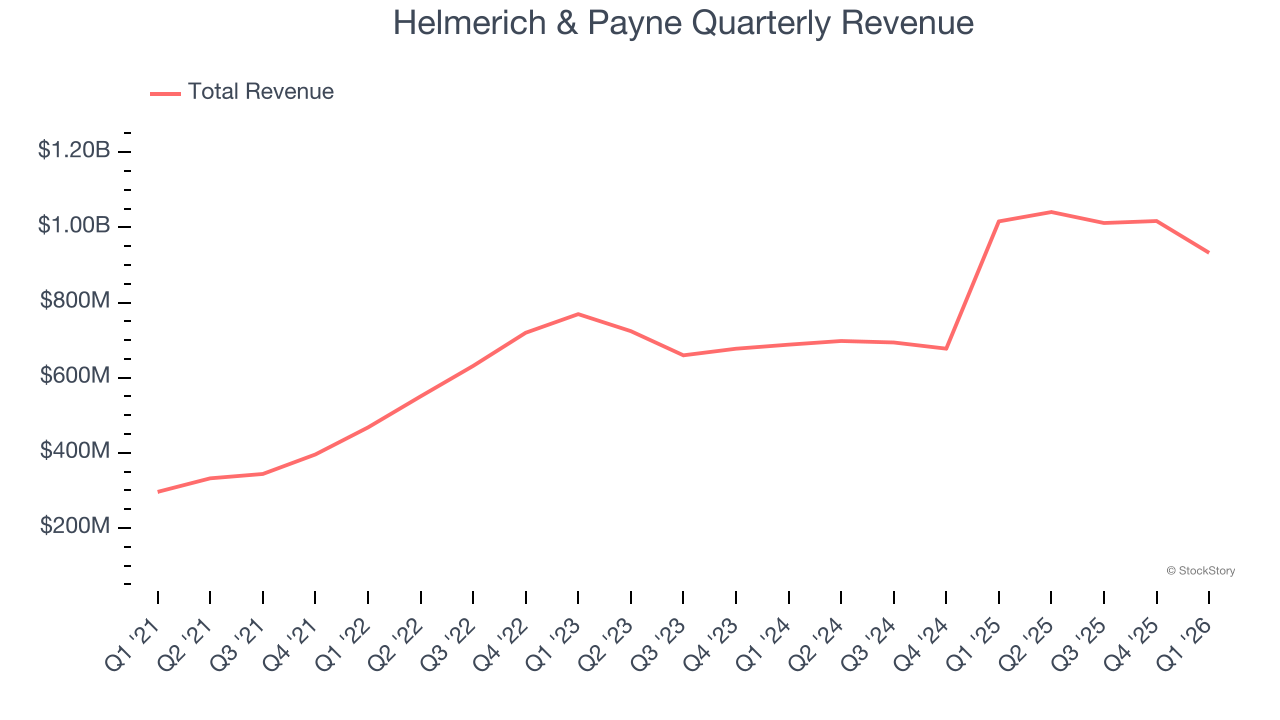

Land drilling contractor Helmerich & Payne (NYSE: HP) missed Wall Street’s revenue expectations in Q1 CY2026, with sales falling 8.2% year on year to $932.4 million. Its non-GAAP loss of $0.38 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Helmerich & Payne? Find out by accessing our full research report, it’s free.

Helmerich & Payne (HP) Q1 CY2026 Highlights:

- Revenue: $932.4 million vs analyst estimates of $950.3 million (8.2% year-on-year decline, 1.9% miss)

- Adjusted EPS: -$0.38 vs analyst estimates of -$0.04 (significant miss)

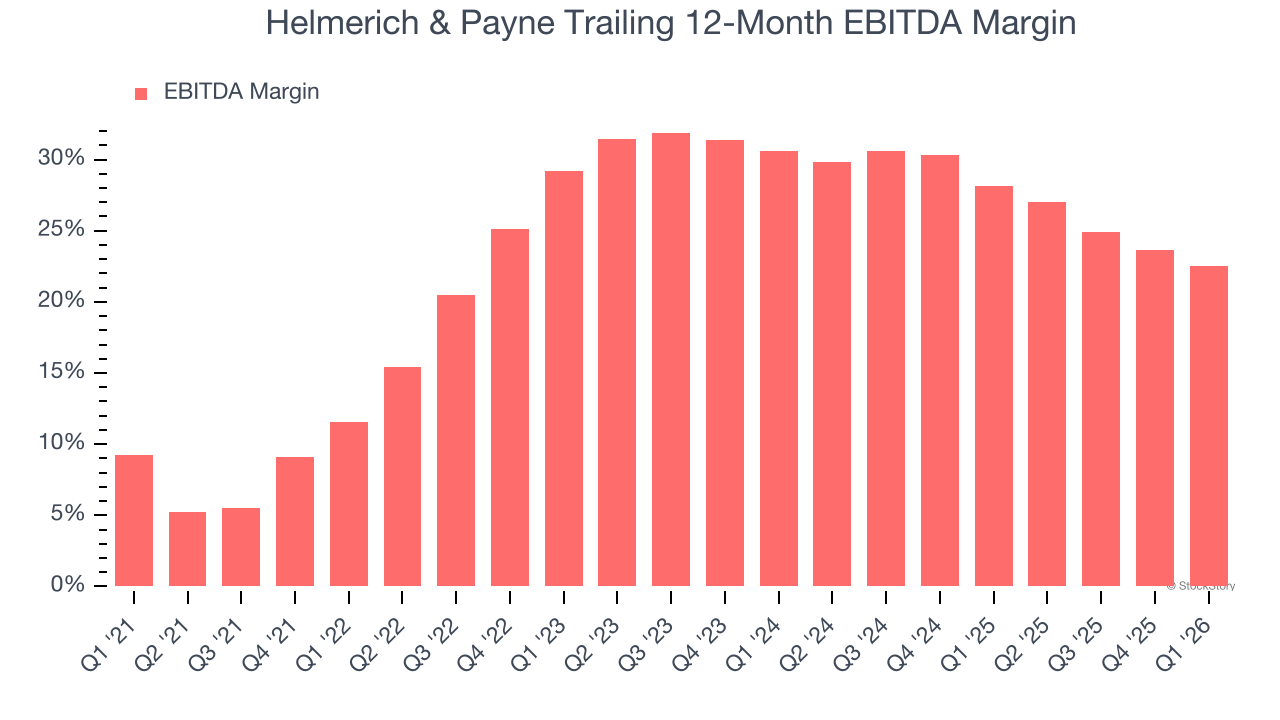

- Adjusted EBITDA: $177.9 million vs analyst estimates of $189 million (19.1% margin, 5.9% miss)

- Operating Margin: -4%, down from 4.1% in the same quarter last year

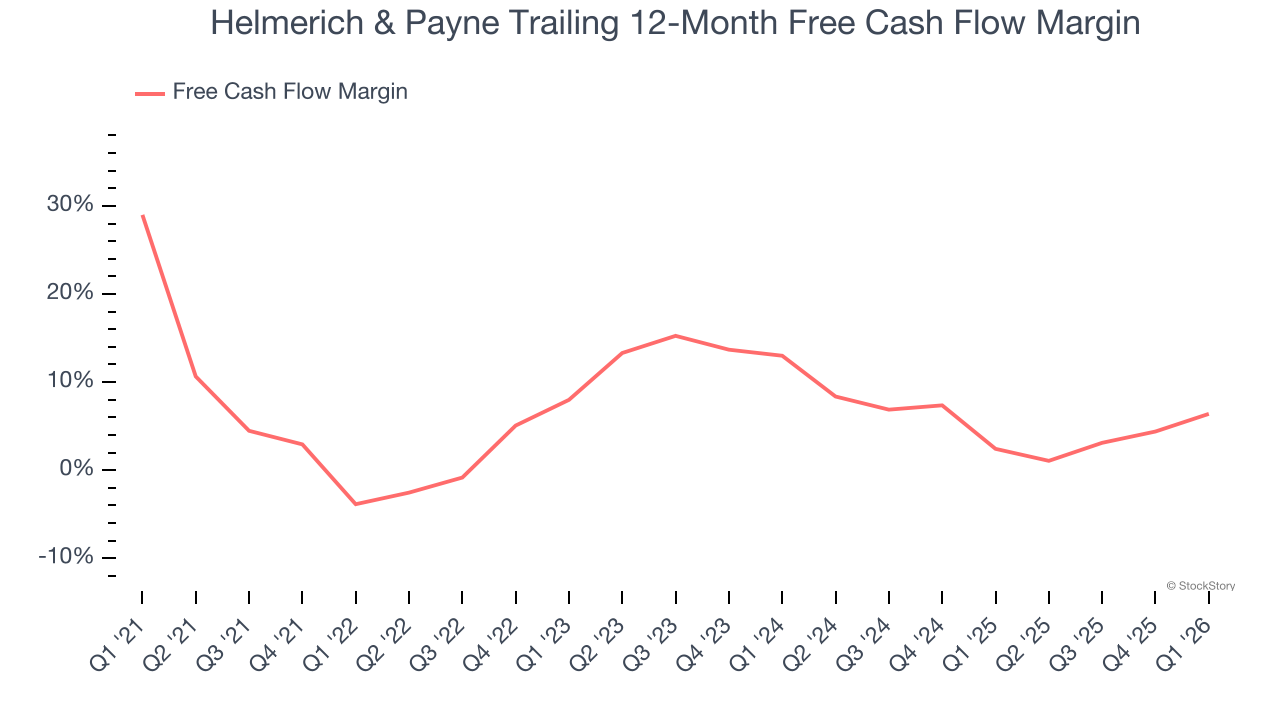

- Free Cash Flow was -$26.28 million compared to -$102.7 million in the same quarter last year

- Market Capitalization: $4.15 billion

Company Overview

Operating the largest fleet of super-spec rigs in North America with technology that can drill horizontal wells over two miles long, Helmerich & Payne (NYSE: HP) provides drilling rigs and crews to oil and gas companies that need wells drilled to extract hydrocarbons from underground.

Revenue Growth

Cyclical industries such as Energy can make mediocre companies look great for a time, but a long-term view reveals which businesses can actually withstand and adapt to changing conditions. Thankfully, Helmerich & Payne’s 32.2% annualized revenue growth over the last five years was incredible. Its growth beat the average energy upstream and integrated energy company and shows its offerings resonate with customers, a helpful starting point for our analysis.

Energy cycles can be long enough that a single five-year period can still reflect one price environment, which is why an additional, decade-long view can help capture through-cycle performance. Helmerich & Payne’s annualized revenue growth of 7.7% over the last ten years is below its five-year trend, but we still think the results suggest decent demand.

This quarter, Helmerich & Payne missed Wall Street’s estimates and reported a rather uninspiring 8.2% year-on-year revenue decline, generating $932.4 million of revenue.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Adjusted EBITDA Margin

Helmerich & Payne was profitable over the last five years but held back by its large cost base. Its average EBITDA margin of 25.4% was weak for an upstream and integrated energy business.

On the plus side, Helmerich & Payne’s EBITDA margin rose by 11 percentage points over the last year, as its sales growth gave it immense operating leverage.

In Q1, Helmerich & Payne generated an EBITDA margin profit margin of 19.1%, down 4.7 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue. This adjusted EBITDA fell short of Wall Street’s estimates.

Cash Is King

Adjusted EBITDA shows how profitable a company’s existing wells are before financing and reinvestment decisions, but free cash flow shows how much value remains after paying the cost of replacing those wells. In upstream energy, production naturally declines over time, so companies must continuously reinvest just to stand still. A producer can report strong EBITDA margins yet generate little or no free cash flow if its wells decline quickly or if new drilling is expensive. Free cash flow therefore captures not only how efficiently a company produces hydrocarbons today, but also how costly it is to sustain that production into the future.

Helmerich & Payne has shown mediocre cash profitability relative to peers over the last five years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 6%, below what we’d expect for an upstream and integrated energy business.

The level of free cash flow is important, but its durability across cycles is just as critical. Consistent margins are far more valuable than volatile swings driven by commodity prices.

Helmerich & Payne’s ratio of quarterly free cash flow volatility to WTI crude price volatility over the past five years was 10.8 (lower is better), indicating that its cash generation is far more sensitive to commodity-price swings than most peers. This elevated volatility limits its access to capital in downturns and makes it unlikely to act as a consolidator when weaker competitors come under pressure.

You may be asking why we wait until the free cash flow line to perform this stability analysis versus commodity prices. Why not compare revenue or EBITDA to WTI Crude prices in the case of Helmerich & Payne? Because what ultimately matters is not how much revenue or profit you earn when prices are high but how much cash you can generate when prices are low. Free cash flow is the superior metric because it includes everything from hedging prowess to growth and maintenance capex to management behavior during good times and bad.

Helmerich & Payne burned through $26.28 million of cash in Q1, equivalent to a negative 2.8% margin. The company’s cash burn slowed from $102.7 million of lost cash in the same quarter last year. These numbers deviate from its longer-term margin, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings.

Key Takeaways from Helmerich & Payne’s Q1 Results

We struggled to find many positives in these results. Its EPS missed and its revenue fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 3.8% to $38.33 immediately following the results.

Helmerich & Payne may have had a tough quarter, but does that actually create an opportunity to invest right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).