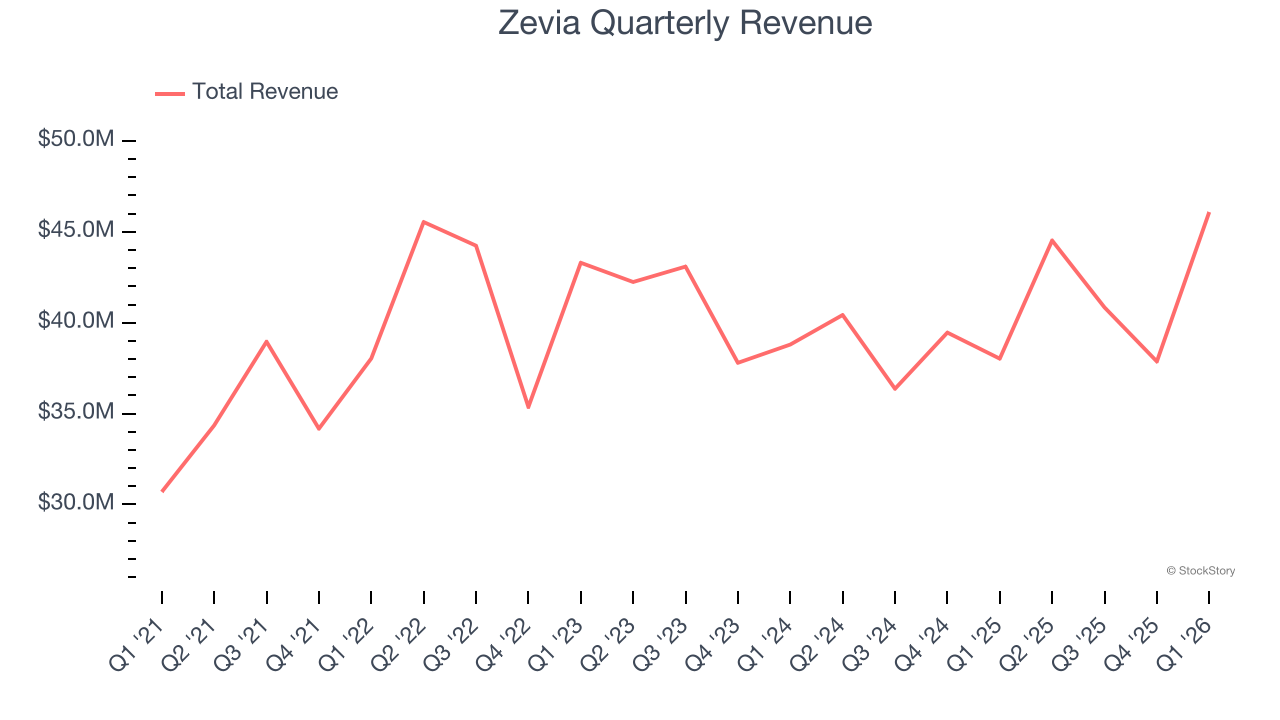

Beverage company Zevia (NYSE: ZVIA) reported Q1 CY2026 results beating Wall Street’s revenue expectations, with sales up 21.2% year on year to $46.09 million. Revenue guidance for the full year exceeded analysts’ estimates, but next quarter’s guidance of $44 million was less impressive, coming in 3% below expectations. Its GAAP loss of $0.03 per share was $0.01 above analysts’ consensus estimates.

Is now the time to buy Zevia? Find out by accessing our full research report, it’s free.

Zevia (ZVIA) Q1 CY2026 Highlights:

- Revenue: $46.09 million vs analyst estimates of $41.09 million (21.2% year-on-year growth, 12.2% beat)

- EPS (GAAP): -$0.03 vs analyst estimates of -$0.04 ($0.01 beat)

- Adjusted EBITDA: $939,000 (2% margin, 129% year-on-year growth)

- The company slightly lifted its revenue guidance for the full year to $172.5 million at the midpoint from $171 million

- EBITDA guidance for the full year is $3 million at the midpoint, above analyst estimates of -$405,960

- Operating Margin: -5.1%, up from -16.8% in the same quarter last year

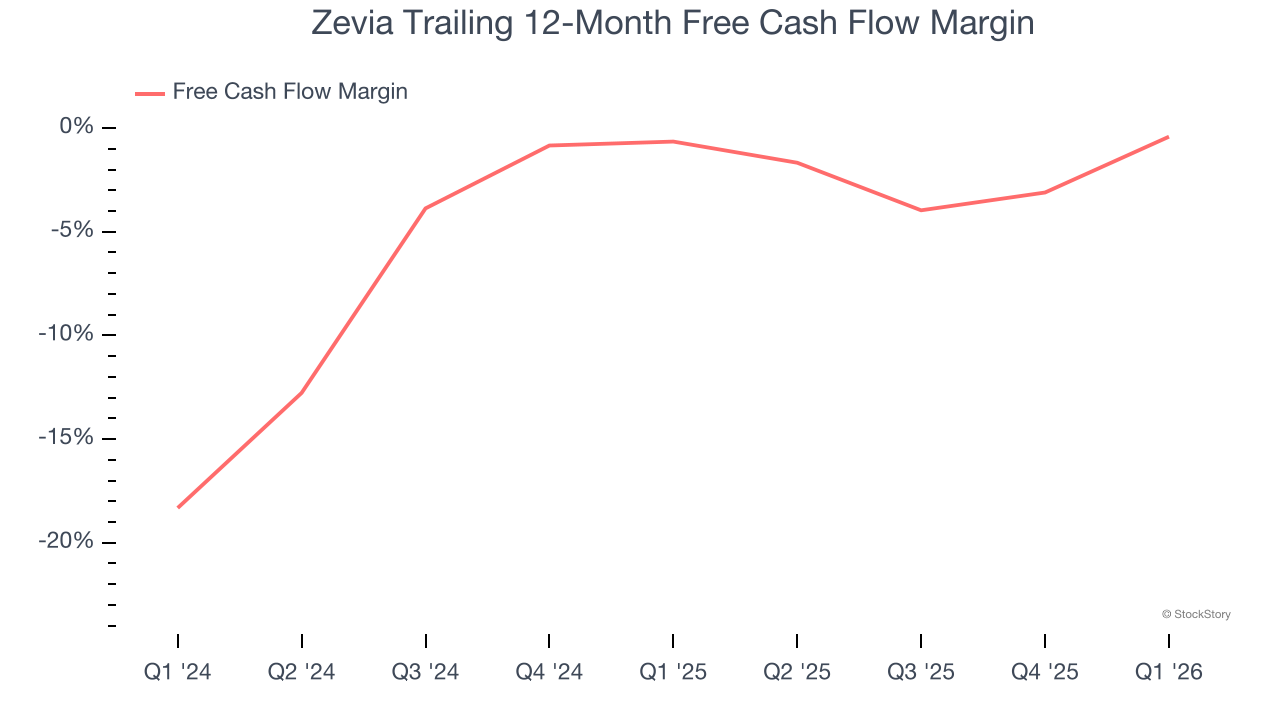

- Free Cash Flow was $1.37 million, up from -$2.94 million in the same quarter last year

- Market Capitalization: $89.65 million

Company Overview

With a primary focus on soda but also a presence in energy drinks and teas, Zevia (NYSE: ZVIA) is a better-for-you beverage company.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $169.3 million in revenue over the past 12 months, Zevia is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

As you can see below, Zevia struggled to increase demand as its $169.3 million of sales for the trailing 12 months was close to its revenue three years ago. This shows demand was soft, a rough starting point for our analysis.

This quarter, Zevia reported robust year-on-year revenue growth of 21.2%, and its $46.09 million of revenue topped Wall Street estimates by 12.2%. Company management is currently guiding for a 1.2% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 2.2% over the next 12 months. Although this projection suggests its newer products will fuel better top-line performance, it is still below the sector average.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Zevia broke even from a free cash flow perspective over the last two years, giving the company limited opportunities to return capital to shareholders.

Zevia’s free cash flow clocked in at $1.37 million in Q1, equivalent to a 3% margin. Its cash flow turned positive after being negative in the same quarter last year, but we wouldn’t put too much weight on the short term because investment needs can be seasonal, causing temporary swings. Long-term trends carry greater meaning.

Key Takeaways from Zevia’s Q1 Results

We were impressed by how significantly Zevia blew past analysts’ EBITDA expectations this quarter. We were also excited its adjusted operating income outperformed Wall Street’s estimates by a wide margin. On the other hand, its revenue guidance for next quarter missed. Zooming out, we think this quarter featured some important positives. The stock traded up 10.7% to $1.31 immediately following the results.

Zevia had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).