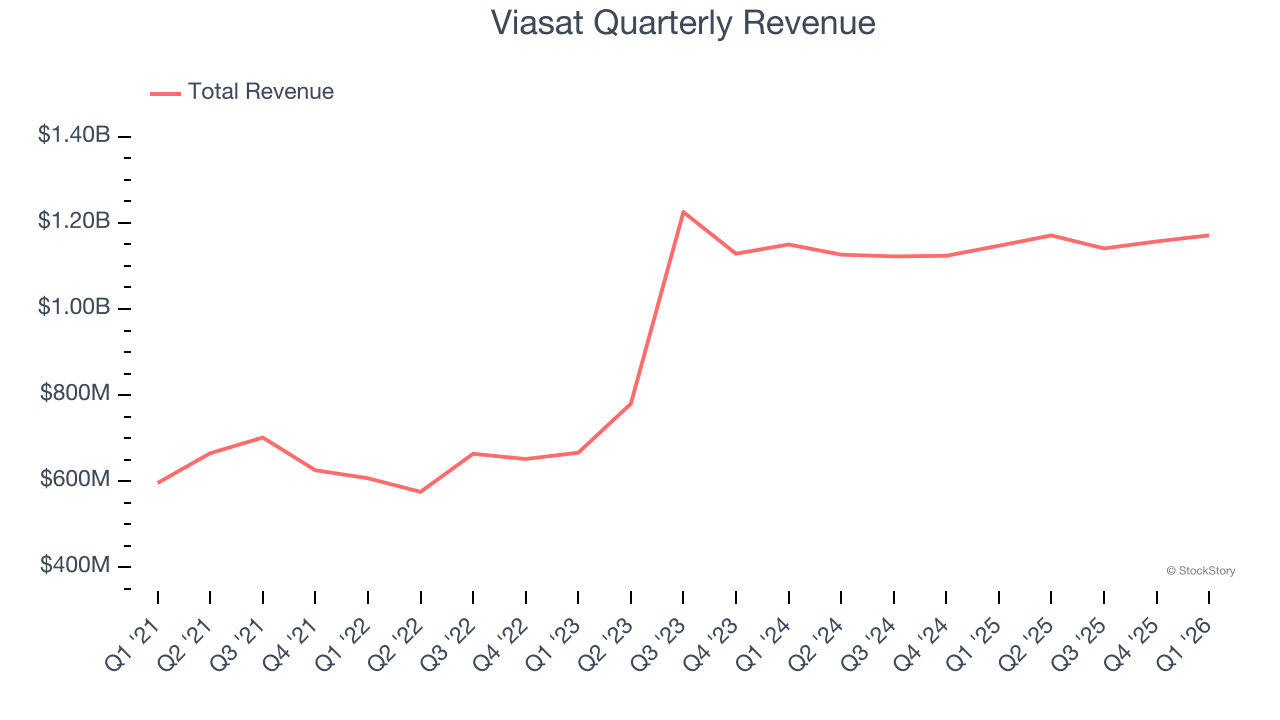

Global satellite communications provider Viasat (NASDAQ: VSAT) fell short of the market’s revenue expectations in Q1 CY2026 as sales rose 2.1% year on year to $1.17 billion. Its non-GAAP loss of $0.02 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Viasat? Find out by accessing our full research report, it’s free.

Viasat (VSAT) Q1 CY2026 Highlights:

- Revenue: $1.17 billion vs analyst estimates of $1.21 billion (2.1% year-on-year growth, 3% miss)

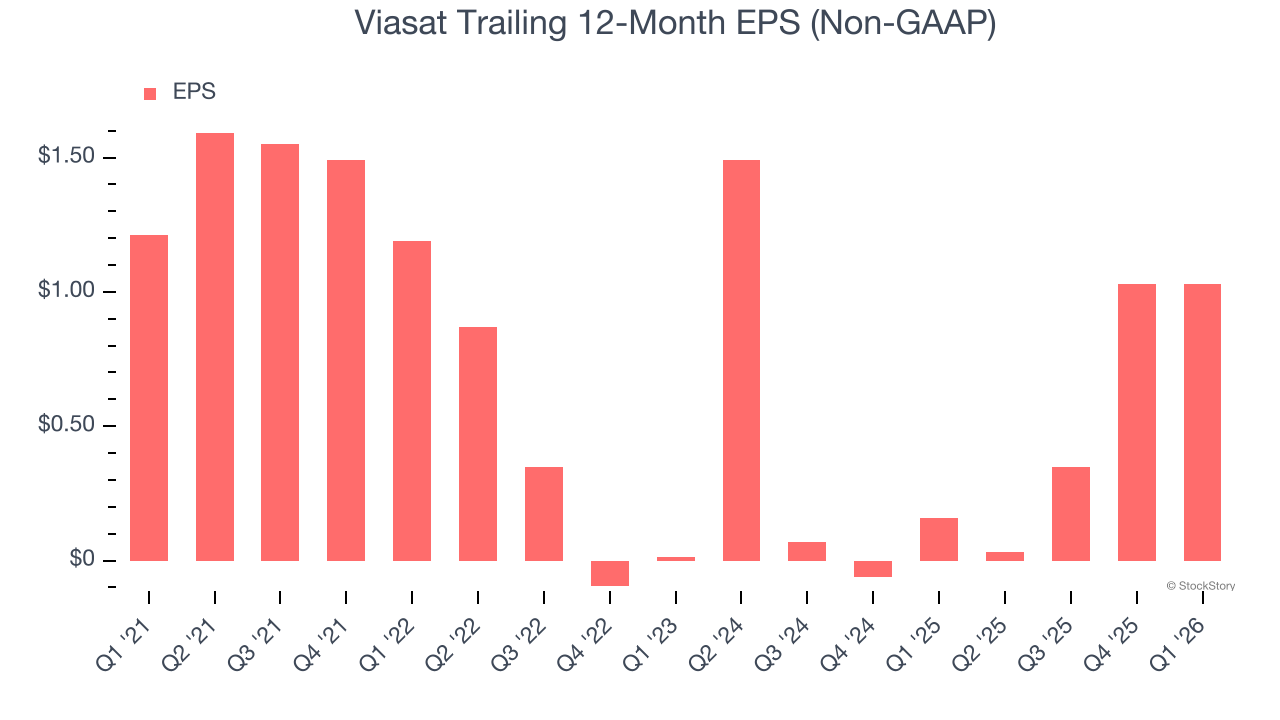

- Adjusted EPS: -$0.02 vs analyst estimates of $0.32 (significant miss)

- Adjusted EBITDA: $369.9 million vs analyst estimates of $383.3 million (31.6% margin, 3.5% miss)

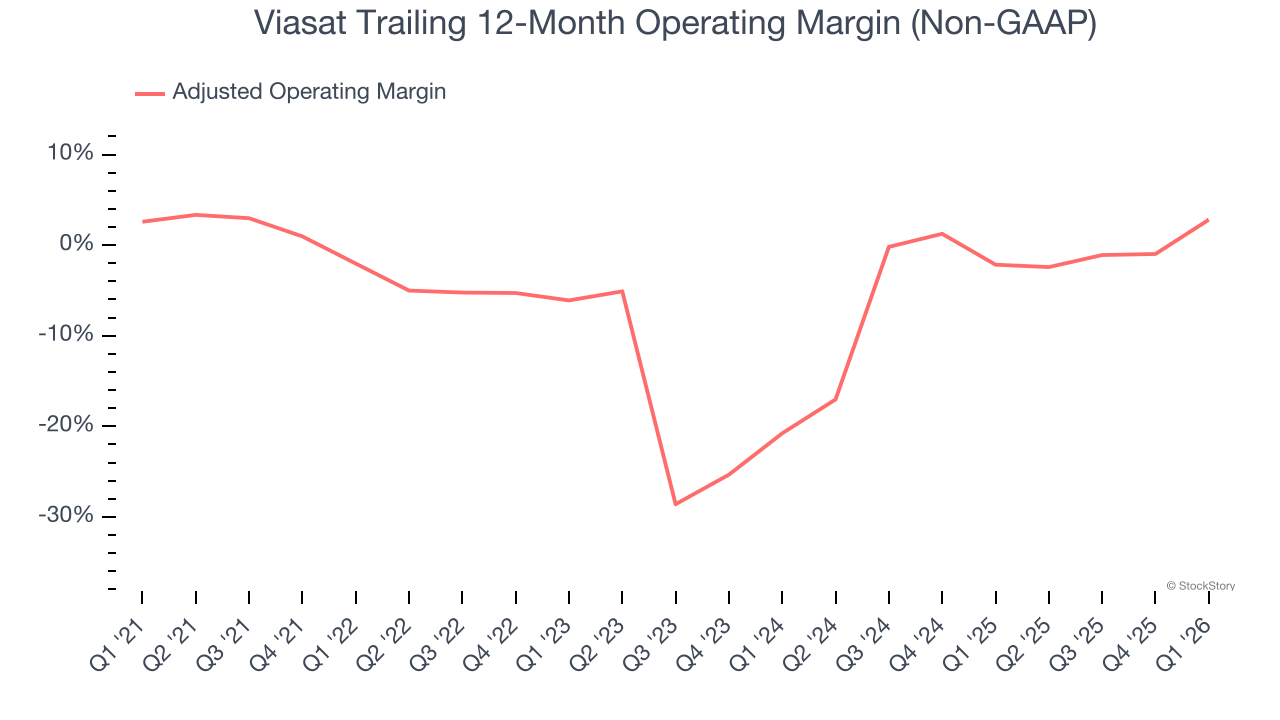

- Operating Margin: -0.1%, up from -13.4% in the same quarter last year

- Free Cash Flow Margin: 2%, down from 4.4% in the same quarter last year

- Market Capitalization: $11.62 billion

Company Overview

Operating a fleet of 23 satellites that orbit the Earth and beam connectivity from space, Viasat (NASDAQ: VSAT) provides satellite-based communications networks and services for airlines, maritime vessels, governments, businesses, and residential customers worldwide.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $4.64 billion in revenue over the past 12 months, Viasat is one of the larger companies in the business services industry and benefits from a well-known brand that influences purchasing decisions.

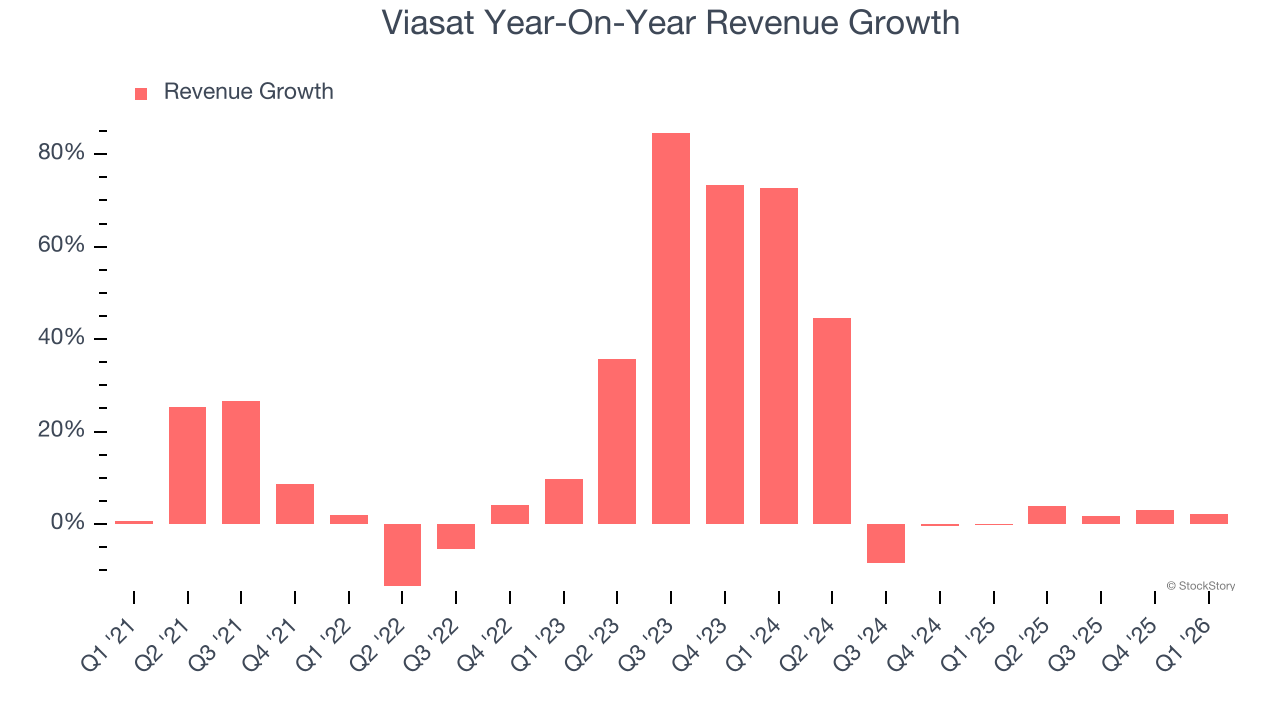

As you can see below, Viasat’s sales grew at an incredible 15.5% compounded annual growth rate over the last five years. This shows it had high demand, a useful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Viasat’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 4.1% over the last two years was well below its five-year trend.

This quarter, Viasat’s revenue grew by 2.1% year on year to $1.17 billion, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 4.9% over the next 12 months, similar to its two-year rate. This projection doesn’t excite us and indicates its newer products and services will not catalyze better top-line performance yet.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Adjusted Operating Margin

Adjusted operating margin is a key measure of profitability. Think of it as net income (the bottom line) excluding the impact of non-recurring expenses, taxes, and interest on debt - metrics less connected to business fundamentals.

Although Viasat was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average adjusted operating margin of negative 5.7% over the last five years. Unprofitable business services companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, Viasat’s adjusted operating margin rose by 4.8 percentage points over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to reach long-term profitability.

This quarter, Viasat generated an adjusted operating margin profit margin of 1.8%, up 15.2 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth — for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Viasat, its EPS declined by 3.2% annually over the last five years while its revenue grew by 15.5%. However, its adjusted operating margin actually improved during this time, telling us that non-fundamental factors such as interest expenses and taxes affected its ultimate earnings.

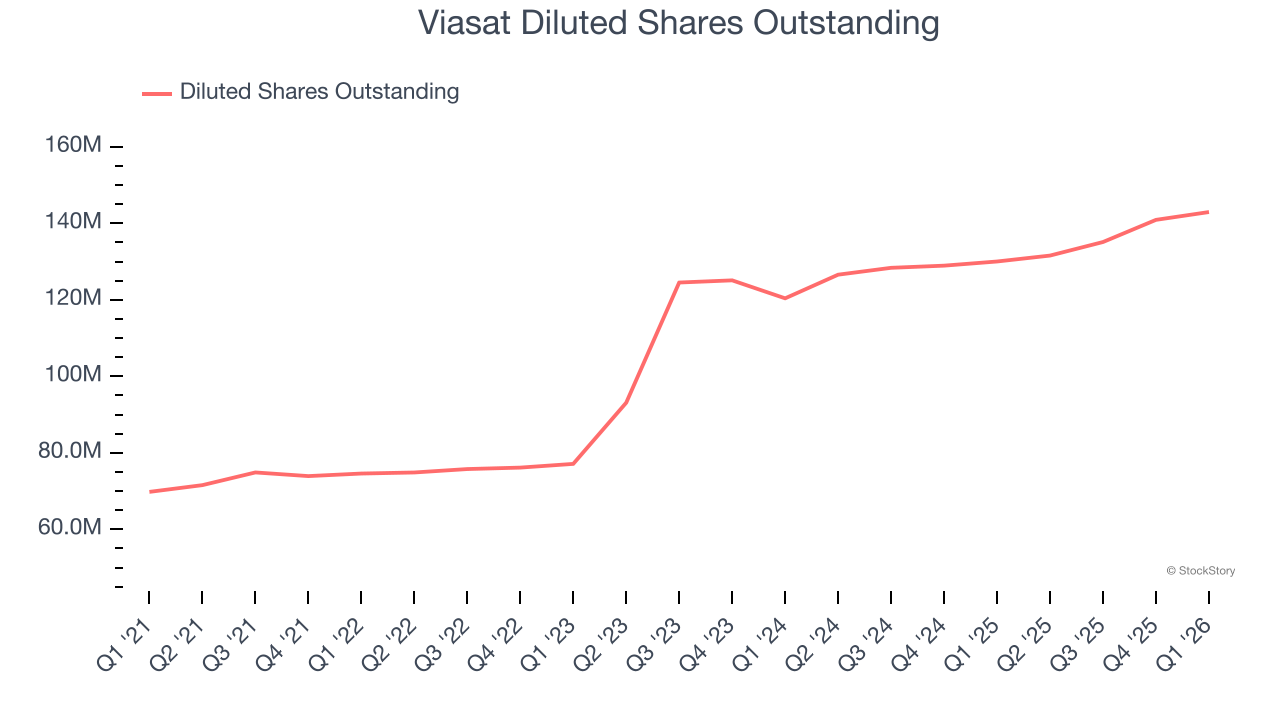

Diving into the nuances of Viasat’s earnings can give us a better understanding of its performance. A five-year view shows Viasat has diluted its shareholders, growing its share count by 105%. This dilution overshadowed its increased operational efficiency and has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Viasat, its two-year annual EPS declines of 15% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q1, Viasat reported adjusted EPS of negative $0.02, in line with the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Viasat’s full-year EPS to shrink by 53.4% from $1.03 to $0.48. This is unusual as its revenue and operating margin are anticipated to increase, signaling the fall likely stems from “below-the-line” items such as taxes.

Key Takeaways from Viasat’s Q1 Results

We struggled to find many positives in these results. Its revenue missed and its EPS fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 6.4% to $82.50 immediately after reporting.

Viasat may have had a tough quarter, but does that actually create an opportunity to invest right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).