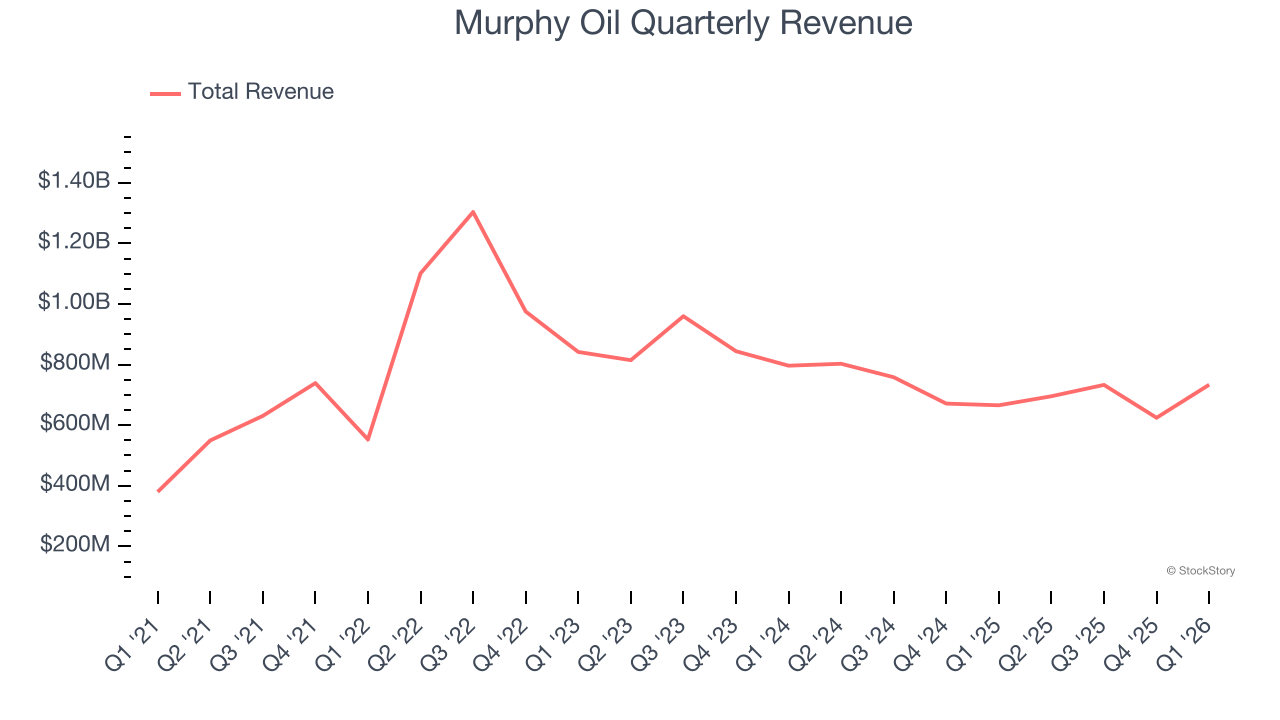

Oil and gas producer Murphy Oil (NYSE: MUR) announced better-than-expected revenue in Q1 CY2026, with sales up 10.2% year on year to $733.6 million. Its GAAP profit of $0.37 per share was 8% above analysts’ consensus estimates.

Is now the time to buy Murphy Oil? Find out by accessing our full research report, it’s free.

Murphy Oil (MUR) Q1 CY2026 Highlights:

- Revenue: $733.6 million vs analyst estimates of $707.1 million (10.2% year-on-year growth, 3.7% beat)

- EPS (GAAP): $0.37 vs analyst estimates of $0.34 (8% beat)

- Adjusted Operating Income: $138.3 million vs analyst estimates of $126.2 million (18.8% margin, 9.6% beat)

- Operating Margin: 18.8%, down from 21.6% in the same quarter last year

- Free Cash Flow was $41,400, up from -$73.64 million in the same quarter last year

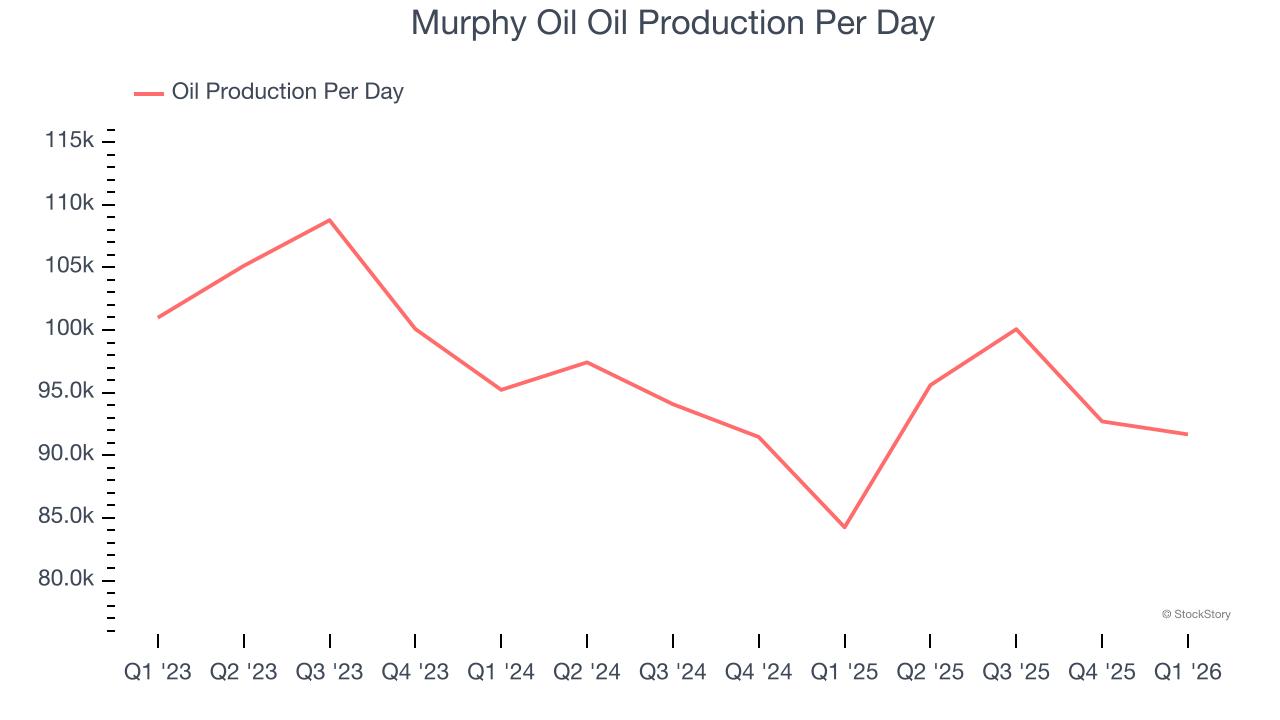

- Oil production per day: up 8.8% year on year

- Market Capitalization: $5.58 billion

“During these uncertain times, our strategy is to stay anchored to what we control—disciplined capital allocation, safe and reliable operations, and our long‑cycle projects. In the first quarter, this focus translated into strong execution across our portfolio with meaningful progress at Lac Da Vang in Vietnam, advancement of the high-impact Chinook #8 well in the Gulf of America, and sustained outperformance from our US and Canada onshore programs,” stated Eric M. Hambly, President and Chief Executive Officer.

Company Overview

Operating in waters over a mile deep in the Gulf of Mexico and extracting hydrocarbons from tight shale rock formations in Texas, Murphy Oil (NYSE: MUR) explores for and produces crude oil, natural gas, and natural gas liquids from fields in North America and Asia.

Revenue Growth

A company’s long-term performance can give signals about its business quality. Even a bad business, especially in a cyclical industry, can shine for a year or so, but a top-tier one should exhibit resilience through cycles. Luckily, Murphy Oil’s sales grew at a solid 15.7% compounded annual growth rate over the last five years. Its growth beat the average energy upstream and integrated energy company and shows its offerings resonate with customers.

Energy cycles can be long enough that a single five-year period can still reflect one price environment, which is why an additional, decade-long view can help capture through-cycle performance. Murphy Oil’s annualized revenue growth of 0.9% over the last ten years is below its five-year trend, but we still think the results were respectable.

While looking at revenue is important, it can also introduce noise around commodity prices and M&A. Analyzing drivers of revenue, on the other hand, highlights what is happening inside the asset base and whether the economic footprint of a company is expanding. Over the last two years, Murphy Oil’s oil production per day averaged 3.3% year-on-year declines. On the other hand, its natural gas production per day averaged 4.7% year-on-year growth.

This quarter, Murphy Oil reported year-on-year revenue growth of 10.2%, and its $733.6 million of revenue exceeded Wall Street’s estimates by 3.7%. This quarter, Murphy Oil reported year-on-year Oil production per day growth of 8.8%.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

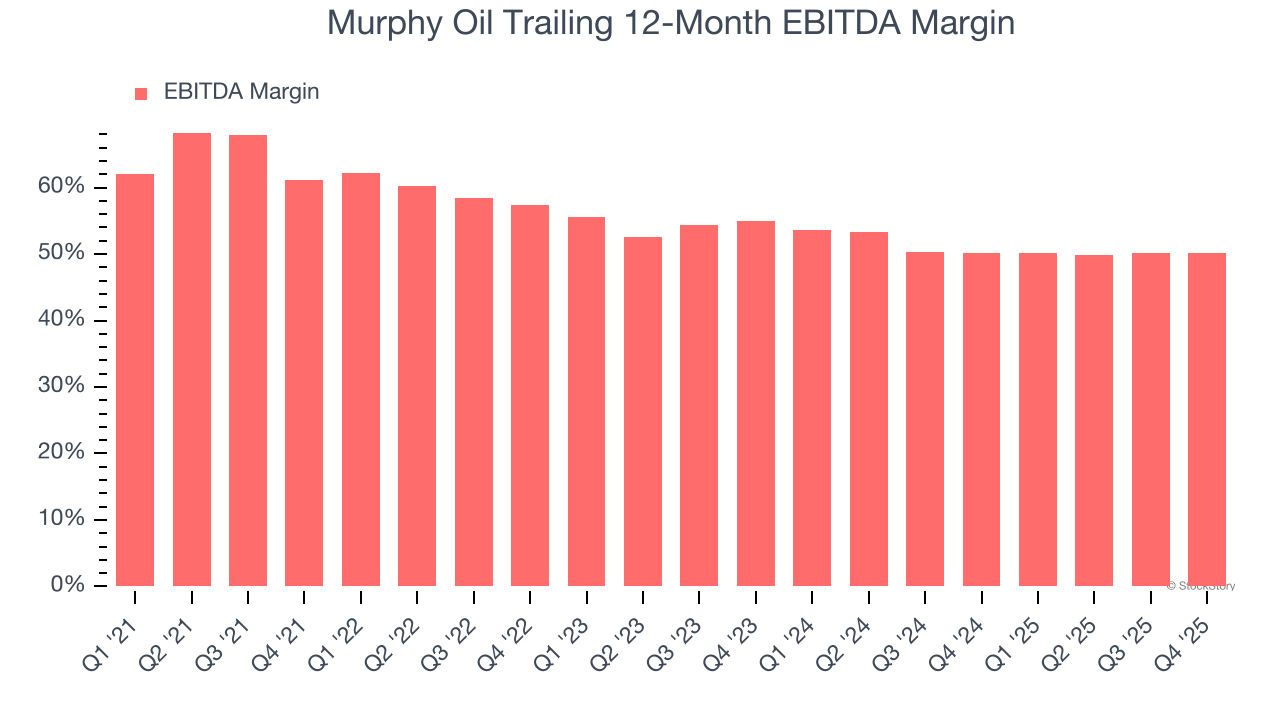

Adjusted EBITDA Margin

Murphy Oil has been an efficient company over the last five years. It was one of the more profitable businesses in the energy upstream and integrated energy sector, boasting an average EBITDA margin of 54.4%.

Analyzing the trend in its profitability, Murphy Oil’s EBITDA margin decreased by 10.1 percentage points over the last year. Even though its historical margin was healthy, shareholders will want to see Murphy Oil become more profitable in the future.

in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Cash Is King

Adjusted EBITDA shows how profitable a company’s existing wells are before financing and reinvestment decisions, but free cash flow shows how much value remains after paying the cost of replacing those wells. In upstream energy, production naturally declines over time, so companies must continuously reinvest just to stand still. A producer can report strong EBITDA margins yet generate little or no free cash flow if its wells decline quickly or if new drilling is expensive. Free cash flow therefore captures not only how efficiently a company produces hydrocarbons today, but also how costly it is to sustain that production into the future.

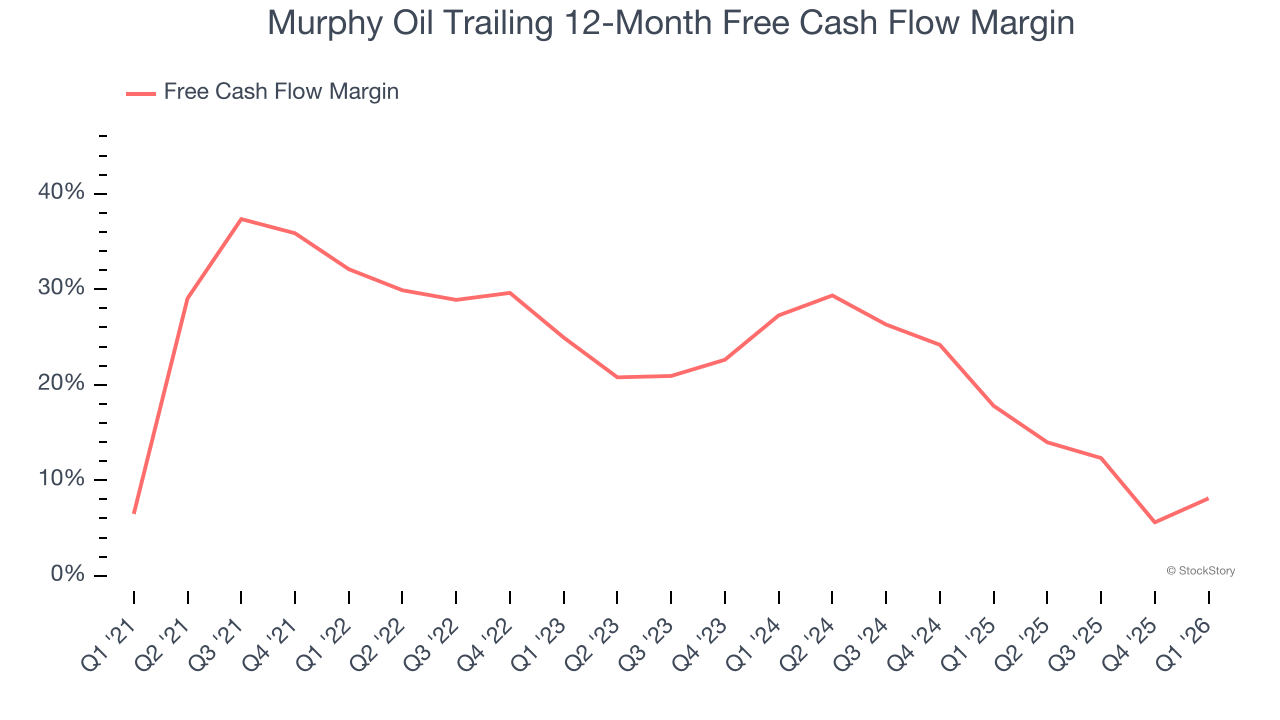

Murphy Oil has shown terrific cash profitability, enabling it to reinvest, return capital to investors, and stay ahead of the competition while maintaining an ample cushion. The company’s free cash flow margin was among the best in the energy upstream and integrated energy sector, averaging 22.3% over the last five years.

While the level of free cash flow margins is important, their consistency matters just as much.

Murphy Oil’s ratio of quarterly free cash flow volatility to WTI crude price volatility over the past five years was 5.1 (lower is better), indicating excellent insulation from commodity swings. This stability supports capital access in downturns and positions Murphy Oil to act as a consolidator when weaker peers are forced to retrench.

You may be asking why we wait until the free cash flow line to perform this stability analysis versus commodity prices. Why not compare revenue or EBITDA to WTI Crude prices in the case of Murphy Oil? Because what ultimately matters is not how much revenue or profit you earn when prices are high but how much cash you can generate when prices are low. Free cash flow is the superior metric because it includes everything from hedging prowess to growth and maintenance capex to management behavior during good times and bad.

Murphy Oil broke even from a free cash flow perspective in Q1. This result was good as its margin was 11.1 percentage points higher than in the same quarter last year, but we wouldn’t put too much weight on the short term because investment needs can be seasonal, causing temporary swings. Long-term trends carry greater meaning.

Key Takeaways from Murphy Oil’s Q1 Results

We enjoyed seeing Murphy Oil beat analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock remained flat at $38.96 immediately following the results.

Sure, Murphy Oil had a solid quarter, but if we look at the bigger picture, is this stock a buy? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).