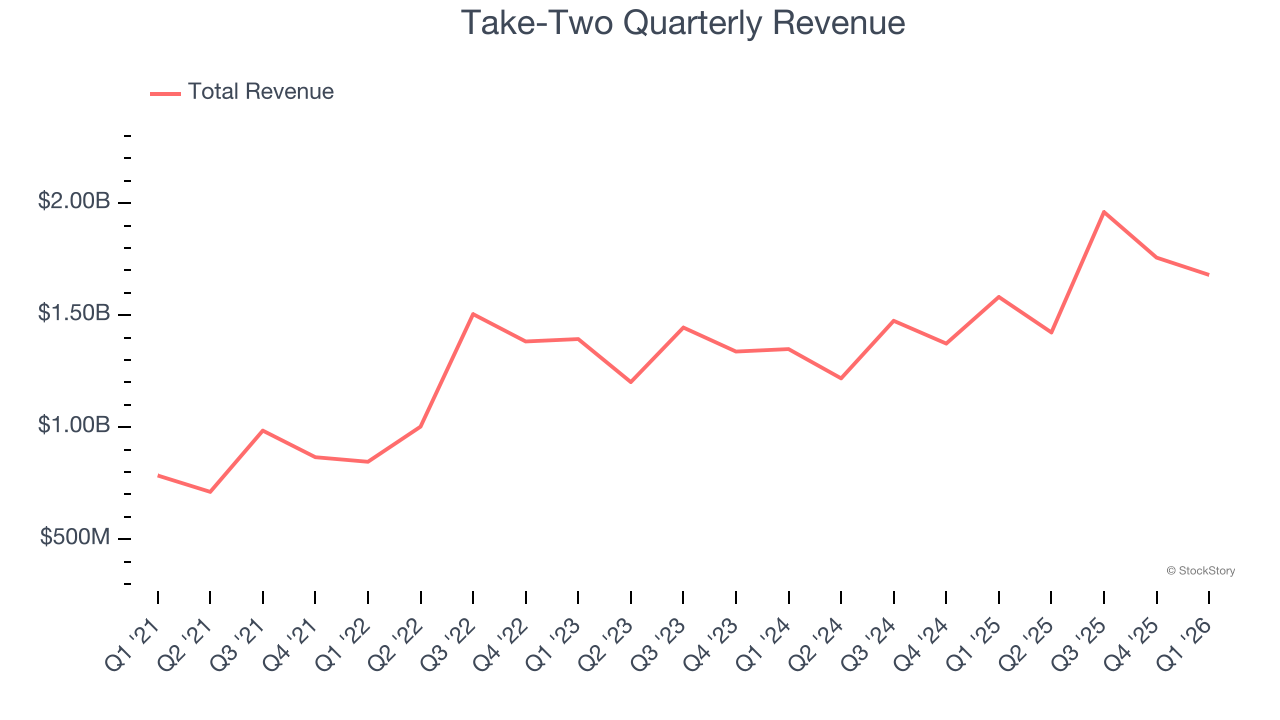

Video game publisher Take Two (NASDAQ: TTWO) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 6.2% year on year to $1.68 billion. On the other hand, next quarter’s revenue guidance of $1.48 billion was less impressive, coming in 4.1% below analysts’ estimates. Its GAAP loss of $0.32 per share was 38.2% above analysts’ consensus estimates.

Is now the time to buy Take-Two? Find out by accessing our full research report, it’s free.

Take-Two (TTWO) Q1 CY2026 Highlights:

- Revenue: $1.68 billion vs analyst estimates of $1.56 billion (6.2% year-on-year growth, 7.9% beat)

- EPS (GAAP): -$0.32 vs analyst estimates of -$0.52 (38.2% beat)

- Adjusted EBITDA: $243.7 million vs analyst estimates of $189.3 million (14.5% margin, 28.7% beat)

- Revenue Guidance for Q2 CY2026 is $1.48 billion at the midpoint, below analyst estimates of $1.54 billion

- EPS (GAAP) guidance for the upcoming financial year 2027 is $0.65 at the midpoint, missing analyst estimates by 82.7%

- EBITDA guidance for the upcoming financial year 2027 is $1.04 billion at the midpoint, below analyst estimates of $1.95 billion

- Operating Margin: 0.6%, up from -239% in the same quarter last year

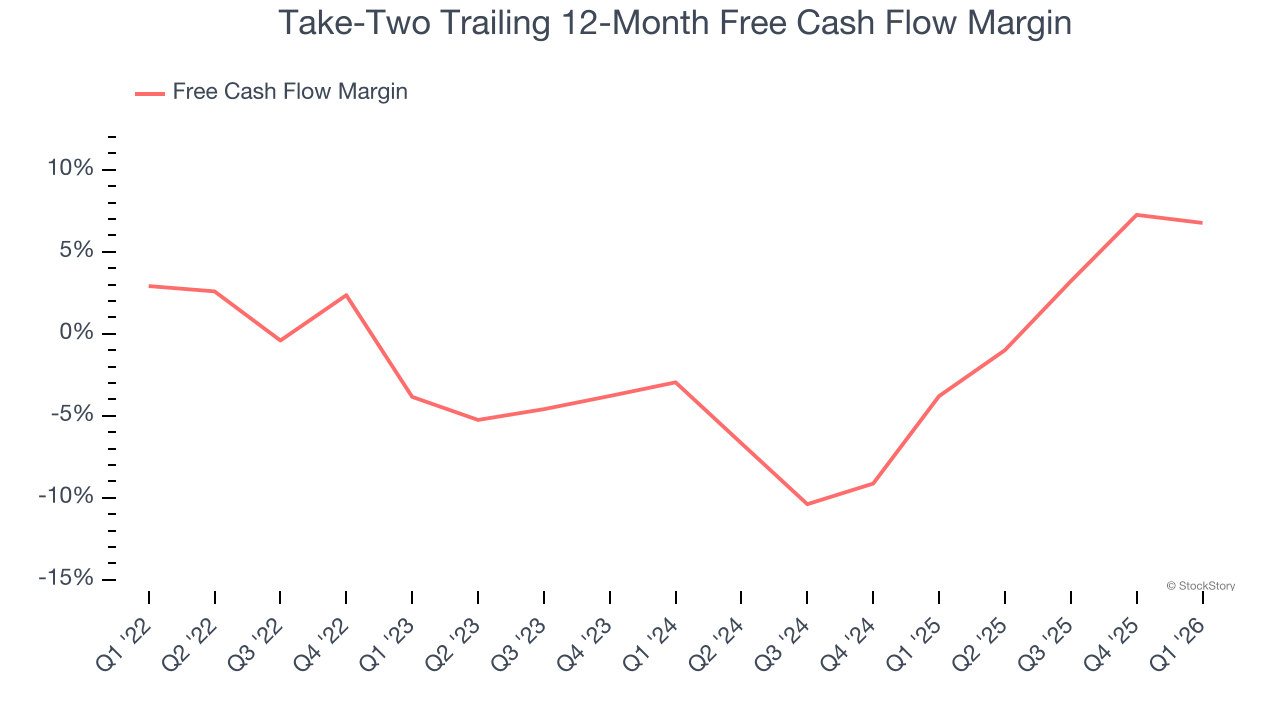

- Free Cash Flow Margin: 11.8%, down from 13.4% in the previous quarter

- Market Capitalization: $43.82 billion

Company Overview

Best known for its Grand Theft Auto and NBA 2K franchises, Take Two (NASDAQ: TTWO) is one of the world’s largest video game publishers.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last three years, Take-Two grew its sales at a mediocre 8.9% compounded annual growth rate. This wasn’t a great result compared to the rest of the consumer internet sector, but there are still things to like about Take-Two.

This quarter, Take-Two reported year-on-year revenue growth of 6.2%, and its $1.68 billion of revenue exceeded Wall Street’s estimates by 7.9%. Company management is currently guiding for a 3.6% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 36.5% over the next 12 months, an acceleration versus the last three years. This projection is eye-popping and suggests its newer products and services will fuel better top-line performance.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Take-Two has shown weak cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 2%, below what we’d expect for a consumer internet business. The divergence from its good EBITDA margin stems from its capital-intensive business model, which requires Take-Two to make large cash investments in working capital (i.e., stocking inventories) and capital expenditures (i.e., building new facilities).

Taking a step back, an encouraging sign is that Take-Two’s margin expanded by 10.6 percentage points over the last few years. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability was flat.

Take-Two’s free cash flow clocked in at $198.6 million in Q1, equivalent to a 11.8% margin. The company’s cash profitability regressed as it was 2.4 percentage points lower than in the same quarter last year, but it’s still above its two-year average. We wouldn’t read too much into this quarter’s decline because investment needs can be seasonal, leading to short-term swings. Long-term trends trump temporary fluctuations.

Key Takeaways from Take-Two’s Q1 Results

We were impressed by how significantly Take-Two blew past analysts’ EBITDA expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. On the other hand, its full-year revenue guidance missed and its full-year EBITDA guidance fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded up 6.9% to $256.56 immediately after reporting.

Is Take-Two an attractive investment opportunity right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).