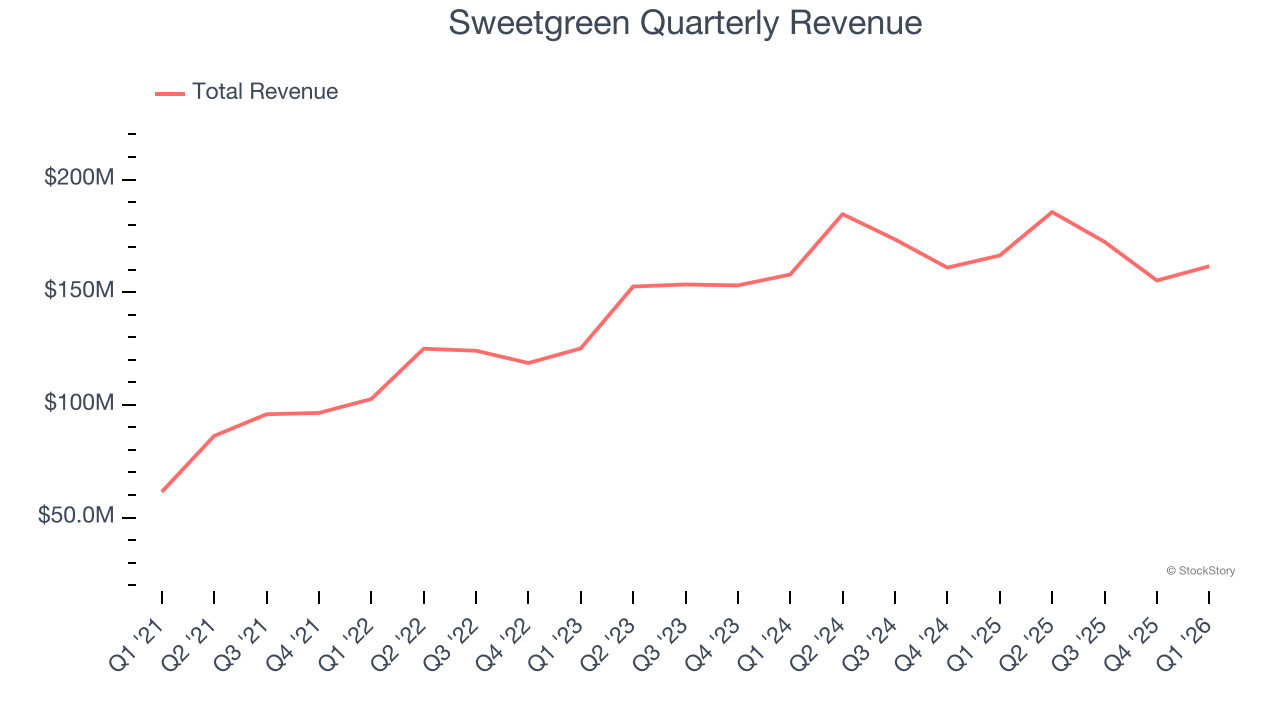

Casual salad chain Sweetgreen (NYSE: SG) fell short of the market’s revenue expectations in Q1 CY2026, with sales falling 2.9% year on year to $161.5 million. Its GAAP profit of $1.05 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Sweetgreen? Find out by accessing our full research report, it’s free.

Sweetgreen (SG) Q1 CY2026 Highlights:

- Revenue: $161.5 million vs analyst estimates of $164.1 million (2.9% year-on-year decline, 1.6% miss)

- EPS (GAAP): $1.05 vs analyst estimates of -$0.24 (significant beat)

- Adjusted EBITDA: -$8.09 million (-5% margin, 2,937% year-on-year decline)

- EBITDA guidance for the full year is $3.5 million at the midpoint, above analyst estimates of $3.23 million

- Adjusted EBITDA Margin: -5%, down from 0.2% in the same quarter last year

- Free Cash Flow was -$29.56 million compared to -$29.86 million in the same quarter last year

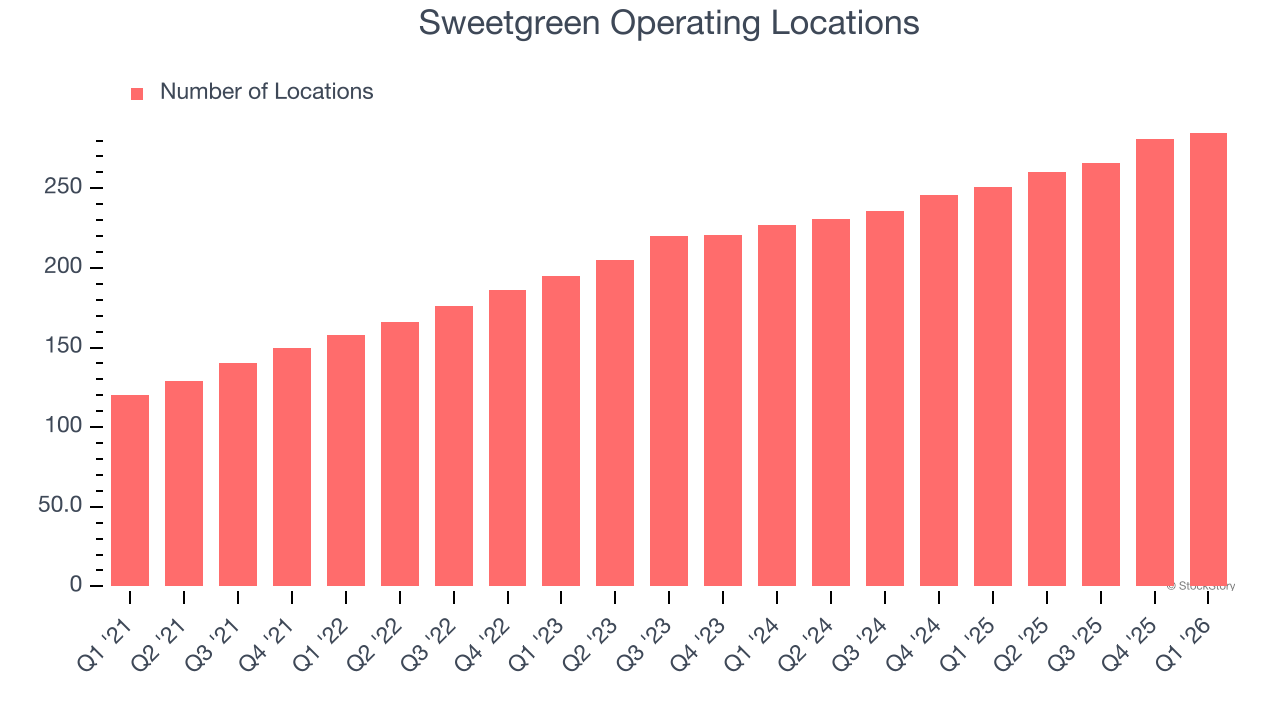

- Locations: 285 at quarter end, up from 251 in the same quarter last year

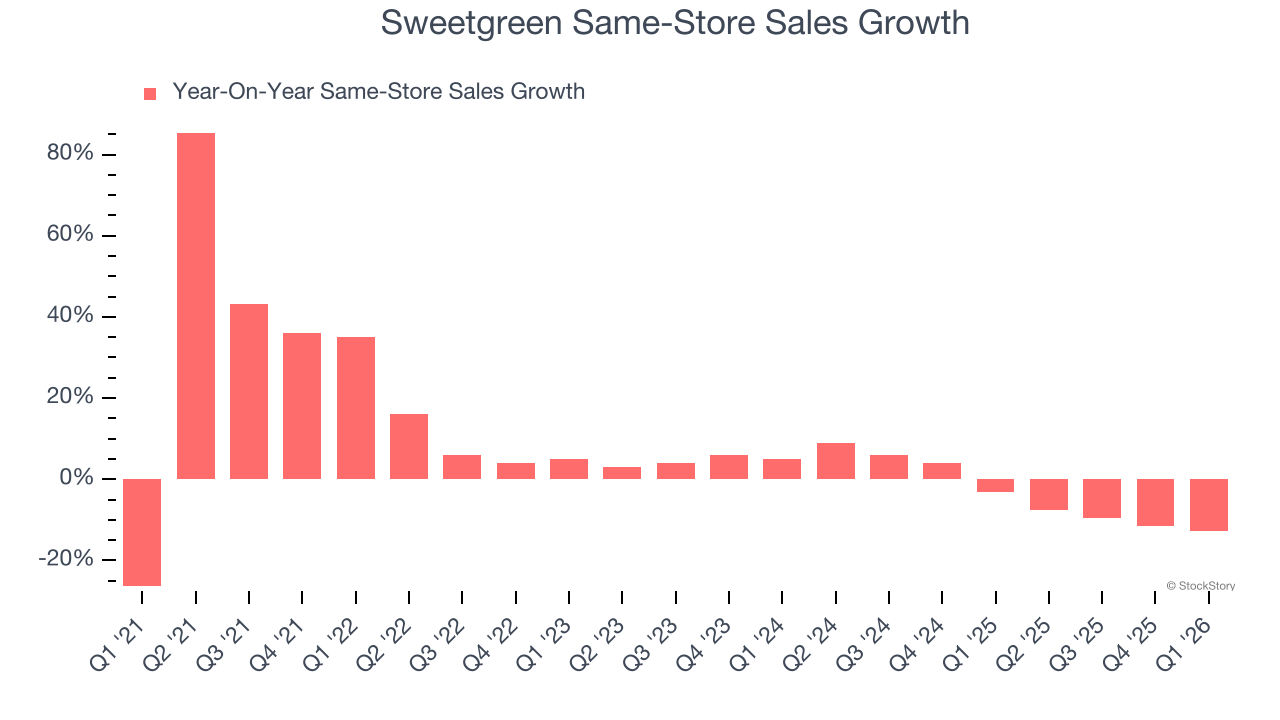

- Same-Store Sales fell 12.8% year on year (-3.1% in the same quarter last year)

- Market Capitalization: $816.3 million

Company Overview

Founded in 2007 by three Georgetown University alum, Sweetgreen (NYSE: SG) is a casual quick service chain known for its healthy salads and bowls.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $674.7 million in revenue over the past 12 months, Sweetgreen is a small restaurant chain, which sometimes brings disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale. On the bright side, it can grow faster because it has more white space to build new restaurants.

As you can see below, Sweetgreen grew its sales at an impressive 15.3% compounded annual growth rate over the last six years as it opened new restaurants and expanded its reach.

This quarter, Sweetgreen missed Wall Street’s estimates and reported a rather uninspiring 2.9% year-on-year revenue decline, generating $161.5 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 7.4% over the next 12 months, a deceleration versus the last six years. Still, this projection is above average for the sector and implies the market is baking in some success for its newer menu offerings.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Restaurant Performance

Number of Restaurants

A restaurant chain’s total number of dining locations influences how much it can sell and how quickly revenue can grow.

Sweetgreen sported 285 locations in the latest quarter. Over the last two years, it has opened new restaurants at a rapid clip by averaging 11.9% annual growth, among the fastest in the restaurant sector. This gives it a chance to scale into a mid-sized business over time.

When a chain opens new restaurants, it usually means it’s investing for growth because there’s healthy demand for its meals and there are markets where its concepts have few or no locations.

Same-Store Sales

A company's restaurant base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales gives us insight into this topic because it measures organic growth at restaurants open for at least a year.

Sweetgreen’s demand has been shrinking over the last two years as its same-store sales have averaged 3.2% annual declines. This performance is concerning - it shows Sweetgreen artificially boosts its revenue by building new restaurants. We’d like to see a company’s same-store sales rise before it takes on the costly, capital-intensive endeavor of expanding its restaurant base.

In the latest quarter, Sweetgreen’s same-store sales fell by 12.8% year on year. This decrease represents a further deceleration from its historical levels. We hope the business can get back on track.

Key Takeaways from Sweetgreen’s Q1 Results

It was good to see Sweetgreen beat analysts’ EPS expectations this quarter. We were also glad its full-year EBITDA guidance trumped Wall Street’s estimates. On the other hand, its EBITDA missed and its same-store sales fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 3.1% to $6.80 immediately following the results.

Is Sweetgreen an attractive investment opportunity at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).