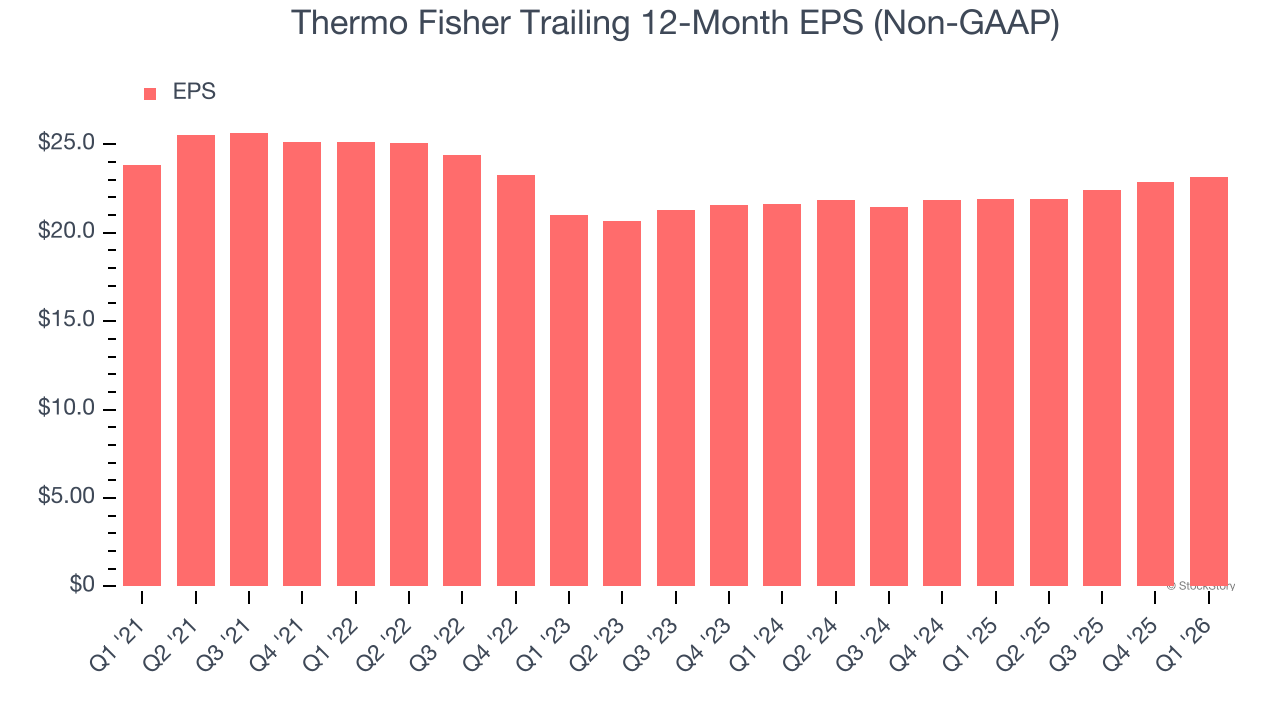

3. EPS Growth Has Stalled

Analyzing the long-term change in earnings per share (EPS) shows whether a company’s incremental sales were profitable — for example, revenue could be inflated through excessive spending on advertising and promotions.

Thermo Fisher’s flat EPS over the last five years was below its 4.7% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

Thermo Fisher isn’t a terrible business, but it isn’t one of our picks. Following the recent decline, the stock trades at 18.6× forward P/E (or $464.50 per share). This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We’re pretty confident there are superior stocks to buy right now. We’d recommend looking at an all-weather company that owns household favorite Taco Bell.

High-Quality Stocks for All Market Conditions

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don’t just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn’t over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.