Over the past six months, 1st Source has been a great trade, beating the S&P 500 by 7%. Its stock price has climbed to $73.91, representing a healthy 17% increase. This run-up might have investors contemplating their next move.

Is now still a good time to buy SRCE? Or is this a case of a company fueled by heightened investor enthusiasm? Find out in our full research report, it’s free.

Why Does SRCE Stock Spark Debate?

Tracing its roots back to 1863 during the Civil War era, 1st Source Corporation (NASDAQ: SRCE) is a regional bank holding company that provides commercial, consumer, specialty finance, and wealth management services across Indiana, Michigan, and Florida.

Two Things to Like:

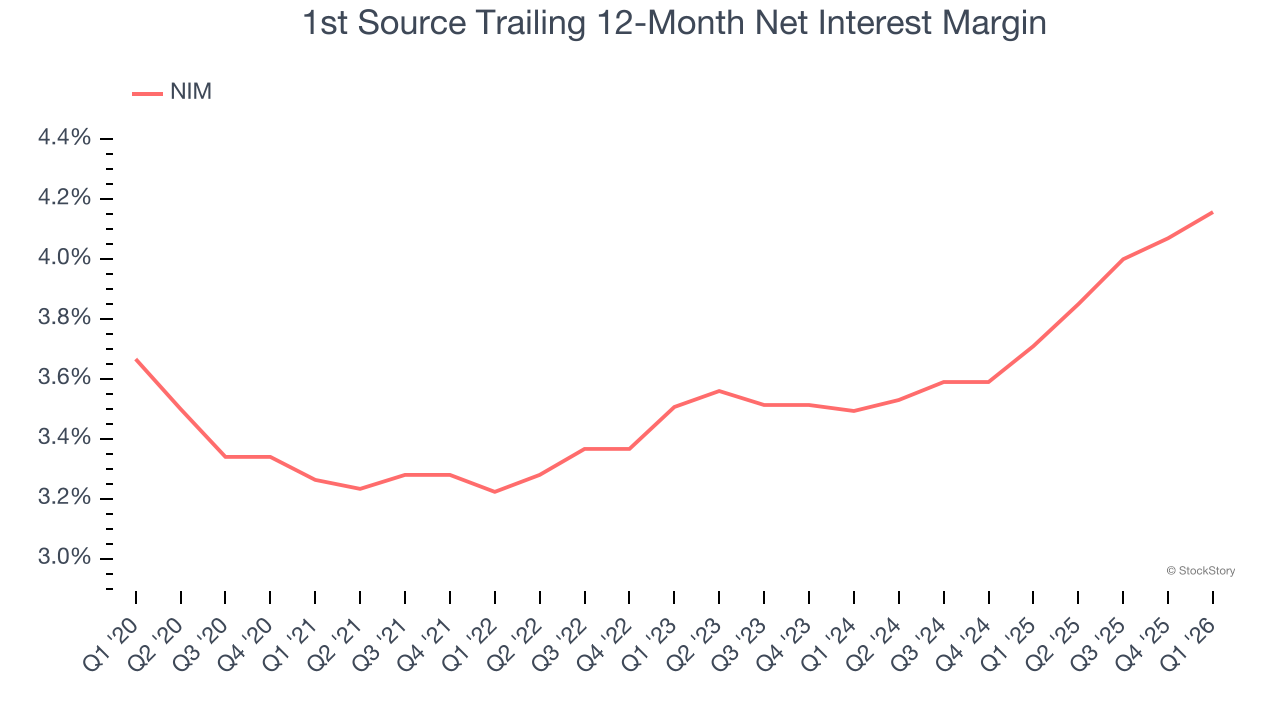

1. Increasing Net Interest Margin Juices Financials

Net interest margin (NIM) serves as a critical gauge of a bank's fundamental profitability by showing the spread between interest income and interest expenses. It's essential for understanding whether a firm can sustainably generate returns from its lending operations.

Over the past two years, 1st Source’s net interest margin averaged 4%, climbing by 66.4 basis points (100 basis points = 1 percentage point) over that period.

This expansion was a tailwind for its net interest income, and while prevailing interest rates matter the most for industry net interest margins, banks that consistently increase this figure generally boast higher-earning loan books (all else equal such as the risk of those loans) or provide differentiated services that give them the ability to charge higher rates (pricing power).

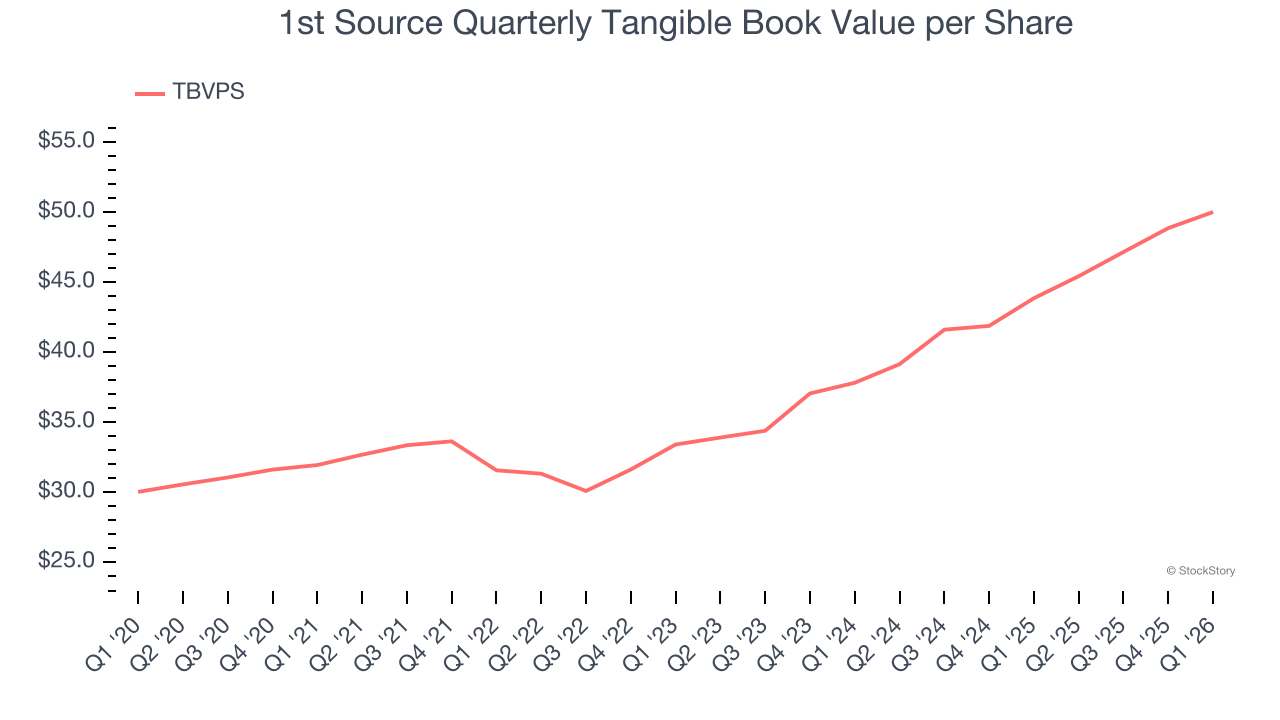

2. Growing TBVPS Reflects Strong Asset Base

We consider tangible book value per share (TBVPS) the most important metric to track for banks. TBVPS represents the real, liquid net worth per share of a bank, excluding intangible assets that have debatable value upon liquidation.

1st Source’s TBVPS increased by 9.4% annually over the last five years, and growth has recently accelerated as TBVPS grew at an impressive 15% annual clip over the past two years (from $37.83 to $50.03 per share).

One Reason to be Careful:

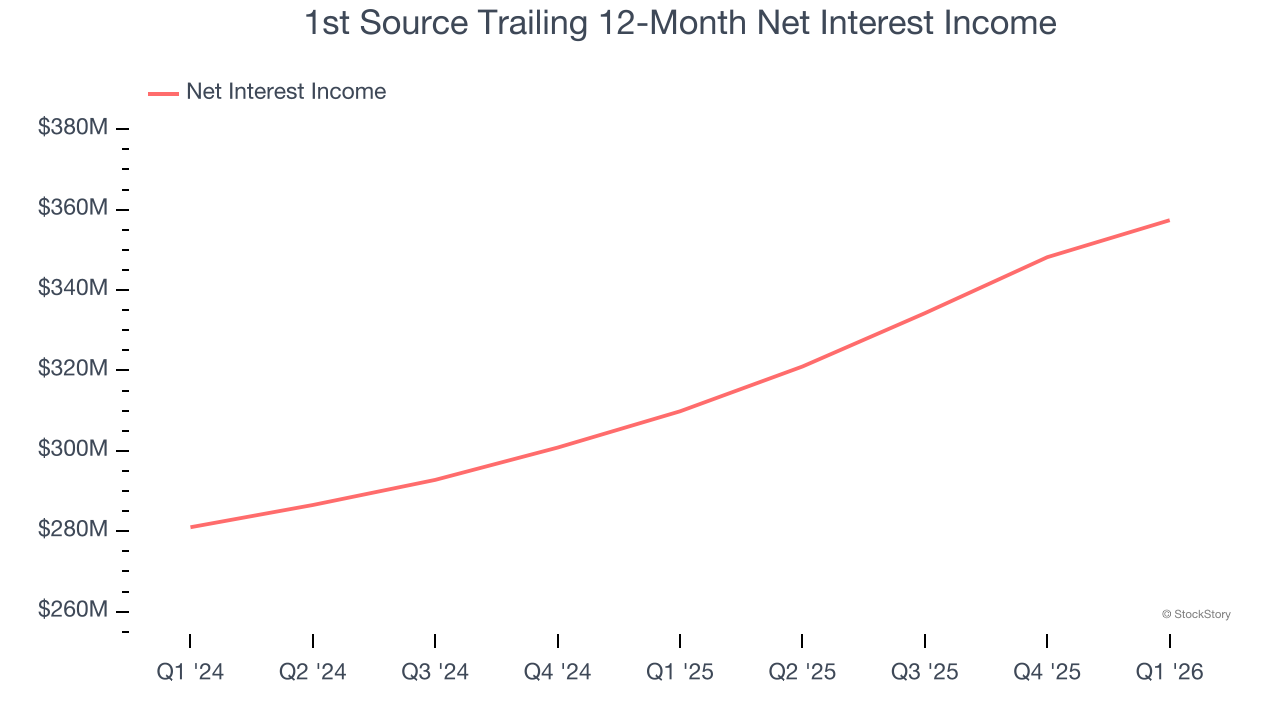

Net Interest Income Points to Soft Demand

Markets consistently prioritize net interest income over non-recurring fees, recognizing its superior quality compared to the more unpredictable revenue streams.

1st Source’s net interest income has grown at a 9.4% annualized rate over the last five years, slightly worse than the broader banking industry.

Final Judgment

1st Source’s positive characteristics outweigh the negatives, and with its shares topping the market in recent months, the stock trades at 1.3× forward P/B (or $73.91 per share). Is now the time to initiate a position? See for yourself in our comprehensive research report, it’s free.

Stocks We Like Even More Than 1st Source

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.