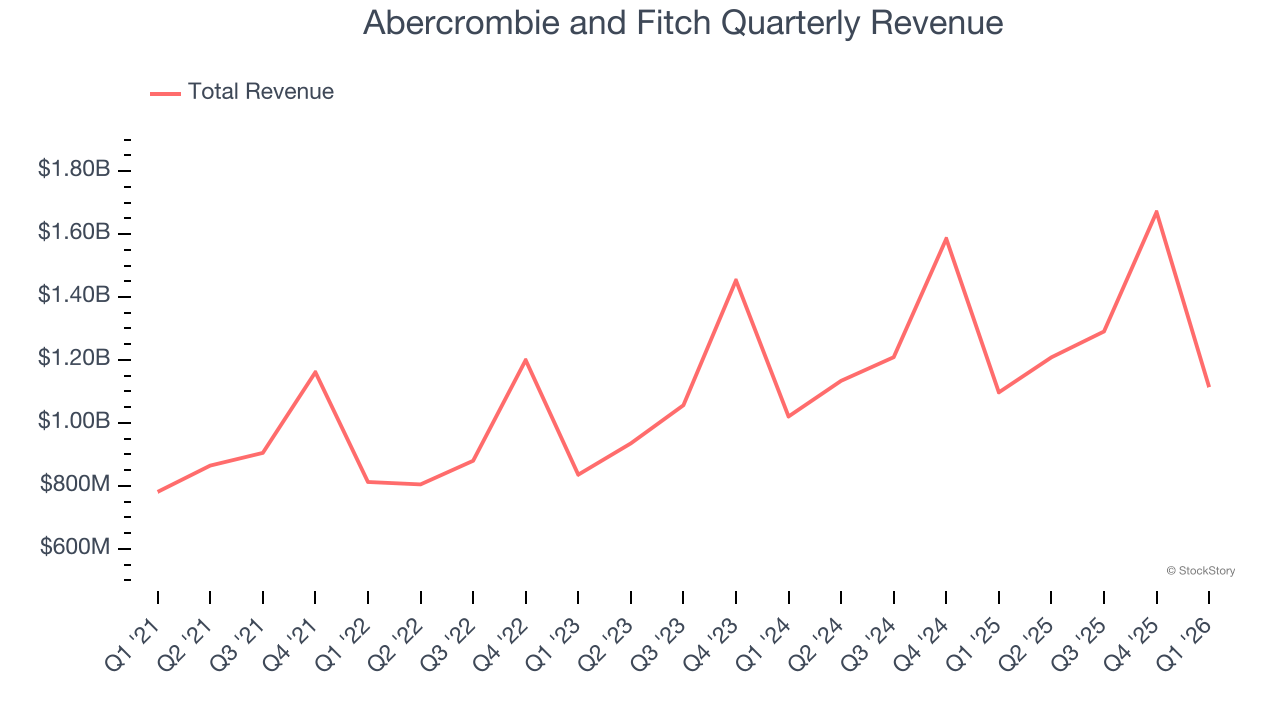

Young adult apparel retailer Abercrombie & Fitch (NYSE: ANF) fell short of the market’s revenue expectations in Q1 CY2026 as sales only rose 1.5% year on year to $1.11 billion. Next quarter’s revenue guidance of $1.24 billion underwhelmed, coming in 0.7% below analysts’ estimates. Its GAAP profit of $1.47 per share was 15.7% above analysts’ consensus estimates.

Is now the time to buy Abercrombie and Fitch? Find out by accessing our full research report, it’s free.

Abercrombie and Fitch (ANF) Q1 CY2026 Highlights:

- Revenue: $1.11 billion vs analyst estimates of $1.12 billion (1.5% year-on-year growth, 0.8% miss)

- EPS (GAAP): $1.47 vs analyst estimates of $1.27 (15.7% beat)

- Adjusted EBITDA: $131.1 million vs analyst estimates of $117.2 million (11.8% margin, 11.9% beat)

- Revenue Guidance for Q2 CY2026 is $1.24 billion at the midpoint, below analyst estimates of $1.25 billion

- EPS (GAAP) guidance for the full year is $10.60 at the midpoint, missing analyst estimates by 1.1%

- Operating Margin: 8%, down from 9.3% in the same quarter last year

- Free Cash Flow was -$17.09 million compared to -$54.76 million in the same quarter last year

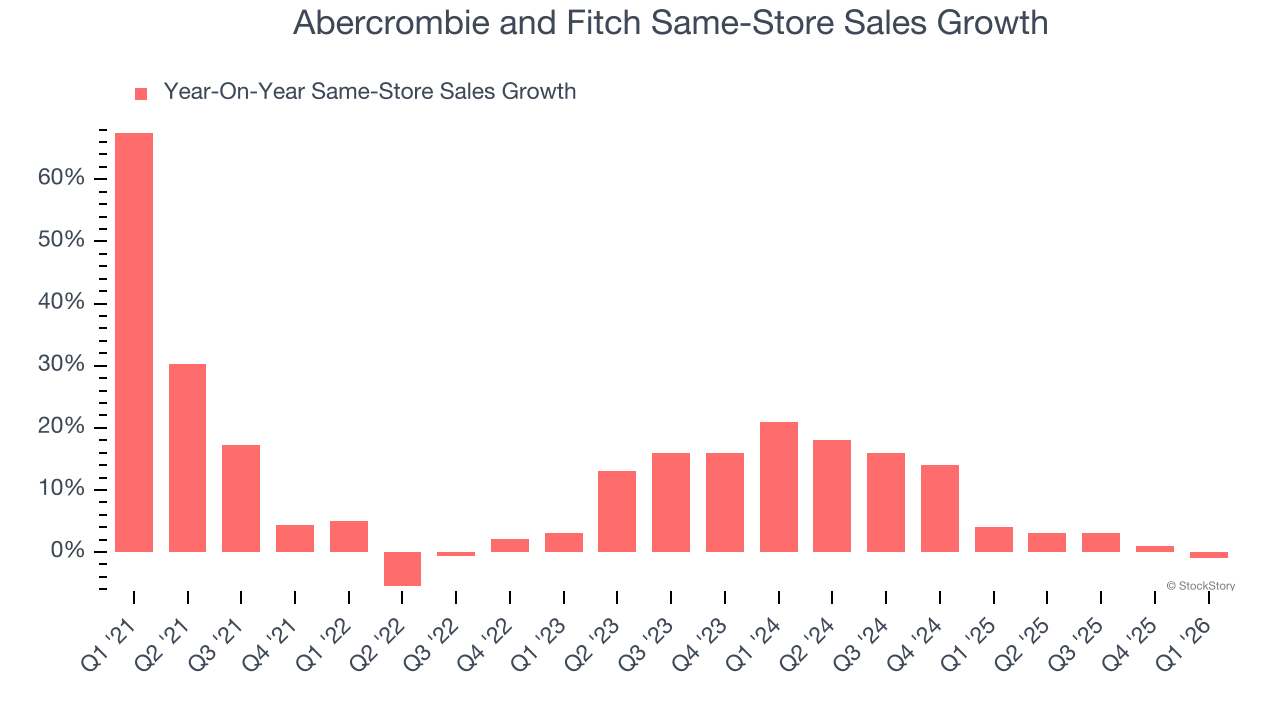

- Same-Store Sales fell 1% year on year (4% in the same quarter last year)

- Market Capitalization: $3.35 billion

Fran Horowitz, Chief Executive Officer, said, “We delivered record first quarter net sales and our 14th consecutive quarter of growth, reflecting our teams’ consistent execution for our customers amid a dynamic global environment. Results were driven by continued growth in the Americas, led by Abercrombie Brands, along with strong growth in APAC. In EMEA, demand softened as the Middle East conflict ramped up, particularly impacting Hollister Brands, and we are proactively managing inventory and marketing to support the region. Our bottom-line results reflect discipline and consistency, with both operating margin and earnings per diluted share exceeding our outlook. We continued to invest in stores and marketing to strengthen our brands and customer experiences, while also returning $105 million to shareholders through share repurchases, supported by our strong balance sheet.

Company Overview

Founded as an outdoor and sporting brand, Abercrombie & Fitch (NYSE: ANF) evolved to become a specialty retailer that sells its own brand of fashionable clothing to young adults.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $5.28 billion in revenue over the past 12 months, Abercrombie and Fitch is a mid-sized retailer, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale. On the bright side, it can still flex high growth rates because it’s working from a smaller revenue base.

As you can see below, Abercrombie and Fitch grew its sales at a decent 12.4% compounded annual growth rate over the last three years as it opened new stores and increased sales at existing, established locations.

This quarter, Abercrombie and Fitch’s revenue grew by 1.5% year on year to $1.11 billion, falling short of Wall Street’s estimates. Company management is currently guiding for a 3% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 4.5% over the next 12 months, a deceleration versus the last three years. Still, this projection is commendable and suggests the market sees success for its products.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Store Performance

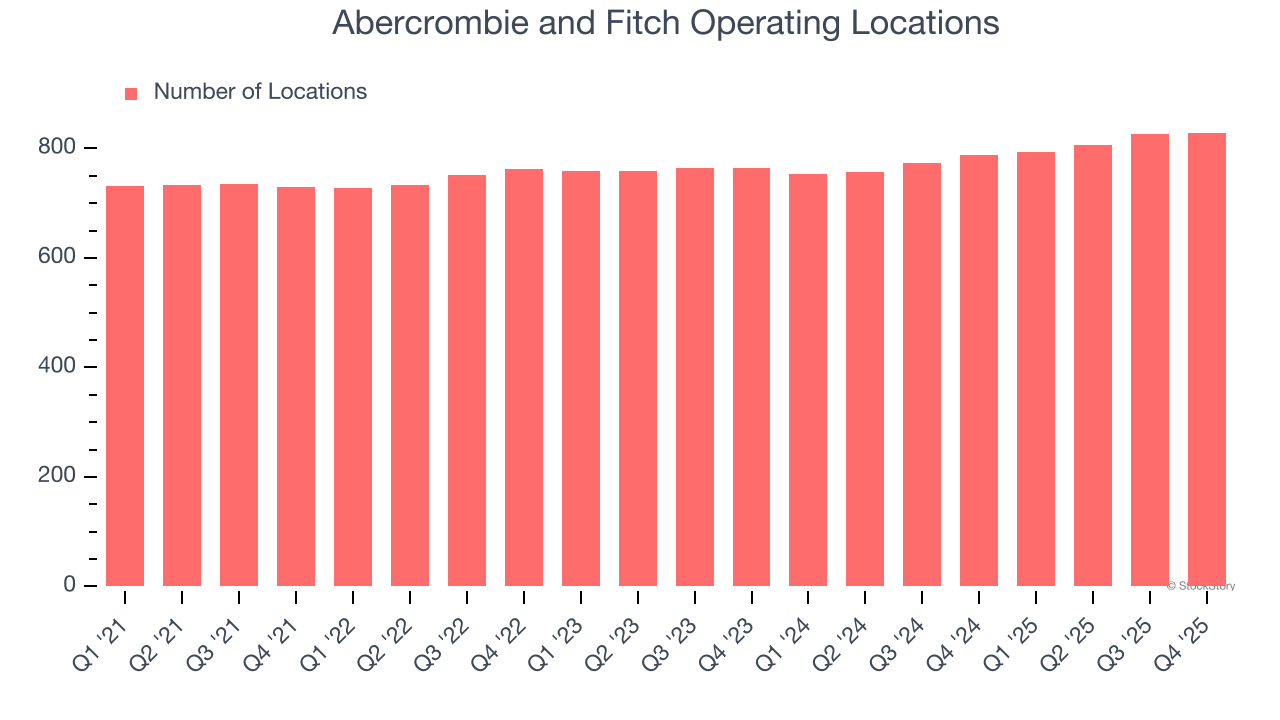

Number of Stores

A retailer’s store count influences how much it can sell and how quickly revenue can grow.

Over the last two years, Abercrombie and Fitch opened new stores quickly, averaging 4% annual growth. This was faster than the broader consumer retail sector.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

Note that Abercrombie and Fitch reports its store count intermittently, so some data points are missing in the chart below.

Same-Store Sales

The change in a company's store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales provides a deeper understanding of this issue because it measures organic growth at brick-and-mortar shops for at least a year.

Abercrombie and Fitch has been one of the most successful retailers over the last two years thanks to skyrocketing demand within its existing locations. On average, the company has posted exceptional year-on-year same-store sales growth of 7.3%. This performance suggests its rollout of new stores is beneficial for shareholders. We like this backdrop because it gives Abercrombie and Fitch multiple ways to win: revenue growth can come from new stores, e-commerce, or increased foot traffic and higher sales per customer at existing locations.

In the latest quarter, Abercrombie and Fitch’s same-store sales fell by 1% year on year. This decline was a reversal from its historical levels. A one quarter hiccup shouldn’t deter you from investing in a business, and we’ll be monitoring the company to see how things progress.

Key Takeaways from Abercrombie and Fitch’s Q1 Results

We were impressed by how significantly Abercrombie and Fitch blew past analysts’ EBITDA expectations this quarter. We were also glad its gross margin outperformed Wall Street’s estimates. On the other hand, its EPS guidance for next quarter missed and its full-year EPS guidance fell slightly short of Wall Street’s estimates. Zooming out, we think this was a mixed quarter. The stock traded up 6.2% to $78.99 immediately after reporting.

Is Abercrombie and Fitch an attractive investment opportunity right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).